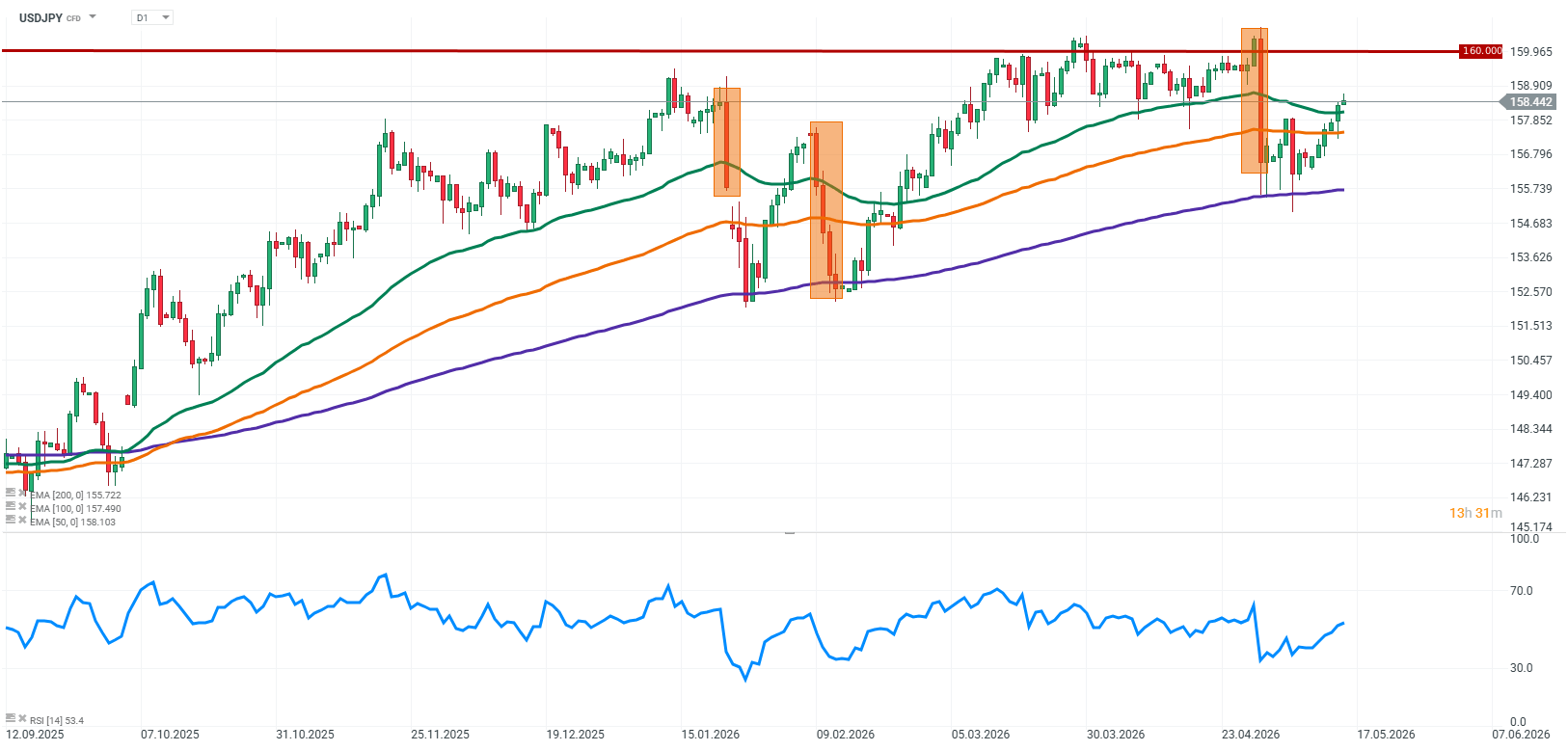

USDJPY today resembles a fight between two boxers, where one is desperately trying not to be pushed into the corner but is running out of strength and ideas, while successive blows coming from macroeconomics and geopolitics only make his situation worse. In this exchange, it becomes increasingly clear that this is no longer a fight for dominance, but a struggle for survival under the rhythm imposed by a stronger opponent, who is gradually taking control of the pace and space in the market.

Source: xStation5

Geopolitics and Energy

The key backdrop to current moves remains tensions around the Strait of Hormuz. Escalating geopolitical risk is pushing up oil prices and, more broadly, all energy commodities, directly hitting importing economies. Japan is in a particularly difficult position as it remains heavily dependent on imported energy resources. Rising energy costs are immediately feeding through into inflationary pressure across the entire production chain, increasing economic stress.

Inflation and the Surprise in Data

The latest producer inflation figures showed a clear acceleration. The PPI rose to 4.9% y/y versus 2.6% previously, significantly beating market expectations. This is not just a statistical deviation, but a signal that cost pressures in Japan are building faster than anticipated. Importantly, inflation is largely imported, meaning its source lies outside domestic policy and is strongly tied to global conditions.

Bank of Japan Under Pressure

Rising inflation is starting to materially reshape the narrative around the Bank of Japan. The market is increasingly pricing in the possibility of a rate hike as early as June, while some economists suggest this may not be a one-off move but the beginning of a broader normalization cycle. This marks a significant shift compared to years of ultra-loose monetary policy that defined Japan’s markets for decades. Inflationary pressure is putting the BOJ in a position where inaction could increasingly be seen as a policy mistake.

Interest Rate Differential and Dollar Strength

Despite rising expectations for policy tightening in Japan, the yen remains structurally weak. The key driver is the massive interest rate differential between Japan and the United States. The Federal Reserve System continues to maintain a relatively high interest rate environment, supporting the dollar and keeping carry trade strategies attractive. In practice, this means capital still has a strong incentive to stay positioned against the yen, limiting its ability to stage a sustained recovery despite shifting BOJ expectations.

Intervention Risk and Market Reaction

Another factor in play is speculation around potential currency intervention by Japanese authorities. Such actions can trigger sharp but typically short-lived yen strength. However, the market remains skeptical about their long-term effectiveness without a corresponding shift in monetary policy. As a result, interventions tend to act more as temporary disruptions in the trend rather than true reversals.

Market Picture

As a result, USDJPY is currently positioned at the intersection of three forces. On one side, the interest rate differential continues to support the dollar. On another, rising expectations of a more hawkish Bank of Japan are supporting the yen. Completing the picture is geopolitics, which through energy prices is fueling inflation and forcing continuous repricing of scenarios.

In the short term, the most likely environment remains elevated volatility, with the market reacting primarily to inflation data and Bank of Japan communications while searching for balance between these three competing forces.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.