The US dollar has not had a very good run lately. Slightly weaker data from the economy, especially from the real estate market, and a more hawkish attitude from other central banks have weakened the world's most important currency. Expectations for interest rate hikes have fallen somewhat, but it seems that the Fed is not changing direction for now. The FOMC minutes may confirm this.

Let's get ready for two double hikes

• FOMC Minutes are likely to confirm the desire for two 50bp rate hikes in June and July

• Further fate of the increases will depend on inflation and inflation expectations

• Market hopes that inflation has already peaked and will fall from the recent 8.3%

• Market expectations for hikes have weakened. Currently, 95% of a 50bp hike in July is being priced in and only 30% of a 50bp hike in September

In terms of expectations for hikes, the minutes should not change market sentiment. Of course, there is a chance to present a clear plan of how the Fed will react to weakening or even accelerating inflation. The market will also be looking for an answer to the question of what's next for hikes after the neutral interest rate, which is estimated at 2.5% and is possible even this year.

Will the Fed be forced to sell assets?

• At the May meeting, the decision was made to begin a balance sheet reduction program

• The Fed will reduce its balance sheet by USD 47.5 billion per month for 3 months: USD 30 billion government bonds and USD 17.5 billion MBS (mortgage-backed securities)

• Starting in September, the Fed will reduce its balance sheet by 95 billion USD: 30 billion USD government bonds and 35 MBS

• It appears that the Fed may be forced to sell MBSs, due to too few maturities. Additionally, it may do so at lower prices, realizing a loss

The market will be waiting for more details on the balance sheet reduction program. In terms of government bonds, we should rather not expect more comments (although there is a risk of further increase in yields, which may force e.g. Japan and China to sell off their reserves). The market will focus on the outlook for MBS. It is estimated that the monthly maturity of these securities may be as low as $20 billion, which would mean that the Fed would have to sell its securities to meet its reduction target. Furthermore, mortgage overpayments in the U.S. are projected to decline due to rising interest rates, which could lead to a drop in MBS prices. In that case, the Fed could sell MBS at a loss. Williams from the New York Fed confirmed that there could be a problem with MBS reduction and the Fed may have to sell these securities.

What does this mean for the market?

If the Fed sells assets, it will be a very good sign for the dollar. Theoretically, the stock market should not react strongly to this information, but if it worsens consumer sentiment, Wall Street may score a continuation of declines. On the other hand, if the Fed does not provide any new information, it should be perceived as a dovish event. Then the Dollar may return to weakness and the stock market should receive support due to the fact that the Fed has no concrete plan for further tightening.

EURUSD is rebounding strongly for the 2nd week in a row. Key resistance is around the 1.0800 level. Lack of new guidance for monetary tightening may prolong dollar weakness. On the other hand, if the Fed is forced to sell assets, the dollar should clearly react with a return to appreciation. Source: xStation5

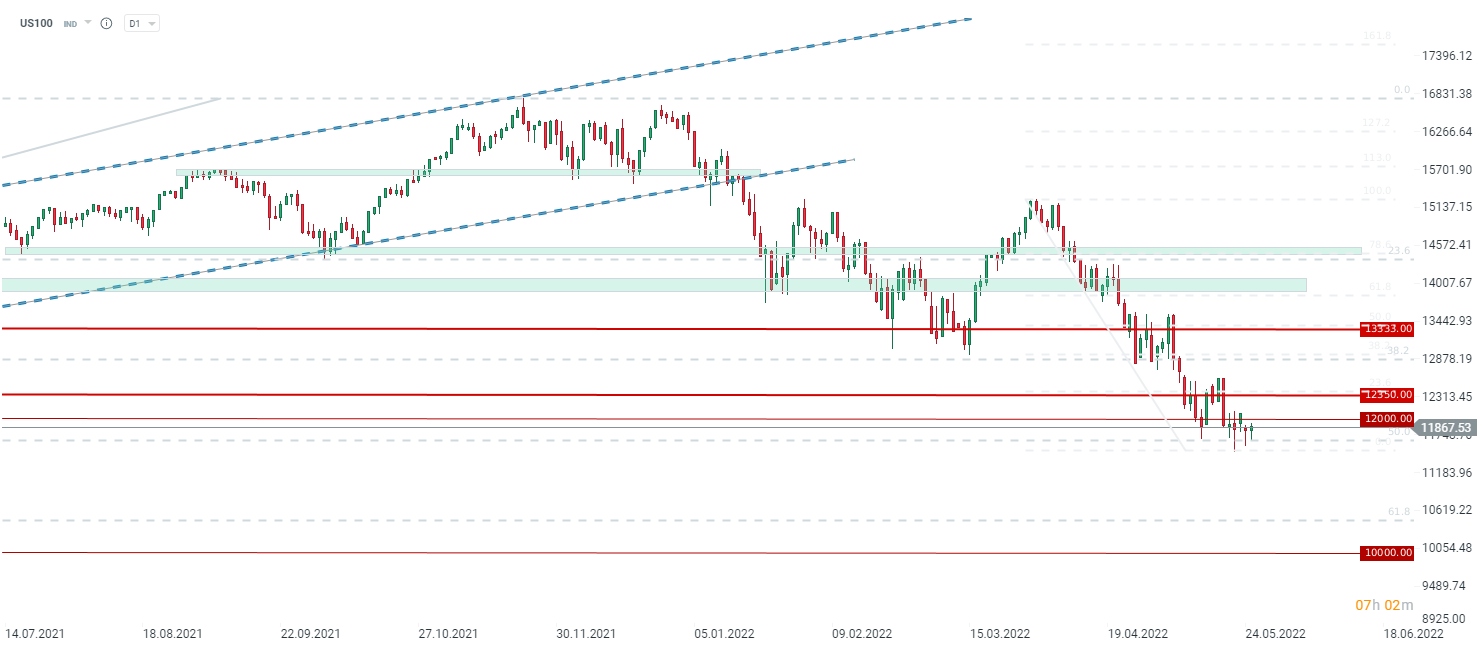

US100 is trying to find a new low and is holding important support all the time. The key for the bulls is to go above the 12000-12300 points zone. The lack of new tightening guidance should help Wall Street. On the other hand, the economy is starting to send worrying signals. A further strong fight of the Fed against inflation, e.g. in the form of asset sales, would be perceived negatively by the Wall Street. Source: xStation5

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

Nasdaq Gains 0.6% and Reclaims 29,000 🔼 Strong Results from ON Semiconductor and Palantir

🗽 US500 sets a new record high

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.