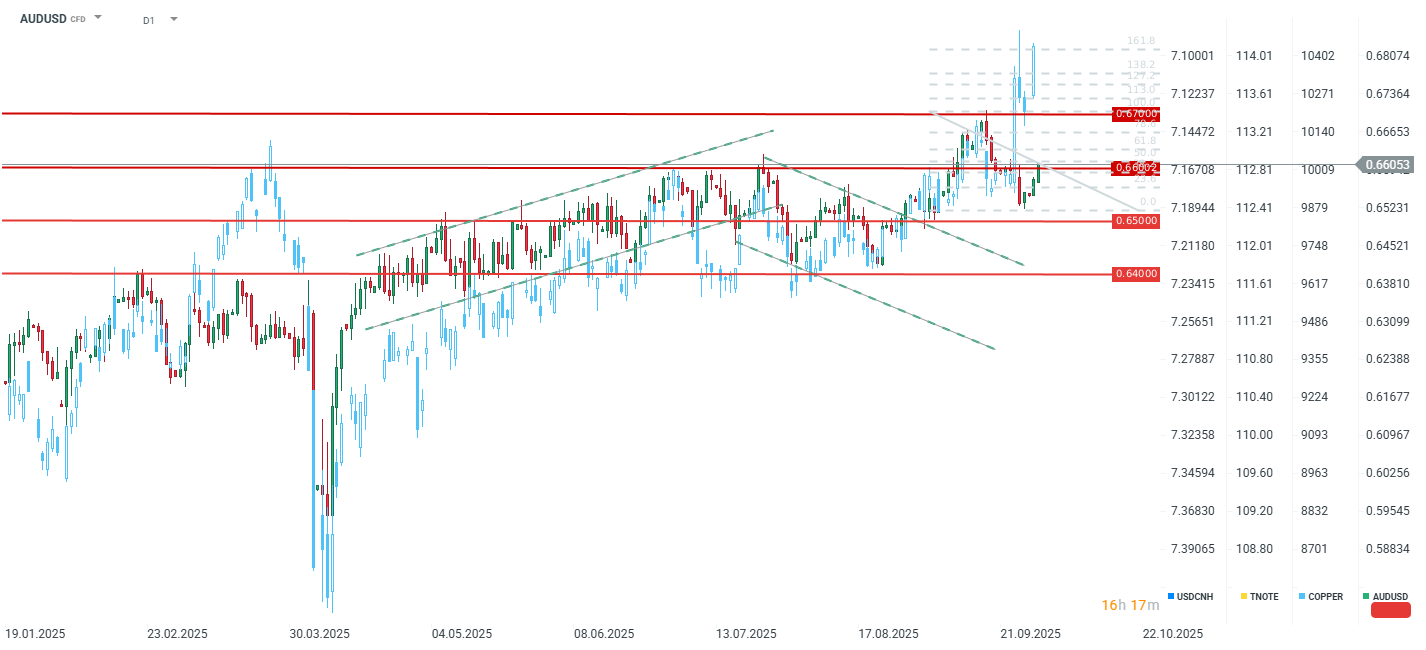

While gold arguably deserves attention for another day, the significant early-morning volatility on AUDUSD warrants its selection as the Chart of the Day, following the Reserve Bank of Australia’s (RBA) interest rate decision.

The RBA kept its cash rate unchanged, a unanimous decision that delivered a distinctly hawkish shift in the assessment of the inflation outlook. The decision was in line with expectations, but the accompanying statement was clearly hawkish. The latest communiqué emphasized that the pace of decline in core inflation has slowed, which the market interpreted as a firm signal against further near-term rate cuts.

Improving macroeconomic data—notably the rebound in consumption and stabilization in the labour market—negates the immediate need for cuts, further supporting the Australian Dollar. The RBA noted that economic activity is gradually picking up and the labour market remains somewhat tight. Global uncertainty persists, particularly concerning US trade policy, though the most extreme scenarios are now deemed less likely, and the influence of tariffs on the economy should be contained.

The RBA maintains a cautious approach, stating its readiness to adjust policy as more data emerges. The bank also stressed that it requires time to assess the full effects of previous rate cuts. The market reaction was swift: AUD/USD rose sharply as investors priced out the risk of further rate cuts, supporting the currency in the short term. The cyclical pause may be prolonged if inflation remains elevated and the economic rebound holds. Moreover, rising commodity prices are positive for Australia, driving increased export revenues. Stronger expansion in China also points to faster Australian growth in the near term.

The AUDUSD pair has broken above the 0.6600 level and is testing the 50.0% Fibonacci retracement of the last downtrend within the broader uptrend. As evidenced by copper prices continuing their rally, this commodity strength acts as a further tailwind for the Australian Dollar.

It is also worth noting that the Australian Dollar, when measured against the New Zealand Dollar, sees the AUDNZD pair hitting 1.14, its highest level since 2022. While this is a rare sight over the past 12 years, the pair traded significantly higher at the end of the previous decade, suggesting potential for substantial further gains in the event of a global recovery. Furthermore, a notable divergence is currently observed in the monetary policy stances of Australia and New Zealand.

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

🔼 Gold gains 1.7%

🛢️Brent Crude Oil Tests $95 per Barrel

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.