- Hyperscalers are expected to spend approximately $760 billion on AI in 2026, while estimated revenues generated from AI products are projected to reach only $80–150 billion.

- Despite growing concerns over investment returns, major technology companies are not slowing spending. Instead, they are intensifying the race for AI dominance.

- Morgan Stanley estimates that global debt issuance linked to AI investments could reach around $570 billion in 2026, representing roughly 100% year-over-year growth.

- Amazon, Microsoft, Alphabet, Meta, and Oracle issued a combined $160 billion in bonds during the first months of 2026 alone, up approximately 47% compared with the whole of 2025.

- AI-related financing already accounts for roughly half of all U.S. investment-grade corporate bond issuance in 2026.

- Hyperscalers are expected to spend approximately $760 billion on AI in 2026, while estimated revenues generated from AI products are projected to reach only $80–150 billion.

- Despite growing concerns over investment returns, major technology companies are not slowing spending. Instead, they are intensifying the race for AI dominance.

- Morgan Stanley estimates that global debt issuance linked to AI investments could reach around $570 billion in 2026, representing roughly 100% year-over-year growth.

- Amazon, Microsoft, Alphabet, Meta, and Oracle issued a combined $160 billion in bonds during the first months of 2026 alone, up approximately 47% compared with the whole of 2025.

- AI-related financing already accounts for roughly half of all U.S. investment-grade corporate bond issuance in 2026.

In 2026, the world's largest technology companies could spend as much as $760 billion on artificial intelligence infrastructure, while revenues generated directly from AI products are unofficially estimated at only $80–150 billion. This growing imbalance is increasingly unsettling investors, who are beginning to ask whether the current AI boom represents the dawn of a new technological era or merely another costly race for market dominance. The market is no longer questioning AI's transformative potential; instead, it is focused on how quickly these investments can translate into tangible cash flows. This shift is particularly visible in equity market performance, where semiconductor manufacturers and infrastructure providers have significantly outperformed the companies funding the broader AI ecosystem. Capital market history suggests that similar tensions emerged during the build-out of the internet, telecommunications networks, and cloud computing. The key question remains unchanged: who will ultimately capture the economic rents generated by the most significant technological transformation of recent decades?

Investors Are Paying Closer Attention to AI Returns

Over the past two years, investors have focused primarily on the scale of spending announced by the largest technology companies. Amazon, Microsoft, Alphabet, Meta, and Oracle have consistently expanded budgets for data centers, advanced processors, and the computing infrastructure required to support AI development.

It is therefore unsurprising that investors are increasingly questioning the relationship between spending and future revenue generation. If the sector is currently investing between five and nine dollars for every dollar of projected AI revenue, markets naturally expect evidence that such capital allocation is economically justified.

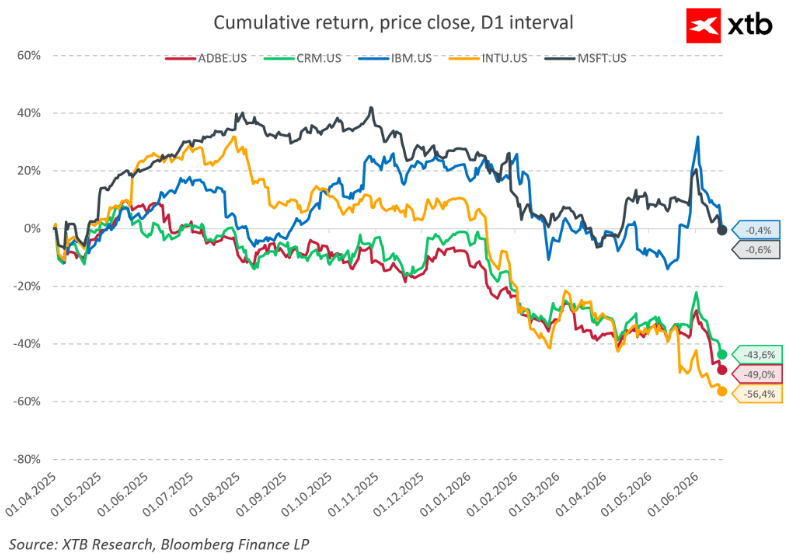

It is no coincidence that the relative valuation of U.S. hyperscalers compared with the semiconductor sector has been trending lower. Investors appear increasingly willing to reward the companies supplying the "picks and shovels" of the AI gold rush, while becoming more demanding toward those financing the infrastructure buildout itself.

Public estimates suggest that hyperscalers could spend roughly $3 trillion on AI by 2030. Even if projections calling for as much as $7 trillion in AI-related revenue over the coming decade prove accurate, the scale of investment remains extraordinary. Assuming these businesses can eventually generate net profit margins of 50% on AI products, it would still take many years for the industry's $3 trillion investment to produce a meaningful return. Meanwhile, software stocks have significantly underperformed for several quarters.

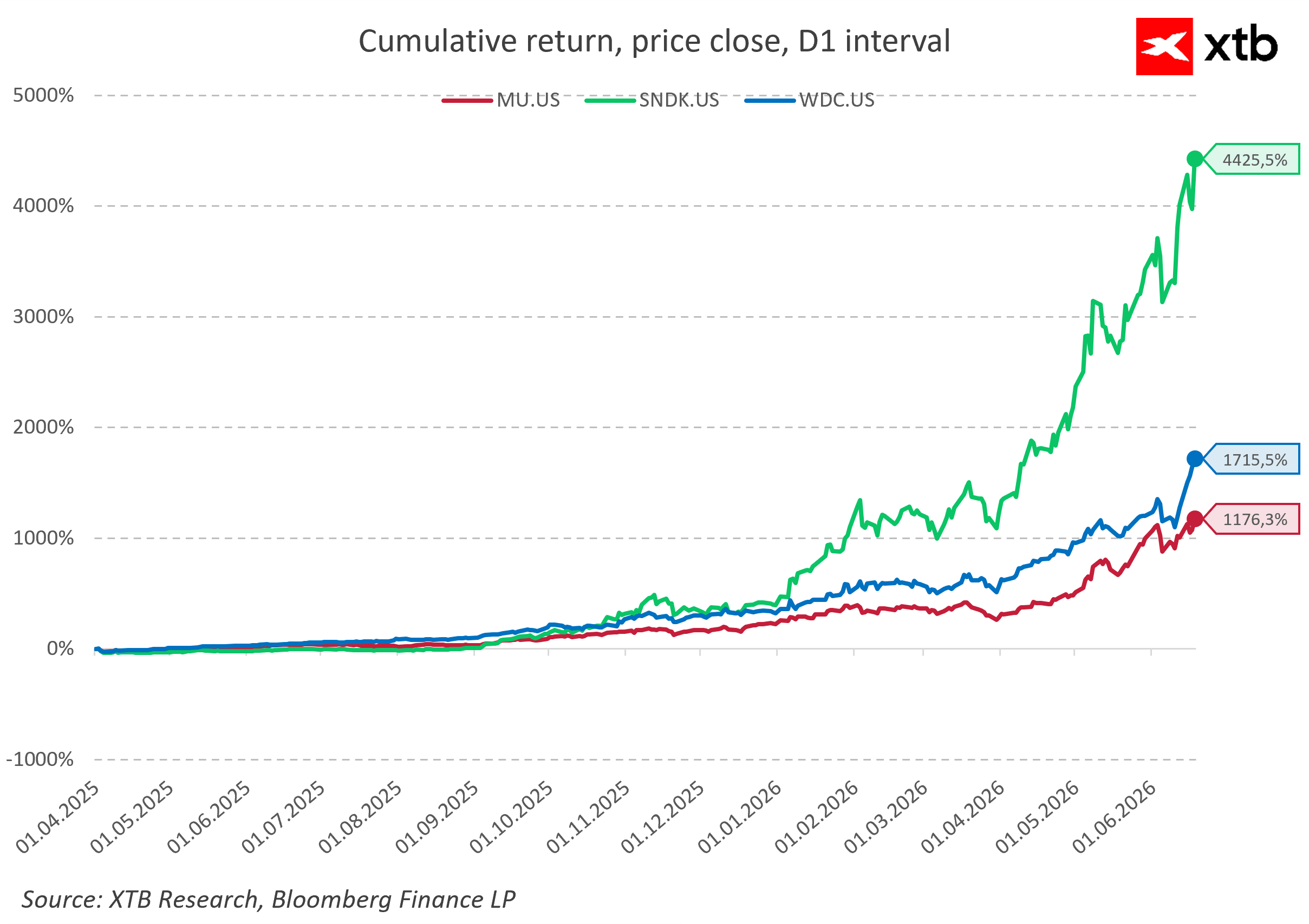

In contrast, shares of memory-chip manufacturers have surged over the same period. Such extreme divergences are rarely healthy and may ultimately undermine the breadth of the technology rally.

The Beneficiaries Are Clear, but the Winners Are Not

The biggest beneficiaries of the current phase of the AI cycle remain chipmakers, memory producers, and providers of cooling systems and energy infrastructure. These companies are the most direct beneficiaries of rising demand for computing power. There is nothing new about this dynamic.

As early as the nineteenth century, investors financed railway construction long before it became clear which railroad companies would survive and profit from the new infrastructure. Similarly, during the late 1990s, capital poured into internet infrastructure before sustainable business models had emerged. Many companies disappeared, but the railways, fiber-optic networks, and data infrastructure remained, becoming the foundation for future waves of economic growth.

However, the highest margins are typically earned at the end of the value chain. If that is precisely where markets are beginning to see the greatest uncertainty—as suggested by weaker valuations across parts of the software sector—the sustainability of continued AI-related capital spending becomes an increasingly important question.

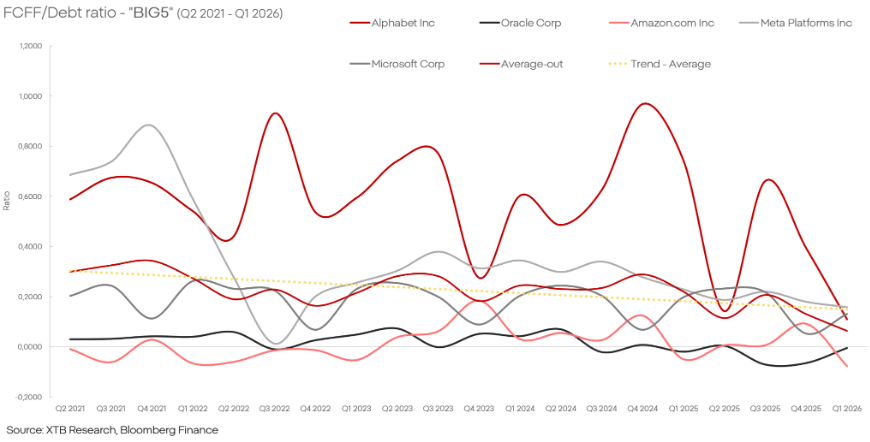

Debt Is Financing the Technology Arms Race

Rising investment spending is increasingly being financed through debt issuance and equity offerings. According to Morgan Stanley estimates, global debt issuance linked to AI investment could reach approximately $570 billion in 2026, representing nearly 100% year-over-year growth.

The scale of financing is remarkable. Nvidia completed a record bond offering, Amazon raised additional debt capital, Alphabet issued billions in debt and equity, while Oracle plans to commit tens of billions more toward expanding AI infrastructure.

Historically, periods characterized by rapidly rising leverage and financing activity on this scale have often preceded a reassessment of market expectations. On the other hand, the largest technology companies continue to generate enormous cash flows and maintain access to relatively inexpensive capital. Measuring the return on AI investments remains challenging, particularly because some of these expenditures may simply represent the cost of preserving competitive advantages and improving operational efficiency.

Will AI Follow the Path of Cloud Computing?

The bearish scenario assumes that AI spending ultimately proves excessive relative to future revenue generation, forcing companies to scale back investment and triggering a correction in valuations. Given today's spending levels and market valuations, this outcome cannot be dismissed.

However, there is another scenario - one that investors have witnessed before. Between 2010 and 2018, cloud-computing investments often appeared excessive, yet they ultimately laid the foundation for one of the most profitable segments of the modern digital economy.

The most important question today is therefore not whether artificial intelligence will reshape the global economy. That outcome increasingly appears inevitable. The real uncertainty lies in identifying which technology companies will successfully convert record investment spending into durable competitive advantages and superior shareholder returns. The rally among infrastructure providers has accelerated dramatically, yet it remains unclear which businesses will ultimately capture the greatest share of the economic value being created.

Eryk Szmyd Financial Markets Analyst, XTB

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.