Textron is an American civil and military conglomerate that focuses on the aerospace sector with brands such as Bell, Aircraft Armaments, Lycoming Engines, Cessna, Beechcraft and Pipistrel. The company has undergone deep restructuring since the 2008 crisis with the appointment of Scott C. Donnelly as its new CEO, who continues to successfully grow the business. Textron has been increasingly involved in the development of the private and civil aviation market, and its Q1 2022 results presented by the company far exceeded analysts' expectations:

-

Textron's share price posted a double-digit gain after the results were presented, however, Friday's weakest US session since 2020 resulted in a sell-off of the company's shares, with its valuation moving back below $70 per share. Earnings per share (EPS) for Q1 came in at 0.88 USD versus analysts' forecasts of 0.74 USD. Total revenue for the quarter was over 3 billion USD;

-

Textron's Aviation revenue for Q1 was over 1 billion USD, up 175 million USD from Q1 2021. Textron Aviation division's Q1 2022 profit was 121 million USD vs. 47 million USD profit in Q1 2021, representing nearly 250% growth and higher net margin;

-

Textron delivered a total of 39 jets and 31 commercial turboprop aircraft in Q1 2022 versus 28 jets and 14 turboprops in Q1 2021. The Bell division delivered 25 helicopters versus 17 in the same quarter last year. The statistics confirm the increase in demand for the company's products;

-

The company is very actively involved in the development of private civil aviation through its well-known Cessna and Beechcraft aircraft brands. The Beechcraft brand is best known for its business models Super King Air (the longest production turboprop) and Starship 2000. Textron has recently seen record interest in Cessna aircraft, of which the Citation series models are particularly popular (the X model is currently the fastest passenger aircraft and the largest Cessna brand aircraft). Both brands also have military versions of the aircraft models;

-

In March 2022, Textron made a strategic acquisition of Slovenian aircraft manufacturer Pipistrel for approximately 235 million USD as part of Textron's eAviation business. The company intends to make a long-term commitment to increase production and distribution of civil electric aircraft. The outlook for the electric air transport industry looks promising. Pipistrel became the first company in the world to obtain a license for the introduction of an electric aircraft in the form of the two-seat Virus model, with prices starting at 65,000 EUR. Textron also received Federal Aviation Administration (FAA) certification in the first quarter for its new Cessna SkyCourier twin-engine turboprop aircraft.

Textron CEO Scott Donnelly was optimistic about the civil aircraft market on April 28 following the release of quarterly results: "We continue to see very strong demand, stable pricing, increased deliveries of our Citation jets and commercial turboprop aircraft and higher aftermarket volume resulting from increased aircraft utilization."

-

Textron is participating in a number of procurements as part of the U.S. weapons systems modernization effort: Next Generation Squad Weapon, Next Generation Squad Automatic Rifle, Next Generation Cased Telescoped Ammunition, Advanced Reconnaissance Vehicle (Bell 360 Invictus helicopter), Long Range Air Assault and Future Vertical Lift (AH-280 Valor rotorcraft). These programs have a very important role in developing the Pentagon's capabilities, the modernization of the army has taken on particular importance in the face of Russian aggression and the crisis in relations with China. The United States plans to eventually move away from attack helicopters such as the Apache or Viper in favour of attack helicopters with better technical parameters and combat capabilities. Bell already provides one of the primary rotorcraft for the US Army, the V-22 Osprey model;

-

The purchase of Bell's AH-1Z Viper helicopters is being considered as part of a long-awaited tender for helicopters for the Polish Army, the competition of course being Apache helicopters. The winner of the tender is expected to be selected later this year due to the urgent need to increase the Polish defence capabilities (KRUK programme);

-

Textron supplies one of the most widely used drones by the US Army, the RQ7 Shadow model. UAVs (Unmanned Aerial Vehicle) are developed by Textron's subsidiary Aircraft Armaments which specializes exclusively in the construction of unmanned systems;

-

Back in 1985, Textron made a strategic acquisition of the Lycoming brand, one of America's leading suppliers of engines to the aviation industry. The company has more than 700 FAA-licensed engine models and has supplied more than 300,000 engines since its inception for use in a significant portion of the world's aircraft and helicopter fleet. Textron also owns the Able Aerospace Services brand, which performs FAA-licensed repair and parts service;

-

While primarily engaged in the aerospace industry, Textron also owns brands primarily known in the U.S. market such as Jacobsen (manufacturer of tractors and garden equipment), ArcticCat (snowmobiles and ATVs), and E-Z GO (vehicles used on golf courses).

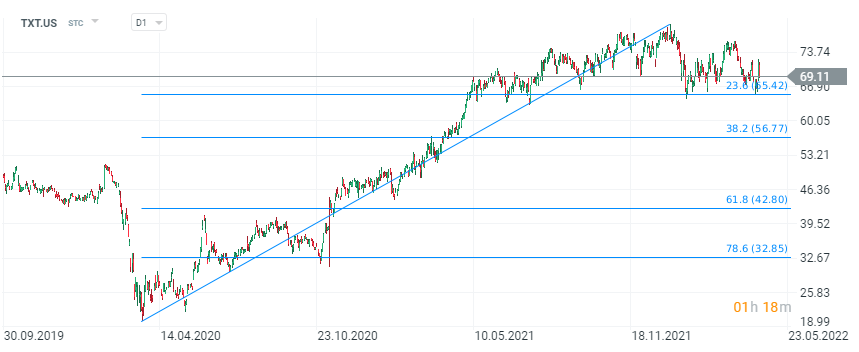

Textron (TXT.US) shares, D1 interval. The company's share price has risen nearly 350% from the price lows caused by the outbreak of the coronavirus pandemic. Recently, however, declines have twice stopped in the area of 66 USD, which coincides with the 23.6 Fibonacci retracement. This zone may provide a base for further growth. At the same time, exactly this zone seems to be crucial for the further price behavior at the moment, as a drop below 65 USD could mean the advantage of supply. Sellers may then try to pull back the valuation below 56 USD, which coincides with the 38.2 Fibo retracement. At the same time, it is worth noting that the price-to-book ratio for Textron compares favorably with the largest companies in the US defense and aerospace industries. Currently P/B Ratio is 2.33 vs. 3.76 of General Dynamics, 8.04 of Airbus or 11.78 of Lockheed Martin. Source: xStation5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Moderna shares slide despite mFlusiva success 📉 What's next for the mRNA vaccines market giant?

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.