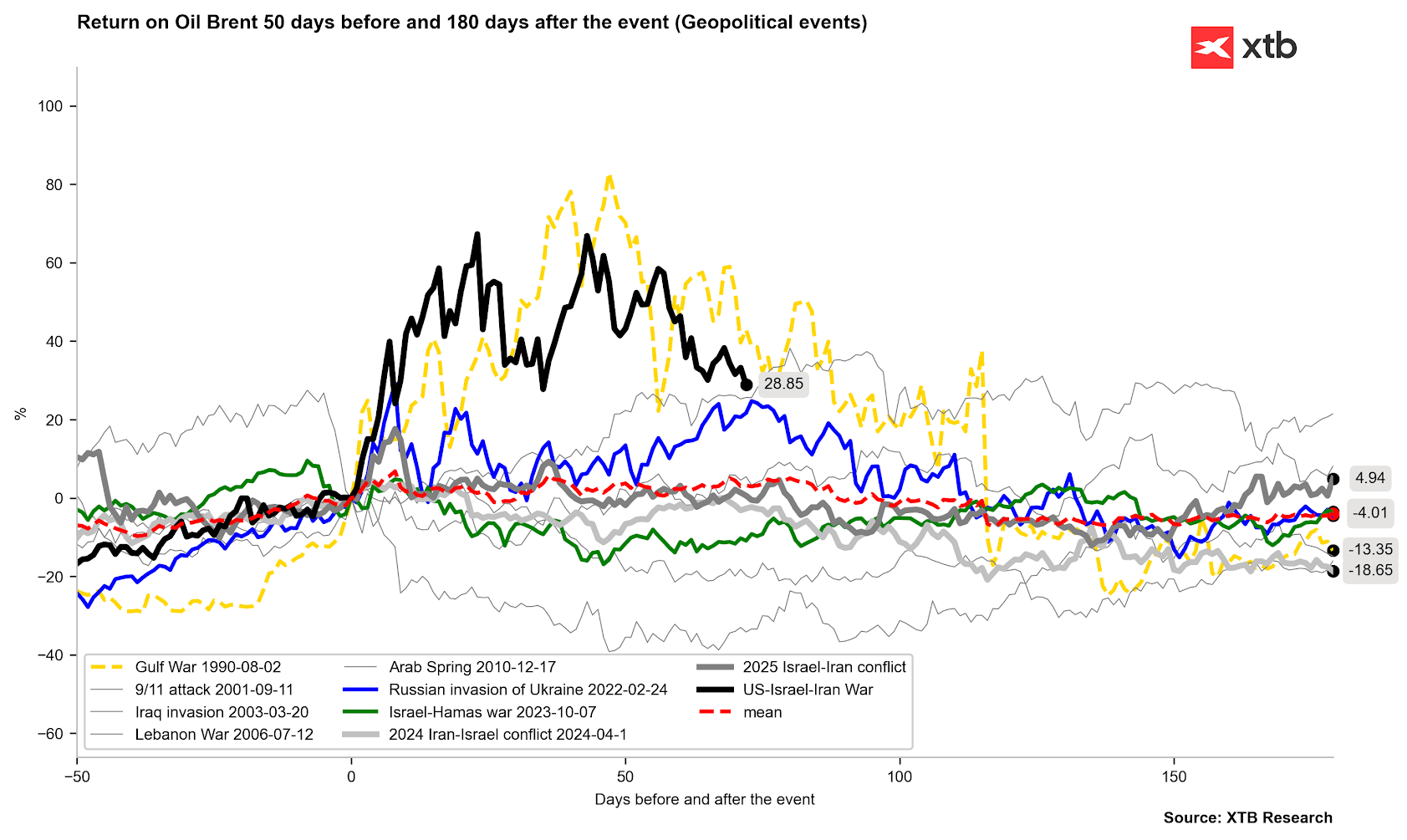

Price Drop Below 90 USD and Multi-Week Lows

Crude oil prices have recorded a significant decline in recent hours, pushing US WTI crude quotes below the psychological barrier of 90 USD per barrel. The current price drops already amount to over 4%. The main impulse for the declines is the intensifying hope for a convergence of positions between the US and Iran regarding the end of the conflict, which has weighed on global markets for months.

This reduction has noticeably eased investors' concerns about high energy costs, which had previously fueled inflationary pressures. At the same time, however, it is worth noting that the drop in oil prices is not improving sentiment in other markets. We are also seeing a clear pullback in Wall Street indices and a pullback in prices in the precious metals market, even despite the potentially diminishing inflationary pressure.

Has Oil Already Peaked?

Many factors may indicate that the price peaks are already behind us, although, of course, the risk of a physical deficit in the fuel market is still present, as the Strait of Hormuz remains closed. As markets price in progress in peace talks and the prospect of averting military conflict, the so-called geopolitical premium is successively evaporating from oil pricing.

A lasting diplomatic agreement will likely seal this trend, preventing a return to recent extreme highs. On the other hand, markets have been living on the hope of ending the conflict for many weeks, and the high prices themselves are being mitigated by a clear decline in global crude oil inventories.

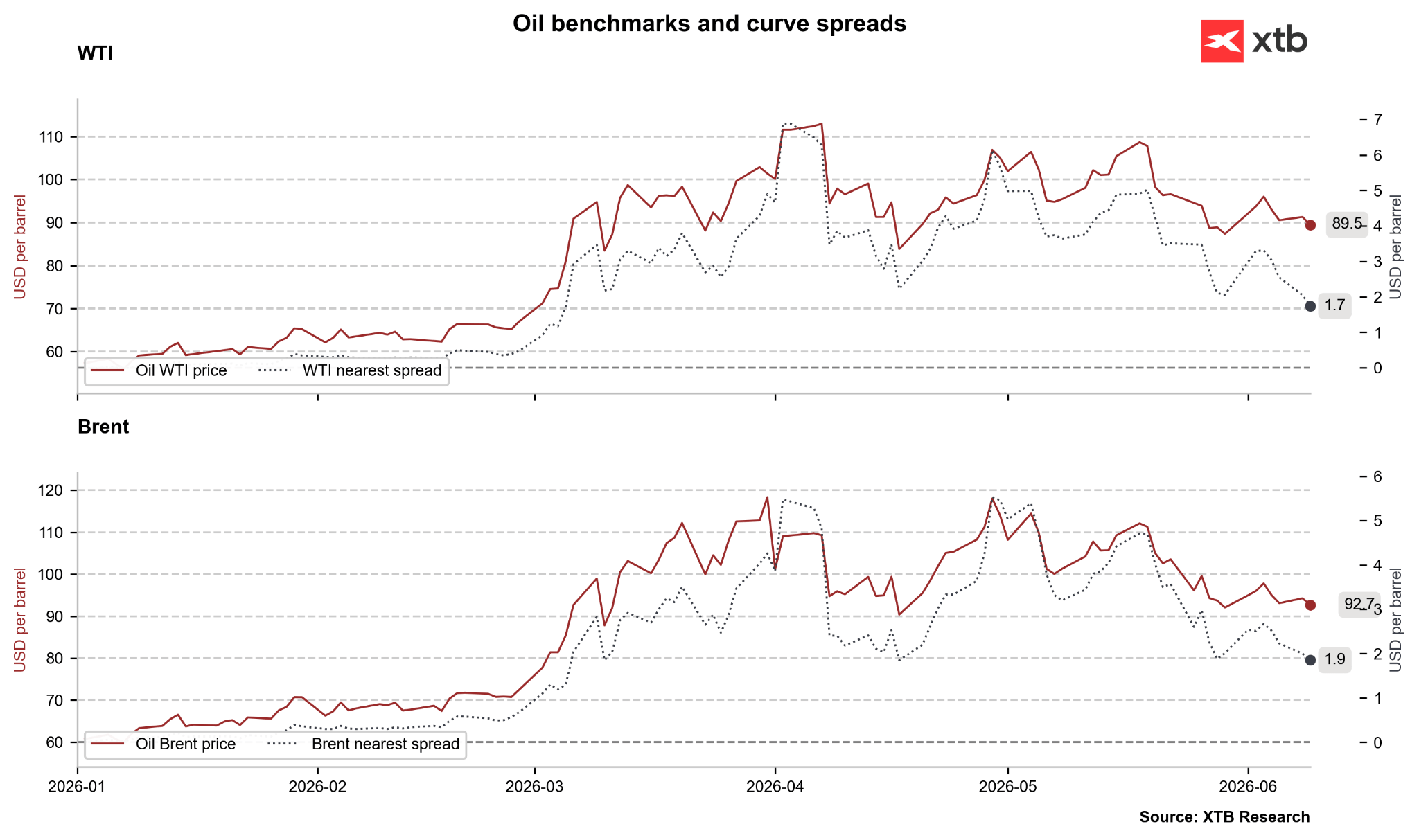

Calendar Spreads Below 2 USD Despite Structural Deficit

The observed decline in calendar spreads below the 2 dollar mark is a technical signal of calming sentiment in the futures market. Such spread compression is typical for a normalization phase, where investors stop paying an exorbitant premium for immediate delivery. Although the 1–2 USD level in a historical context still indicates a tight market, it is far from the 5–6 or even 10 dollar levels we observed in previous months.

Worryingly, however, we are dealing with a clear disconnect between the paper and physical markets. Although futures spreads suggest a return to equilibrium, the real physical market is still stuck in a deep supply deficit after months of turning off the taps and logistical disruptions. This massive deficit makes the market extremely tight, which should provide firm support for prices. It seems that even if a real agreement is signed, the price drop from current levels should be limited to around 10%.

Trump's Rhetoric Versus Diplomatic Reality

President Donald Trump has once again injected a dose of optimism into the market, announcing a breakthrough after negotiating a halt to the exchange of blows between Israel and Iran:

"We are in the final stages of what will be a very, very good deal," Trump told reporters in New York, suggesting that specific outlines of an agreement could emerge within one or two days.

Although financial markets reacted to these words with an immediate drop in commodity prices, investors are approaching these declarations with justified skepticism. In recent weeks, the president has mentioned "imminent success" and a "deal within reach" over thirty times, treating these announcements as part of negotiation leverage and PR gameplay. This time, however, optimism has somewhat stronger foundations, as the actual halting of hostile military actions gives diplomats real room to maneuver.

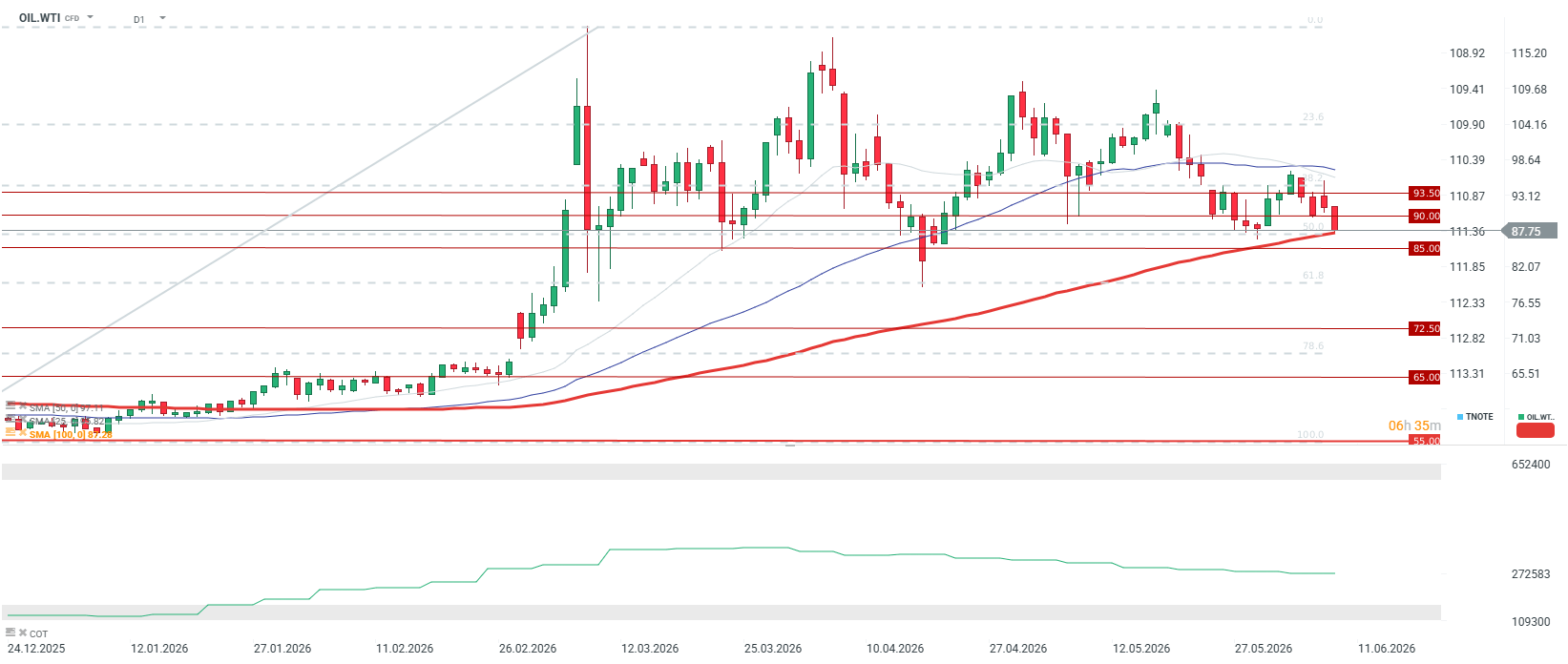

The price of WTI crude oil is falling below 90 USD and is currently testing the 200-session average. This is a key support level. In 2022, after finally breaking below this level, a significant multi-month correction occurred.

Source: xStation5

Source: xStation5

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.