At the intersection of geopolitics and financial markets, the most intriguing paradox of the modern semiconductor sector is unfolding. The official policy of global superpowers has collided with the brutal reality of market demand, creating a tryst-like impasse between Washington, Beijing, and Nvidia. Instead of a complete decoupling of both economies, we are witnessing a hybrid model of interdependence, where official political narratives completely diverge from the actual needs of the economy and the defense sector.

A Game of Shadows: Official Blockade vs. Military Smuggling

On one hand, Beijing is forcing the development of domestic AI capabilities, ordering local businesses to independent themselves from Western tech and heavily backing domestic players like Huawei. On the other hand, reality ruthlessly exposes the massive technological gap that still separates China from the West. Recent media reports confirm that entities directly linked to the Chinese military and elite defense universities are actively seeking ways to acquire Nvidia chips through unofficial channels. This clearly demonstrates that for critical military applications and scientific data analysis, American silicon remains simply irreplaceable at this moment.

A Three-Way Market Impass

This deep divide creates a fundamental market tension, with each key player moving in completely opposite directions. US-based Nvidia aims to maintain access to one of the largest and most lucrative target markets in the world. Chinese buyers, regardless of political barriers and official decrees from their own government, desperately need American technology to avoid losing the AI arms race. Meanwhile, the US administration rigorously blocks the transfer of the latest silicon architectures, treating them as an absolute priority for national security.

The Global Supply Chain Knows No Borders

An additional piece of this complex puzzle comes from sobering assessments straight from within the semiconductor industry itself. The CEO of Arm Holdings pointed out that a total ban on AI technology exports to China might prove practically unfeasible for the US government. The global, highly fragmented trade structure, an extensive network of third-country intermediaries, and the growing capacity of Asian entities to bypass restrictions (e.g., via cloud leasing) render 100% control over the flow of advanced chips an illusion.

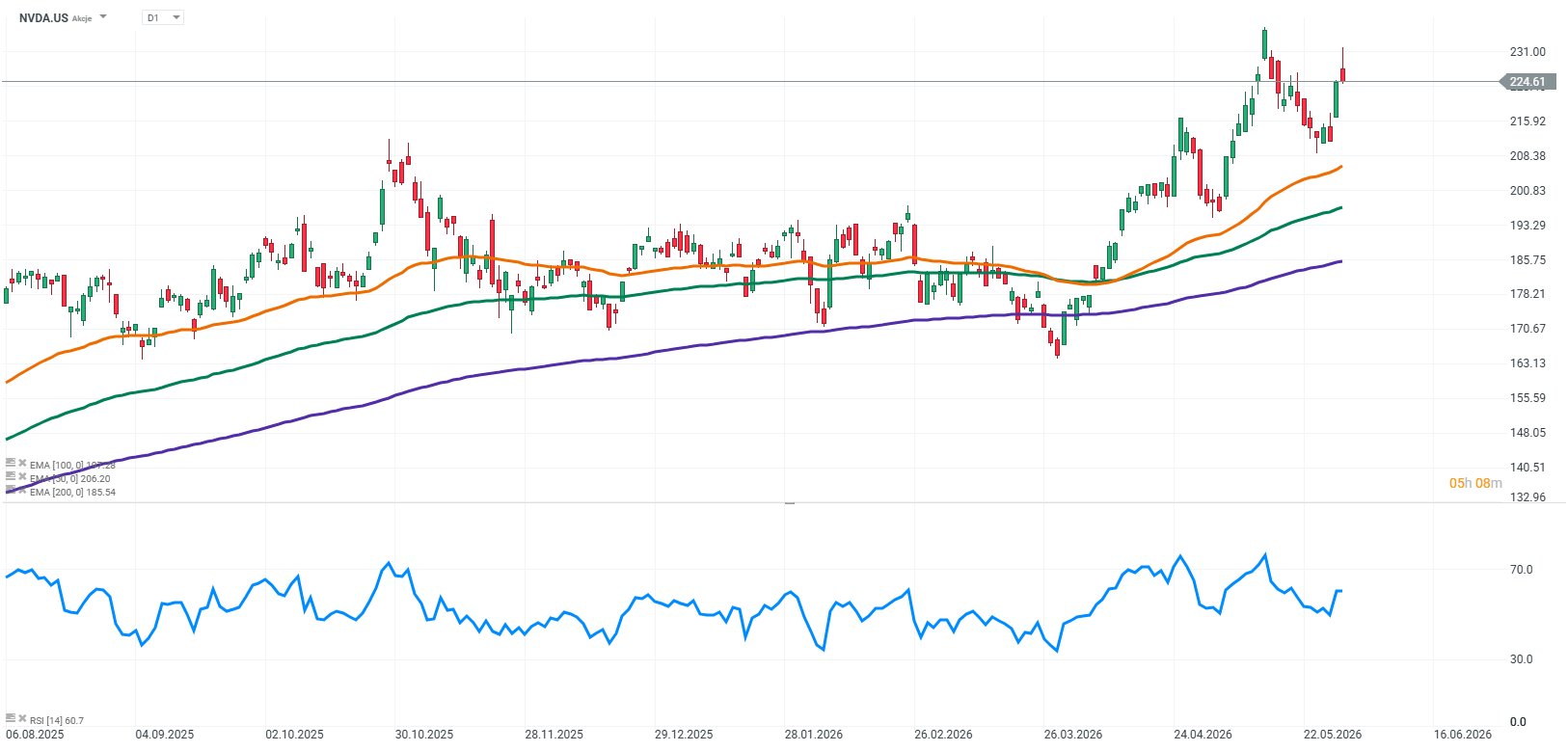

The Bull Case: Nvidia's Structural Advantage

For growth-oriented investors, the situation in China serves as ultimate proof of the massive, almost unreplicable economic moat surrounding Nvidia. Demand for Blackwell or H200 series architectures is fundamental and, at least for now, irreplaceable. Since the Chinese military prefers risking an international scandal to buy these products on the black market rather than utilizing readily available domestic alternatives, it sends a clear signal to NVDA shareholders that the company's leadership remains entirely unchallenged. If demand cannot fit into official distribution channels, the market finds a way regardless.

The Bear Case: Regulatory and Political Risks

However, more cautious investors must remember that this geopolitical gridlock generates massive long-term risks. Every subsequent report of Beijing bypassing sanctions will force Washington to introduce even harsher restrictions, penalize intermediaries, and tighten export blockades. Even though demand in China is immense, being officially cut off from legal revenue in this market forces Nvidia into a perpetual balancing act on the edge of compliance. Should the US-China conflict escalate further, it could trigger sudden and deep volatility in the company's stock price.

Source: xStation5

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

US Open: AMD and SpaceX failed to impress, but the broader market remains resilient

Shopify earnings: "Monstrous quarter"

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.