Kevin Warsh’s appointment as the new Chair of the Federal Reserve opens a new chapter in US monetary policy, but it also places him in an extremely difficult position. For months, Donald Trump has openly called for immediate interest rate cuts, arguing that borrowing costs remain too high and are holding back the economy. The problem, however, is that current macroeconomic conditions leave the Fed with very little room to maneuver.

The latest CPI and PPI inflation readings for April came in even higher than economists’ already revised forecasts, reinforcing the view that inflationary pressure in the US economy remains strong. Under such conditions, rapid rate cuts would be difficult to justify from an economic standpoint and could easily be perceived as a political decision rather than a data driven one.

This is where the biggest risk for Warsh begins to emerge. If the new Fed Chair attempted to repay Trump for his political support by pushing for rate cuts despite persistent inflation, he would immediately face accusations of compromising the central bank’s independence. For financial markets, this would signal that the Fed is beginning to follow the expectations of the White House rather than macroeconomic data. Such a scenario could undermine the credibility of the entire institution.

Moreover, even the Fed Chair does not have complete freedom of action. Decisions on interest rates are made collectively by the FOMC, including other governors and presidents of regional Federal Reserve banks. This means Warsh would not be able to force through rate cuts on his own if the rest of the committee believes inflation remains too high.

A far more likely scenario is that Warsh will attempt to reshape the Fed in a different way by continuing to reduce the central bank’s balance sheet. This is an issue he has spoken about repeatedly even before his nomination. Warsh has long criticized the massive expansion of the Fed’s assets following recent crises and believes the central bank has become too deeply involved in financial markets.

At the same time, geopolitical tensions are making the situation even more complicated for the new Chair. The ongoing conflict in the Persian Gulf continues to keep oil and energy prices elevated, which in turn fuels inflationary pressure. As long as energy prices remain high, the Fed will have limited room to ease monetary policy without risking another acceleration in inflation. The bond market is already signaling concerns that inflation and elevated yields could remain in place for much longer.

Warsh is therefore stepping into the Fed at an exceptionally difficult moment, caught between political pressure from Trump and the harsh reality of persistent inflation. It will quickly become clear whether he intends to act primarily as a loyal presidential appointee or as an independent guardian of US monetary stability.

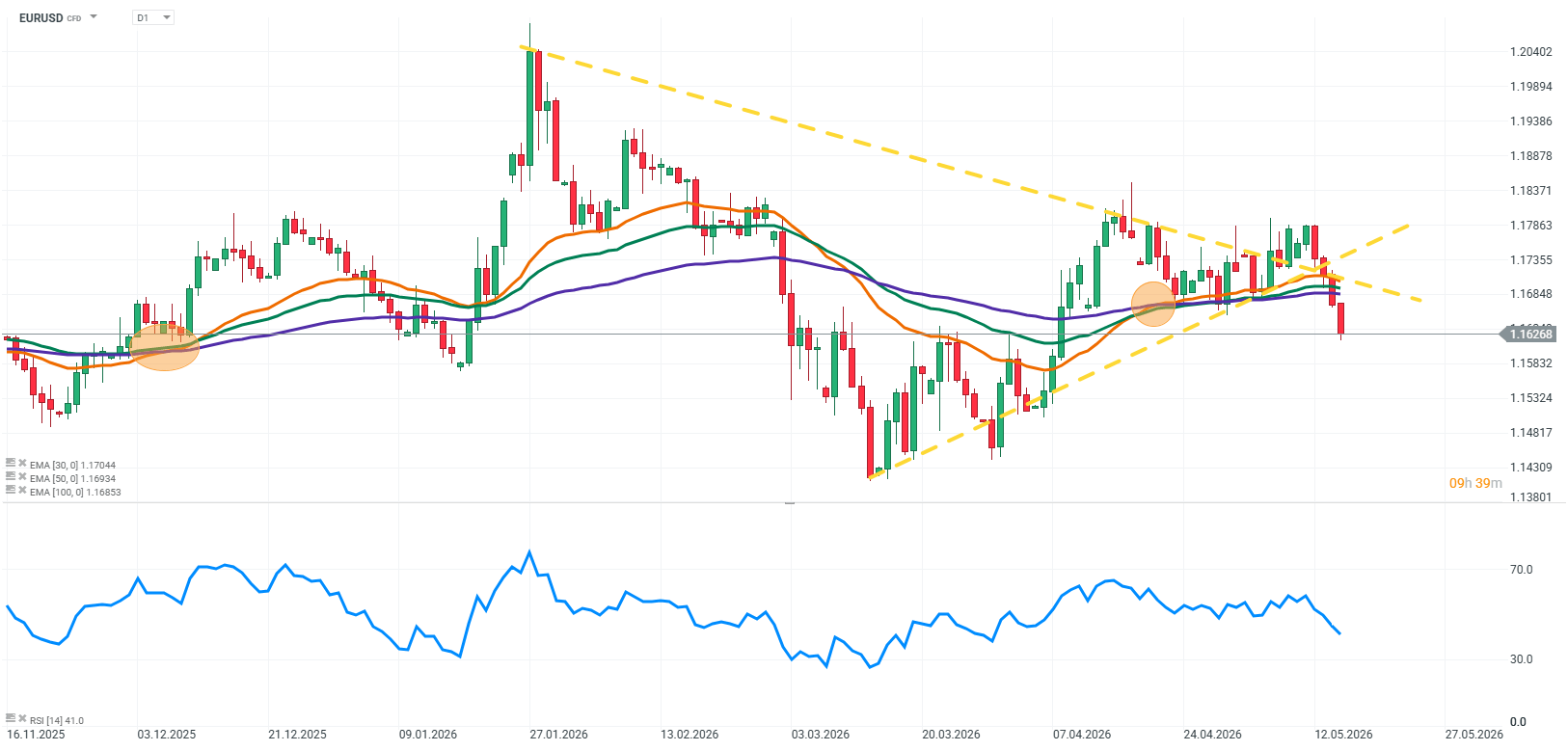

Source: xStation5

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.