-

CD Projekt’s share price has broken below key support levels and returned to the lows seen in 2025, clearly underperforming the WIG20 index.

-

A key source of concern for some investors is the release of the ‘Songs of the Past’ expansion for The Witcher 3, scheduled for 2027, which seems a long way off, and the lack of a clear release date for The Witcher 4.

-

The market fears that the release schedule will be extended further than the consensus forecast, which could reduce average annual financial results for the period 2026–2028.

-

Potential catalysts for an improvement in sentiment include further strong announcements regarding *Songs of the Past*, more precise guidance for *The Witcher 4*, and possible promotional campaigns for titles already available on the market.

-

CD Projekt’s share price has broken below key support levels and returned to the lows seen in 2025, clearly underperforming the WIG20 index.

-

A key source of concern for some investors is the release of the ‘Songs of the Past’ expansion for The Witcher 3, scheduled for 2027, which seems a long way off, and the lack of a clear release date for The Witcher 4.

-

The market fears that the release schedule will be extended further than the consensus forecast, which could reduce average annual financial results for the period 2026–2028.

-

Potential catalysts for an improvement in sentiment include further strong announcements regarding *Songs of the Past*, more precise guidance for *The Witcher 4*, and possible promotional campaigns for titles already available on the market.

CD Projekt’s share price has once again fallen to around PLN 220, which is close to its lowest levels since May 2025. The company is clearly lagging behind the broader market, despite relatively solid results for the first quarter. Concerns about the release schedule are now coming to the fore – from the expansion Songs of the Past for The Witcher 3 to the release date of The Witcher 4.

It was precisely the announcement of a 2027 release date for the eagerly awaited expansion, coupled with the lack of firm commitments regarding the release date of the next instalment in the series, that triggered the sell-off. Investors have begun to question whether CD Projekt is capable of delivering on its ambitious plan to release several major titles within a few years. At the same time, the market is becoming increasingly sensitive to any delays, as the company’s valuation still implies high expectations regarding future profitability.

CD Projekt underperforms the WIG20 index

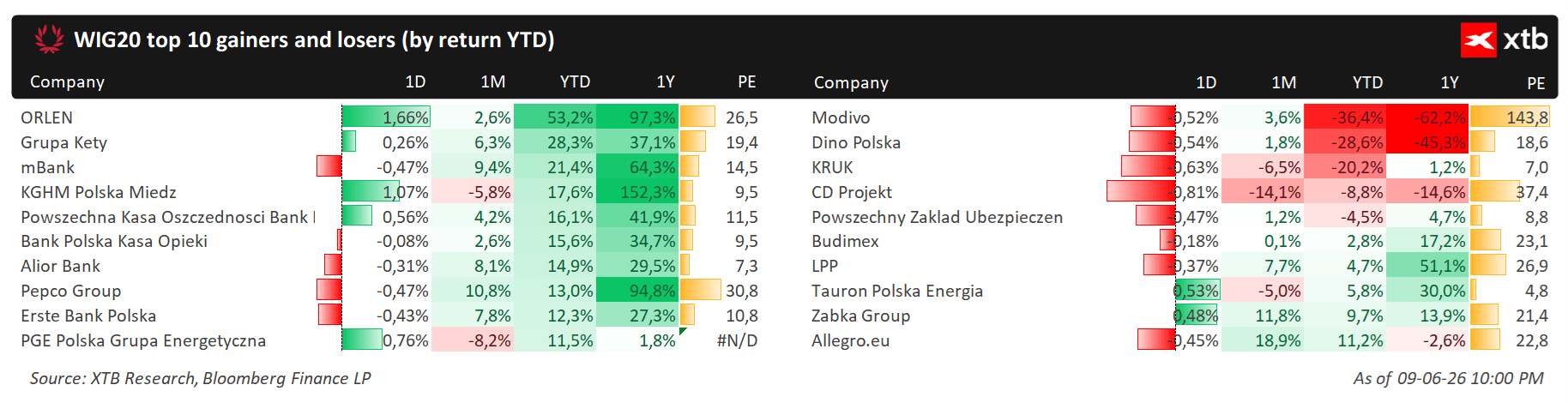

The latest share price of around 220 zł represents a fall of over ten per cent since the start of the year, whilst the broader WIG20 index remains up by almost 13 per cent. For many investors, it is significant that CD Projekt has been among the weakest components of the index despite the solid sales history of The Witcher 3 and Cyberpunk 2077. Only the shares of Modivo, Dino Polska and Kruk have performed worse. Above are the share prices of all companies in the WIG20 index and their performance over various time horizons. Source: xStation

Delayed releases: Songs of the Past and the uncertain The Witcher 4

At the end of May, CD Projekt officially announced the third major expansion for The Witcher 3: Songs of the Past, developed in collaboration with Fool’s Theory. The expansion is not due to be released until 2027 and will be available exclusively on PC and next-gen consoles, with the first details of the plot and gameplay not due to be revealed until late summer 2026.

Although the announcement of a new Geralt adventure was very warmly received by the gaming community, the capital market viewed the long wait for the release as a factor increasing the risk of delays to the entire schedule of major titles. CD Projekt emphasises that The Witcher 4 will not be released before 2027. This decision is, on the one hand, a bad thing, and on the other, a good thing. Let us remember that in 2026, all investors’ eyes will be on GTA VI, so releasing the game at a time when it clashes with Rockstar Games’ release could seriously undermine the sales potential of the new Geralt of Rivia title.

For investors, this means a longer period of intensive production funding, with a limited number of major commercial releases. In the AAA sector, where revenues are heavily concentrated around individual launches, any delay of a year has a significant impact on valuations in DCF models and on the projected cash flow profile.

Publication calendar, valuation and earnings forecasts

In recent years, CD Projekt’s management has repeatedly stated its ambition to deliver more projects than in the previous decade. At the same time, the market is well aware of how costly and time-consuming AAA productions for new consoles and PC are. Following the experience with the launch of Cyberpunk 2077, investors are particularly sensitive to rushing and the risk of technical issues; therefore, the announcement of a longer development cycle for upcoming titles is, on the one hand, understandable, but on the other, it reduces short-term earnings visibility.

The company’s valuation – as measured, for example, by 12-month forward P/E and EV/EBITDA ratios – still implies that future games and expansions will achieve a level of success comparable to The Witcher 3 or the remastered Cyberpunk. However, if the release schedule is significantly extended and revenues are spread over a longer period, the average annual earnings per share may turn out to be lower than assumed in the more optimistic scenarios.

Another cause for concern is the dividend policy – some analysts point out that the postponement of dividend payments and rising CAPEX on new projects mean the company is increasingly focusing on reinvesting cash into portfolio development. For some long-term investors, this is a positive sign, but for those seeking stable cash flows, it may be a reason to reduce their exposure.

What could reverse sentiment towards CD Projekt shares?

Despite the current weakness in the share price, CD Projekt’s track record shows that the turning point is usually marked by concrete gameplay footage and well-received marketing campaigns for major games. A strong presentation of Songs of the Past, with a clear message about the scale of the expansion and its narrative connection to The Witcher 4, could alleviate some of the current concerns. Additionally, the market is awaiting more precise guidance regarding the release window for the next main instalment in the series.

From a long-term perspective, the announcement of a 2027 release need not necessarily be bad news for shareholders. The Witcher 3 has already sold over 65 million copies, making it one of the best-selling titles in the industry’s history. A new expansion following the release of GTA VI will allow the company to monetise the existing brand once again – through extended editions and complete bundles containing all DLC, which some fans will be keen to purchase again on new platforms. Extending the lifecycle of a single, highly profitable IP can therefore stabilise cash flow between the releases of subsequent major games.

Therefore, in the shorter term, the share price will also be influenced by the performance of quarterly results – particularly catalogue sales, the monetisation of Cyberpunk, and the impact of Game Pass-style agreements on revenue and margins.

Finally, it is worth bearing in mind that companies in the gaming sector are characterised by above-average share price volatility and a strong dependence on individual game releases.

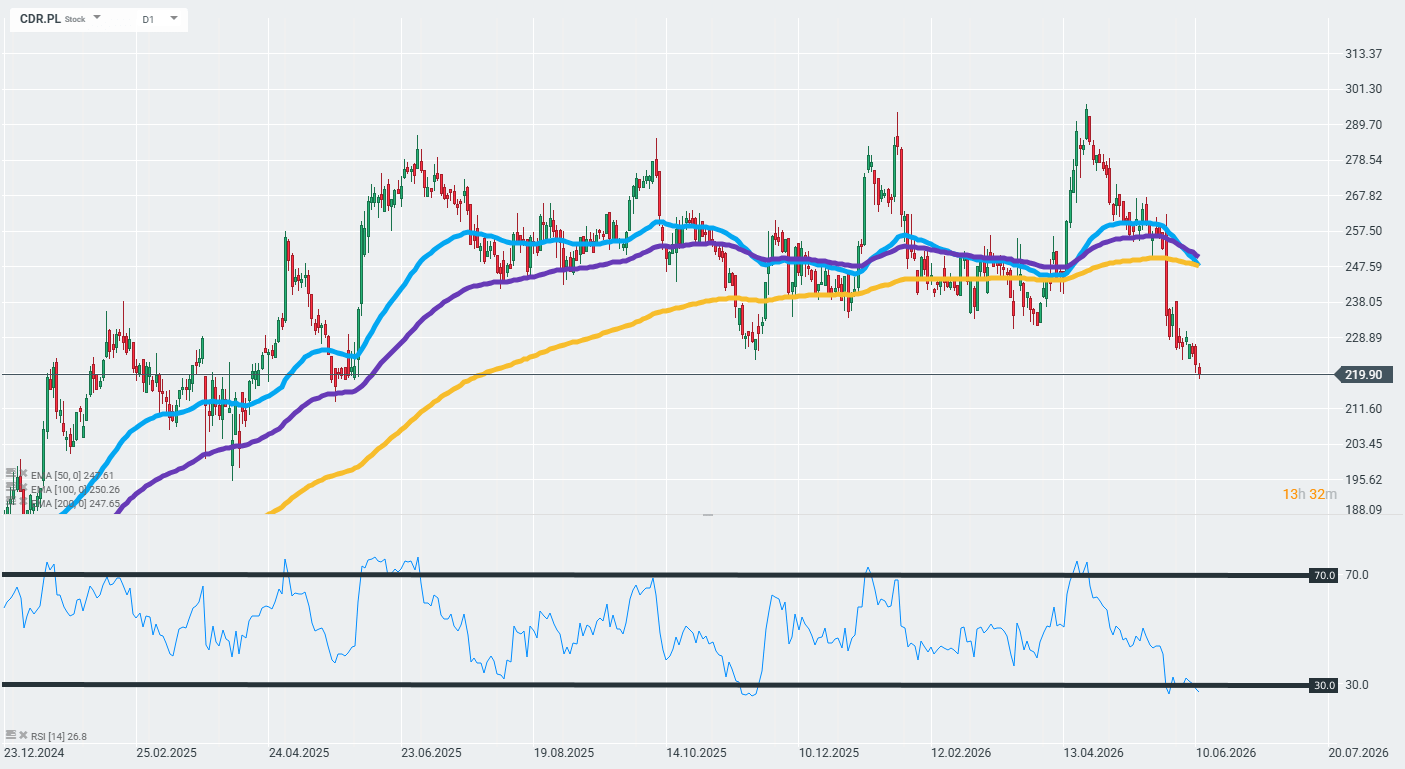

CD Projekt share price chart

The daily chart for CD Projekt shares (CDR.PL) shows that the company’s share price has entered a downtrend, as indicated by the exponential moving averages and the lowest levels seen since May 2025. Interestingly, the RSI for the last 14 days indicates the steepest decline (the lowest RSI value, respectively) since November 2025. Source: xStation

Mateusz Czyżkowski

Financial Markets Analyst XTB Poland

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Berkshire earnings: What do the reports say about the market’s direction?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.