Michael Burry, the investor known for correctly predicting the subprime crisis, has pointed to a further deterioration in Palantir’s situation. Burry has been an outspoken critic of the company’s valuation levels for quite some time. Palantir is one of the companies that, for now, are moving in line with the chief analyst’s forecasts. Since the beginning of the year, the company’s shares have already lost around 30%.

Technicals

In his latest posts, he indicated what he believes is a worsening technical picture for the company. Are these allegations justified?

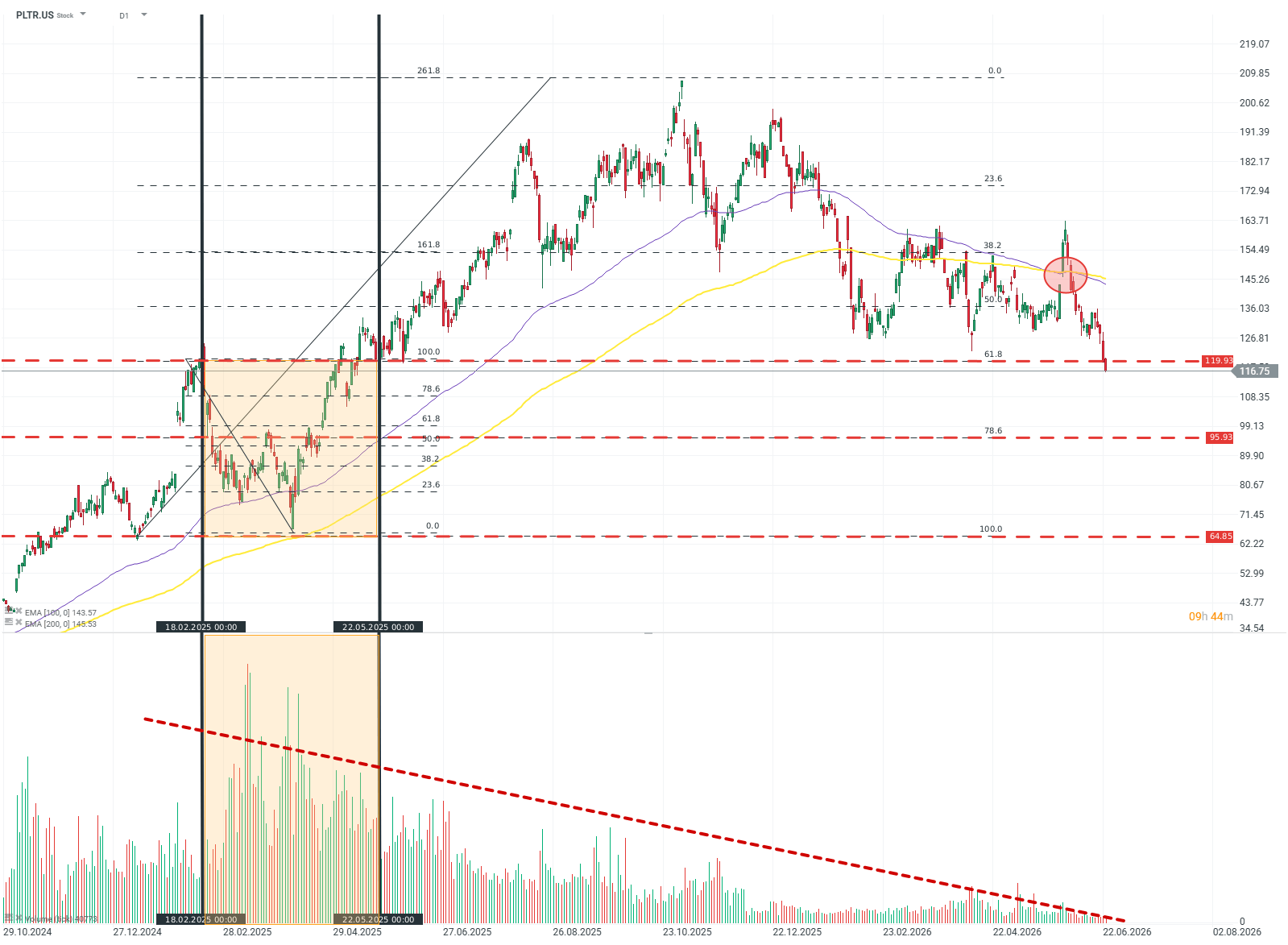

Burry noted that most of the volume was recorded “near the highs,” and that a downtrend accompanied by declining volume supports the thesis that bearish momentum will persist.

Source: xStation5

This view is not entirely consistent with reality. Looking at the chart, one can observe that peak volume occurred across a (fairly wide) price range between USD 118 and 65. After the company’s shares had already fallen by more than 40%, the price merely returned to the main range of that move.

Additionally, Burry tries to link weak volume with a “lack of interest” in the stock and further declines. This is an intuitive view, but from a technical-analysis perspective it is incorrect. A widely accepted theory in publications on this topic is that declining volume reduces, rather than increases, the “quality” and durability of price moves on a chart. Could this therefore signal an upcoming bullish correction?

Not necessarily. A much more important signal than falling volume is the “death cross” formed by the 100- and 200-period EMAs. The previous time such a signal appeared on the company’s chart was at the end of 2021, after which the stock lost about 60% of its value.

Fundamentals

Michael Burry also pointed to a number of fundamental issues. He mainly highlighted the company’s relatively “shallow moat,” especially given that it is a SaaS-type business, even if the company’s leadership may suggest otherwise. Another problem is that Palantir is alleged to engage in “aggressive revenue recognition” to synthetically improve its results. These are interesting observations, but are they correct?

The first argument is debatable. Burry presented no evidence of excessive reliance on third-party solutions. The company itself, meanwhile, offers a very unique set of services and has deep ties with governments and intelligence services around the world. If that kind of moat is shallow, then one has to ask how Burry defines its “depth.”

The allegation about aggressive revenue recognition is, however, false. Under financial audit and accounting standards, such practices are characterized by revenue growing faster than, or outpacing, receivables—in Palantir’s case it is the opposite. That signals an issue for the company, but of a completely different nature.

What’s behind the declines?

Most of the downward move observed in the stock’s valuation is a consequence of its nature. Above all, Palantir is a company often referred to as “hyper-growth,” with profit growth rarely seen even in the tech sector and similarly high margins, giving it enormous operating leverage and, as a result, high valuation multiples. This means that even the smallest disappointment during earnings releases can trigger a painful sell-off.

The second factor pressuring valuations is the SaaS segment the company belongs to. On the wave of the AI boom and the growing importance of agent/LLM-based solutions, the market has preemptively written off nearly all SaaS companies, without asking about the nature of or the real impact of the AI revolution on their business. Palantir is no exception.

Given the broader market context, breaking out of the downtrend and returning to the highs would be a major challenge—however, the USD 120–70 range is wide and provides plenty of opportunities to move into consolidation while waiting for more favorable investor sentiment.

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.