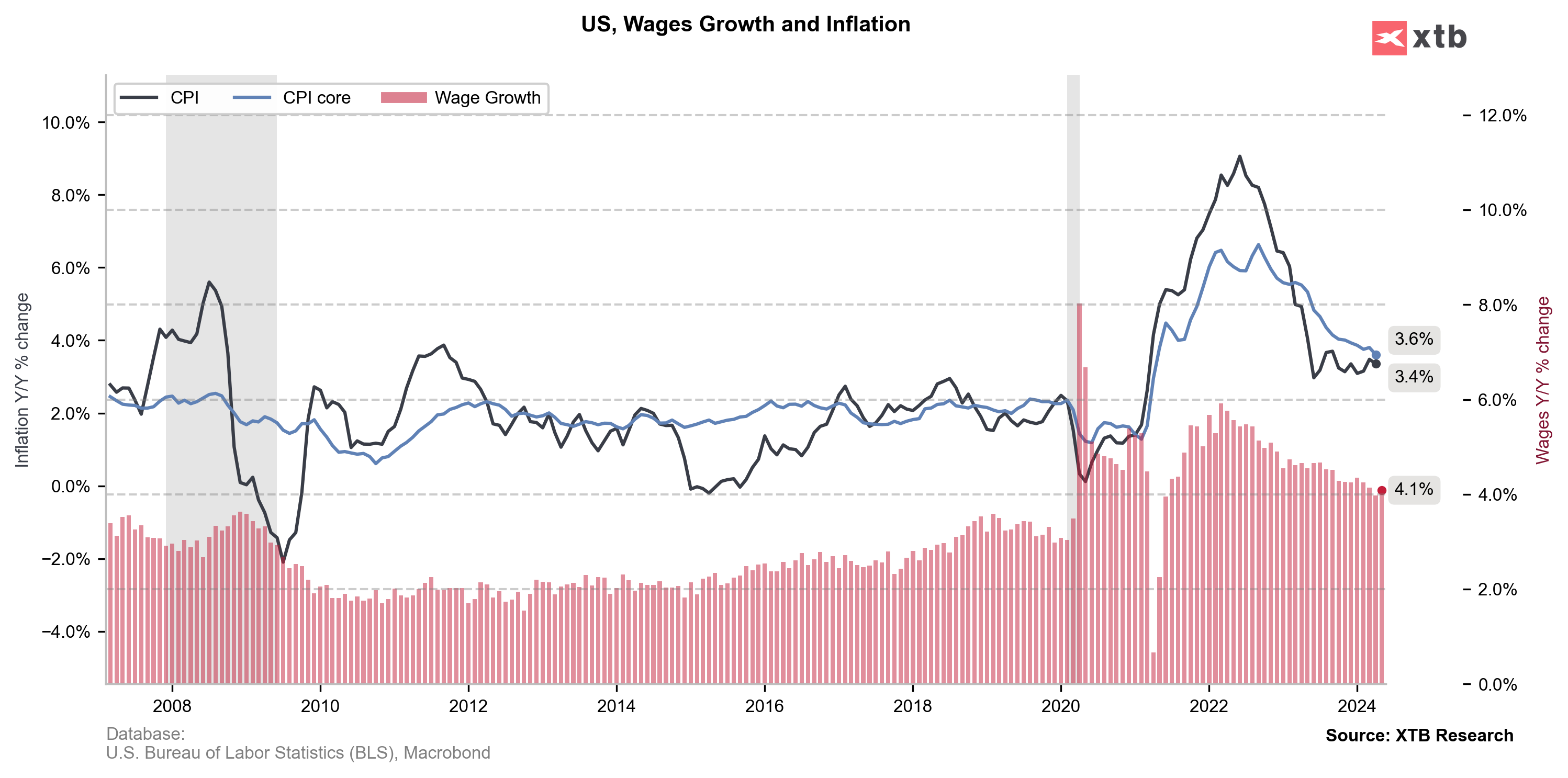

NFP report for May was a key macro release of the day. US jobs market data was released at 1:30 pm BST and was expected to show a slightly higher increase in employment than April's report. Annual wage growth was expected to remain unchanged at 3.9% YoY, but monthly wage growth was seen slowing from 0.5% MoM in April to 0.3% MoM in May.

Actual data turned out to be a hawkish surprise - employment growth turned out to be stronger-than-expected and wage growth unexpectedly accelerated. Such a reading makes it less likely for Fed to sent a dovish message on the next week's meeting. Markets reaction was hawkish as well - USD gained while US index futures dropped.

Money markets now pricing in around-55% chance of Fed cutting rates in September, down from aorund 70% before NFP report release.

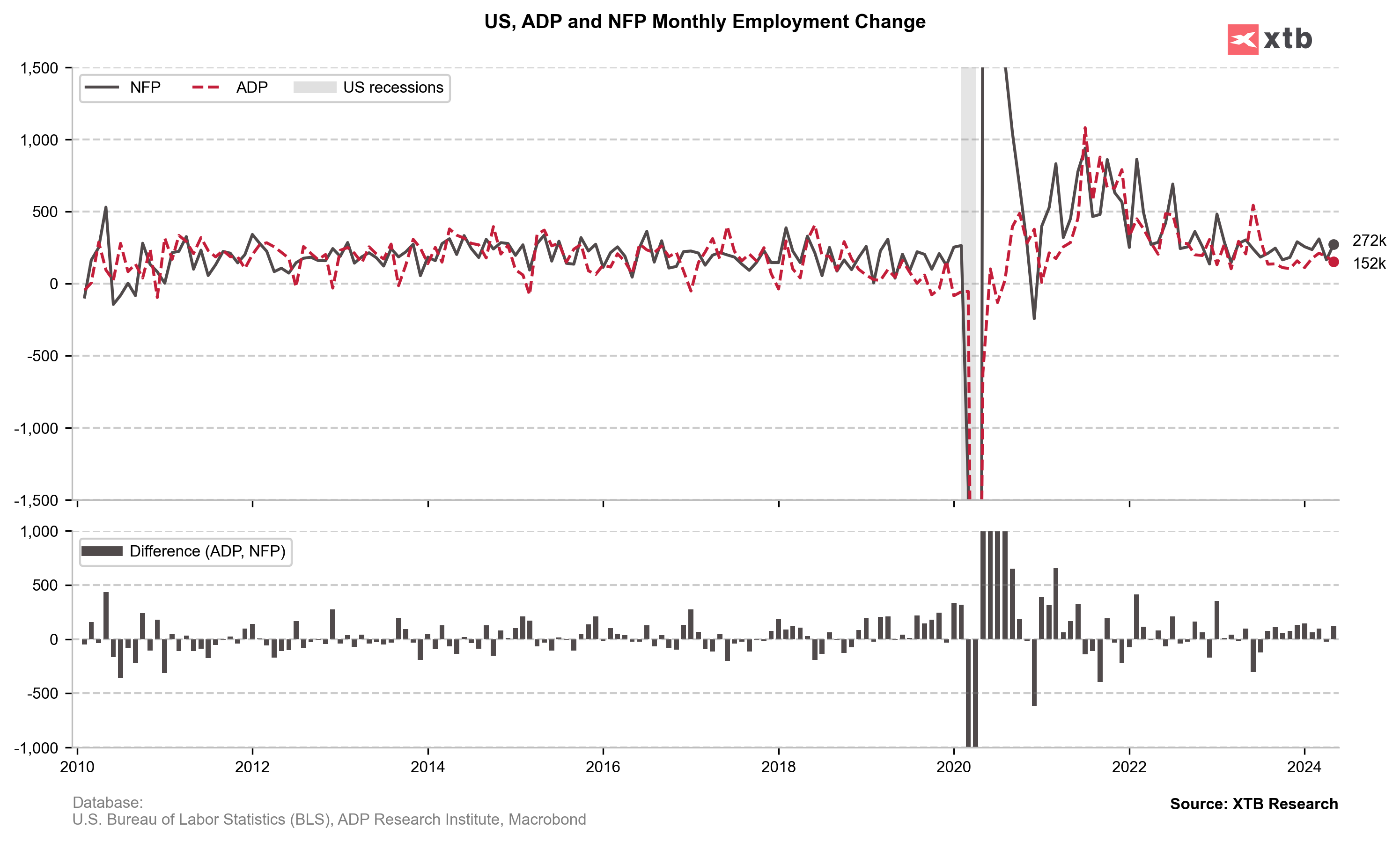

US, NFP report for May

- Non-farm payrolls: 272k vs 185k expected (175k previously)

- Private payrolls: 229k vs 170k expected (167k previously)

- Unemployment rate: 4.0% vs 3.9% expected (3.9% previously)

- Participation rate: 62.5% vs 62.7% expected (62.7% previously)

- Wage growth (annual): 4.1% YoY vs 3.9% YoY expected (3.9% YoY previously)

- Wage growth (monthly): 0.4% MoM vs 0.3% MoM expected (0.5% MoM previously)

Source: xStation5

Source: xStation5

NFP much below expectations! 🚨EURUSD spikes 📈

Dollar and Nasdaq facing a key test

Chart of the Day: What will drive the US stock market? (07.08.2026)

Economic Calendar: Will NFP Move the Market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.