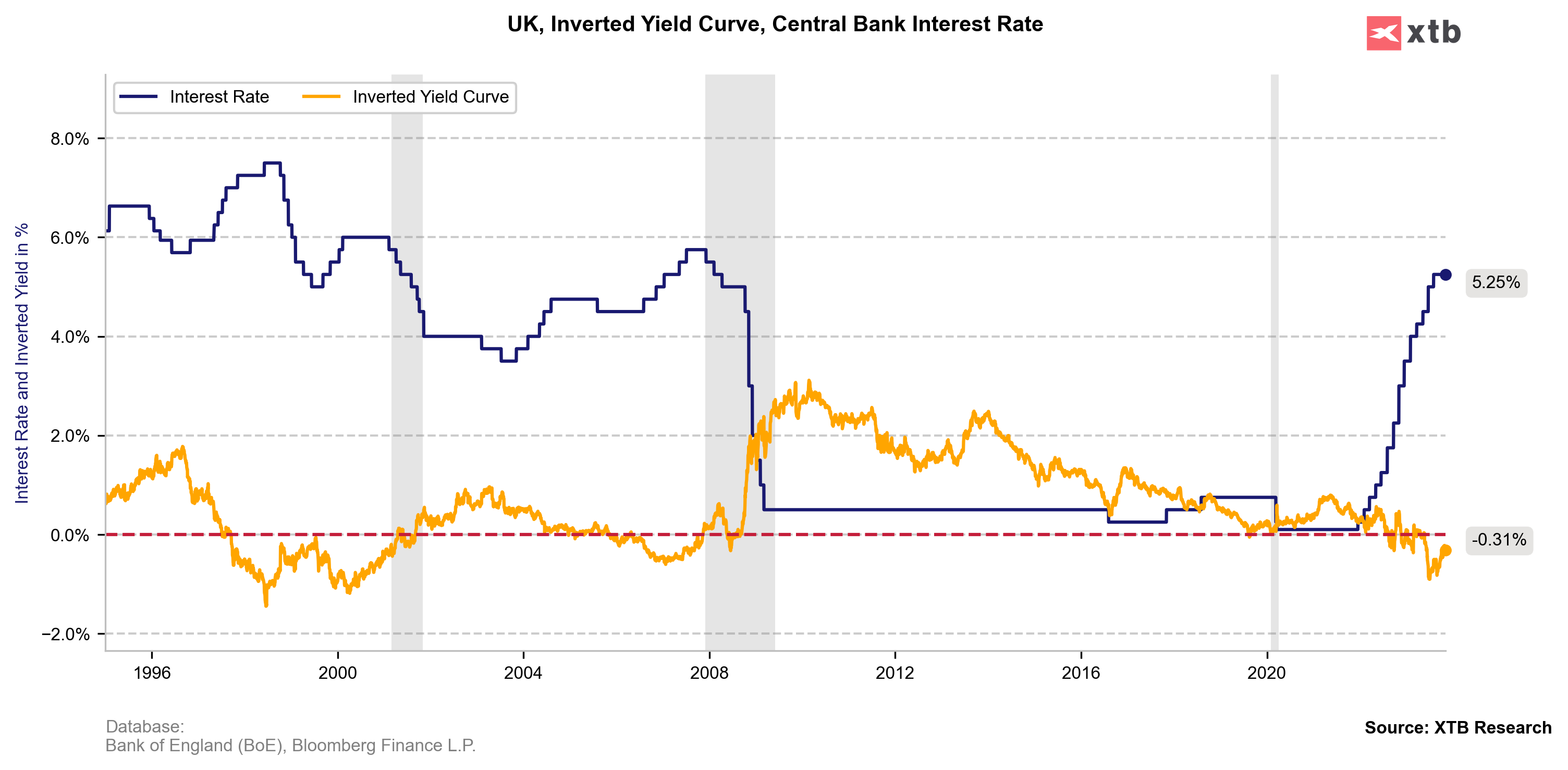

Bank of England announced its latest monetary policy decision today at 12:00 pm GMT. The consensus of the markets was in favor of the BoE keeping interest rates unchanged at 5.25% for the second consecutive time. The actual decision turned out to be in line with these expectations.

Bank of England's Monetary Policy Committee (MPC) voted by a majority of 6–3 to maintain the Bank Rate at 5.25%, with a minority favoring a hike to 5.5%. The Committee's projections, based on market expectations, suggest the Bank Rate will hold around 5.25% until Q3 2024 before gradually declining to 4.25% by the end of 2026. This is higher for longer outlook that previously expected by the markets, which probably triggered bullish reaction on GBP currency.

- Market rates imply less BoE tightening than August, show bank rate at 5.3% in Q4 2023, 5.1% in Q4 2024, 4.5% in Q4 2025 (August: 5.8% in Q4 2023, 5.9% in Q4 2024, 5.0% in Q4 2025)

-

BoE: We estimate wage growth 6.75% yy in Q4 2023 (August: 6%), Q4 2024 4.25% (August: 3.5%); Q4 2025 2.75% (August: 2.5%)

-

BoE estimates GDP in 2023 +0.5% (August forecast: +0.5%), 2024 0% (August +0.5%), 2025 +0.25% (August: +0.25%), based on market rates

-

BoE estimates unemployment rate 4.3% in q4 2023% (August: 4.1%); q4 2024 4.7% (August: 4.5%); q4 2025 5.0% (August: 4.8%)

-

BoE sees inflation first falling below 2% target in Q4 2025 (August: Q2 2025), based on market rates and modal forecast

The UK's CPI inflation dropped to 6.7%, below expectations, yet remains above the 2% target. Inflation is anticipated to decline sharply, returning to the target by the end of 2025 and then falling below it. The MPC acknowledges risks of inflation persisting longer than expected, primarily due to wage-price effects and potential rises in energy prices. The MPC's stance remains restrictive, emphasizing the need to be sufficiently restrictive for a prolonged period to sustainably return inflation to the 2% target. The outlook suggests continued restrictive monetary policy, with further tightening possible if persistent inflationary pressures are observed.

Source: xStation 5

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.