The 10-year Treasury futures (TNOTE) tumbled 0.6% to their lowest level since April 2025 as investors recalibrate the monetary outlook. Markets are aggressively repricing for a more hawkish Fed, fueled by accelerating inflation and the diplomatic stalemate following the Trump-Xi summit.

TNOTE contract dipped below all three exponential moving averages (EMA100, EMA30, EMA10), enforcing the bearish momentum as RSI is still trading above the key 30 level. Source: xStation5

Yields Hit Multi-Year Highs

The 30-year Treasury yield surged to 5.117%, its highest level since May 2025, as markets aggressively repriced risk to inflation. This spike serves as a "baptism by fire" for newly confirmed Fed Chair Kevin Warsh, who must now navigate policy as long-end rates increasingly take control of financial conditions.

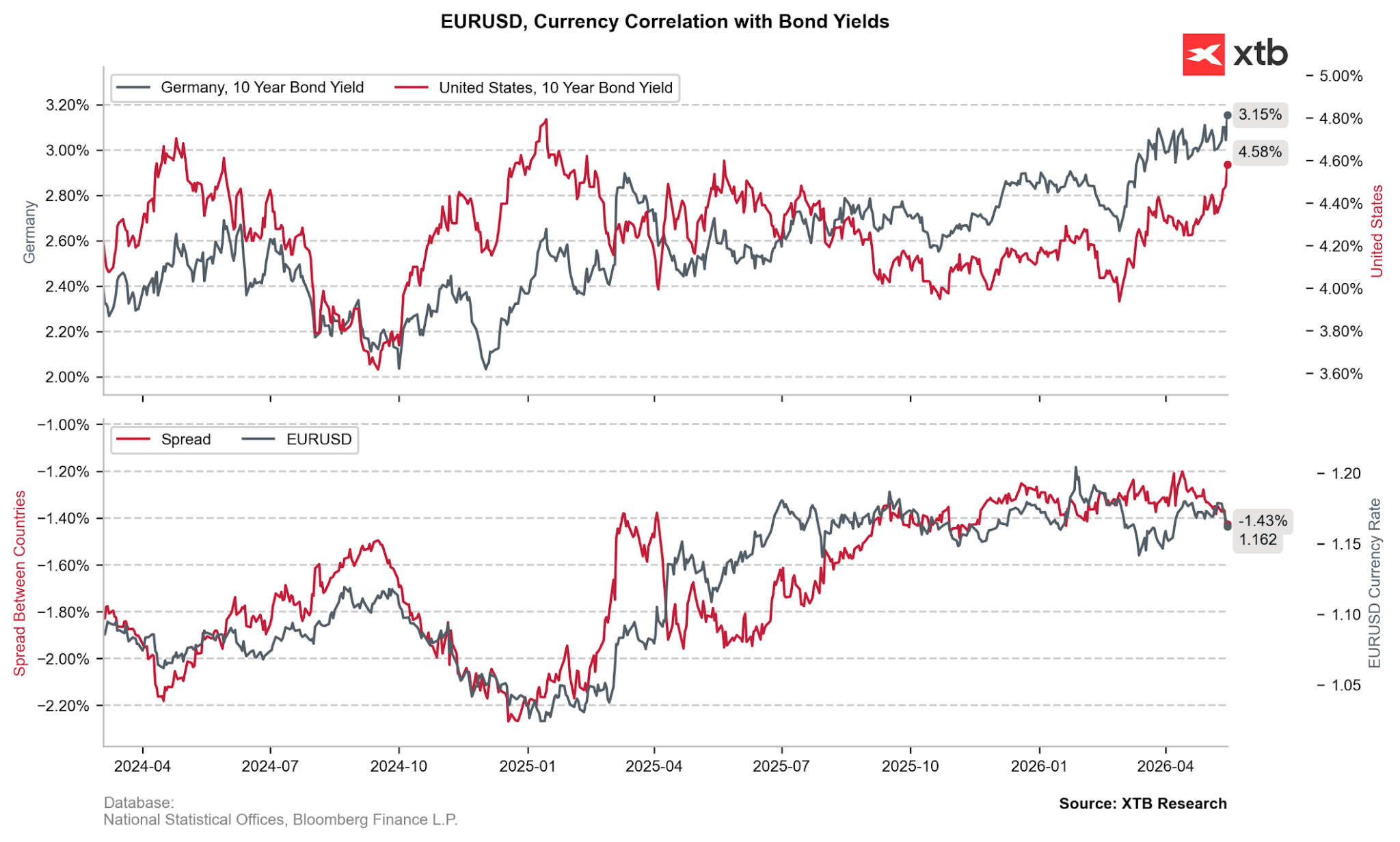

The record highs on US bond yields are outpacing similar trends in other countries, reigniting dollar's strength after the Trump-Xi summit. Source: XTB Research.

Hot Inflationary Data

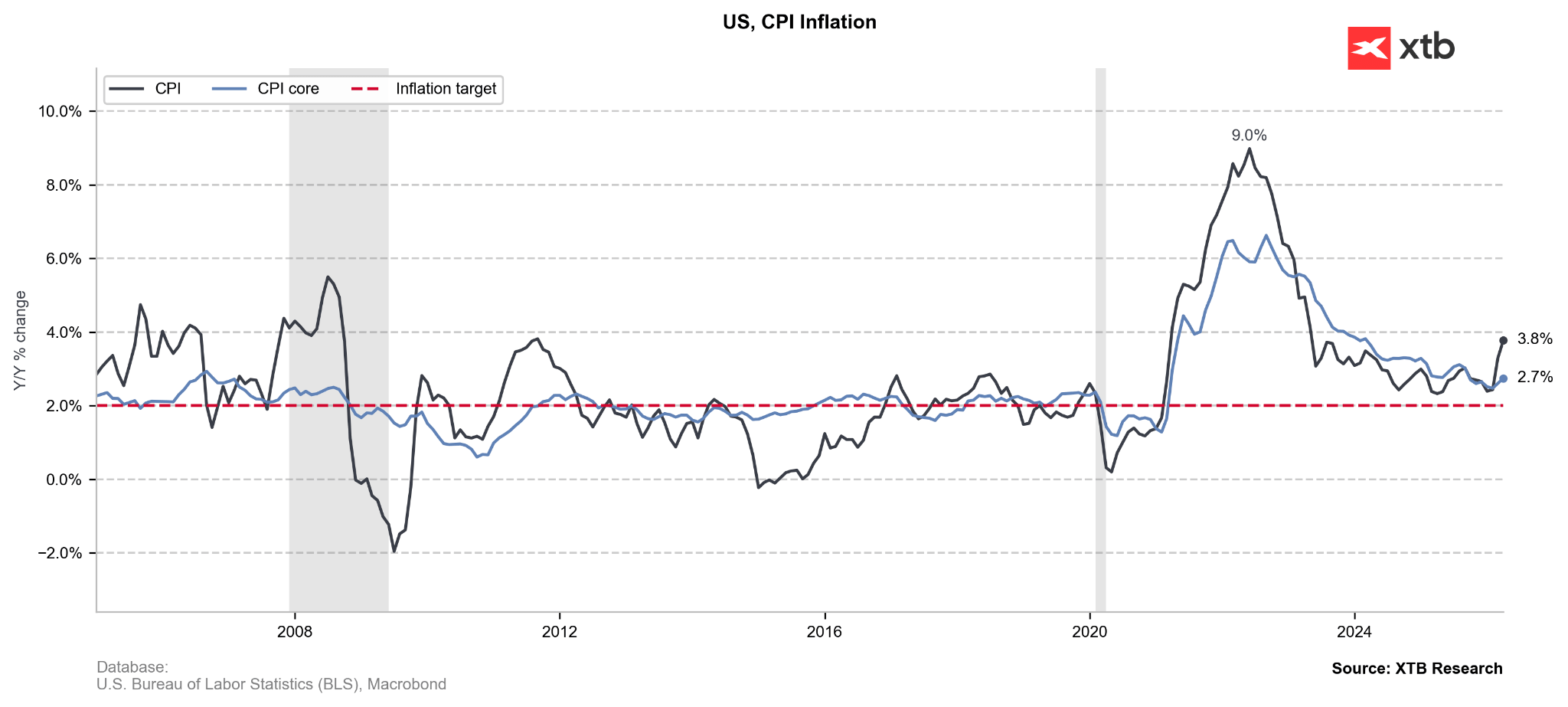

A string of "messy" reports—including 3.8% CPI, a 6% PPI annual rate, and the largest import price jump since 2022—confirms that Middle East tensions are filtering through to wholesale and consumer costs. This data makes President Trump’s calls for rate cuts increasingly difficult for the Fed to justify.

CPI is already far away from Fed’s yearly inflation (PCE) projection (2,7%). Source: XTB Research

Failed Diplomatic Momentum

Energy prices climbed again (WTI over $104) after the Trump-Xi summit concluded without a concrete breakthrough for the Iran conflict. Investors are "pricing in the pain" of a prolonged blockade, viewing the lack of diplomatic progress as a direct catalyst for sustained high energy and transport costs.

OIL.WTI extends above the 10-day exponential moving average (EMA10, yellow). Source: xStation5

Global Fiscal Pressure

The sell-off isn't limited to the U.S.; yields on German Bunds, UK Gilts, and Japanese bonds also spiked. Domestically, the U.S. fiscal situation is worsening, with interest payments on the national debt now the second-largest government expenditure after Social Security, further unsettling bondholders.

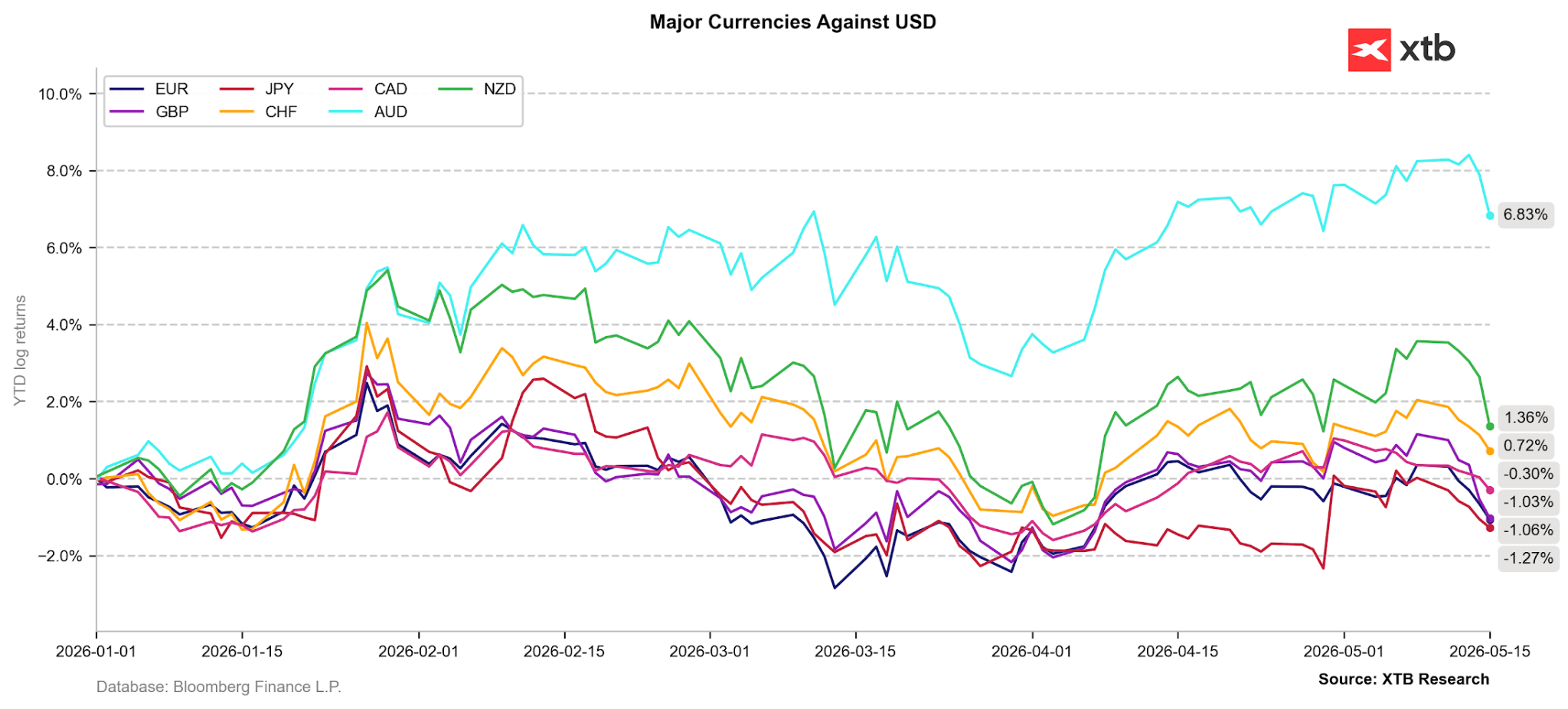

The worldwide worries on bond markets, though symmetric, fuel the dollar as investors’ preferred safe haven, causing a major weakness in other G10 currencies, who have been recovering against USD on April’s Iran war optimism. Source: XTB Reseach

Wheat extends correction, falls to its lowest level since July 10 🚩 Drought, El Niño and the Black Sea in focus

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.