Crude oil remains the key asset this week, and every headline from the Middle East immediately triggers sharp price swings. WTI is approaching $116/bbl, its highest level in a month, while the June Brent contract has broken through $111. Saudi Aramco has set the official selling price for Arab Light to Asia at a record premium of $19.50 above the Oman/Dubai benchmark, compared to just $2.50 a month earlier. Today at 12:00 GMT (Wednesday, 3:00 a.m. Polish time), another of Trump’s “final deadlines” for Iran regarding the Strait of Hormuz expires. He is threatening to destroy the country’s energy and transportation infrastructure, though at the same time he declares that talks are “going well.” The Wall Street Journal reports that Washington is actively planning precision strikes on Iranian energy infrastructure, and Israel has approved updated target lists as a contingency plan, keeping the market on high alert. Adding to the gloomy sentiment is a missile attack on the Saudi petrochemical center in Jubail, facilities responsible for about 7% of Saudi GDP, although Riyadh’s missile defense system managed to intercept all seven ballistic missiles.

The fundamental picture, however, remains more complex than prices alone would suggest. More ships have passed through the Strait of Hormuz in recent days than at any time since the conflict began, under bilateral agreements between Iran and India, Pakistan, China, the Philippines, and Malaysia, although issues regarding vessel insurance and the details of these agreements remain unclear. Oil is reacting to these reports with much less volatility than a few days ago, as the market has entered a zone of strong supply and is gradually pricing in the possibility of a partial reopening of the route. OPEC+ agreed at its weekend meeting to increase production by 206,000 barrels per day in May, but only after the Strait reopens, which limits the upside potential for prices in a de-escalation scenario. Russia, which is grappling with Ukrainian attacks on its own oil infrastructure, remains a key factor on the supply side, as does the fact that Iraq, Kuwait, Saudi Arabia, and the UAE have already significantly curtailed their production volumes. All eyes are on Washington and Tehran tonight—the market remains hostage to a single tweet summarizing the issue of the media “deadline.”

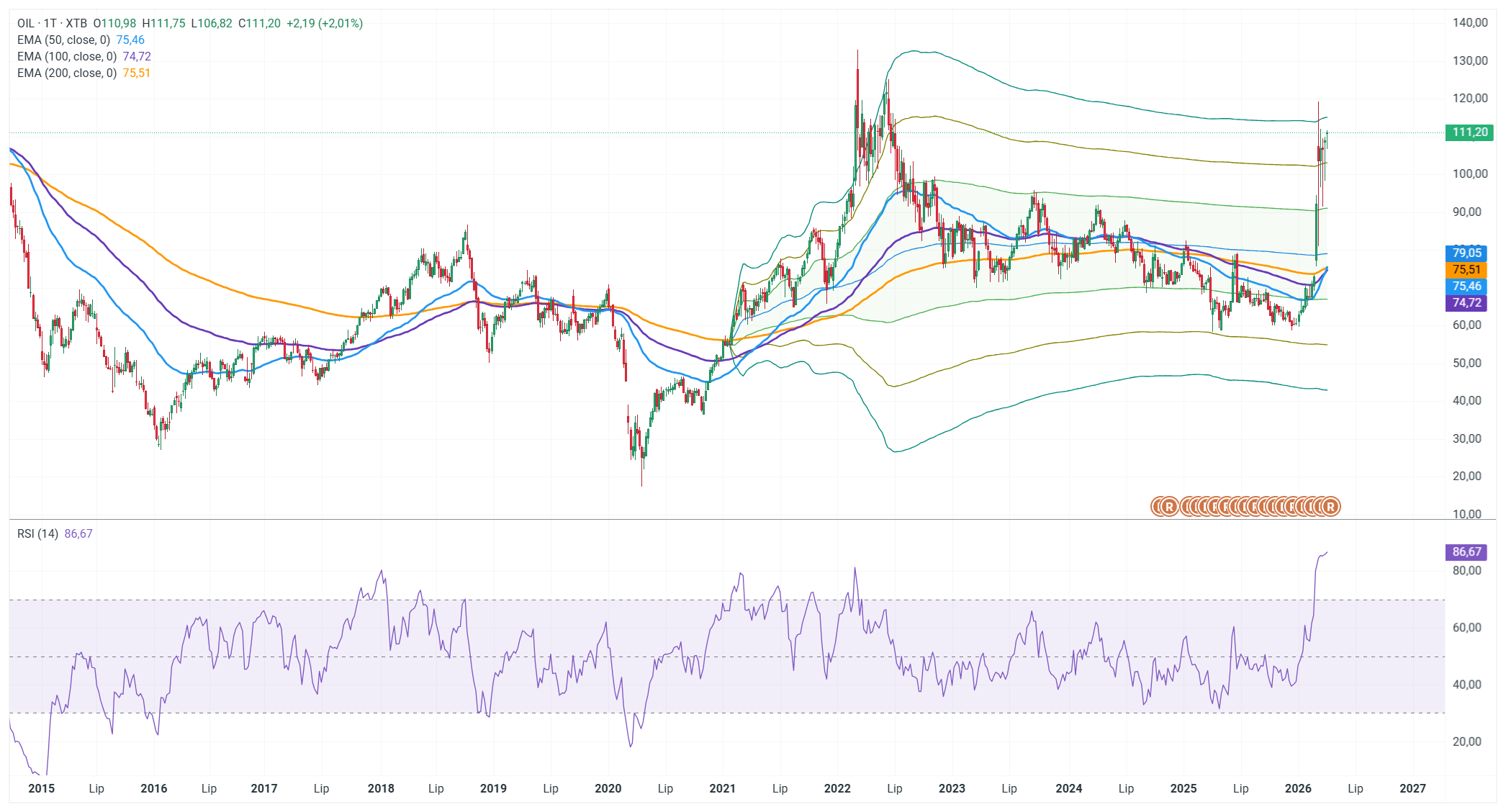

All three key moving averages—the 50-day EMA, 100-day EMA, and 200-day EMA—are still clustered around the $74–79 range, which means the current price is trading at a premium of over 45% above the long-term averages, which is an extreme deviation from the historical norm. The RSI(14) stands at as high as 86.67 — an overbought level, clearly exceeding the RSI peaks from 2022. At this point, however, the turmoil surrounding the uncertain outcome of the U.S.-Iran talks does not allow for a reduction in demand pressure on the commodity. Source: xStation

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

Gold gains almost 3% trying to reverse the trend

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.