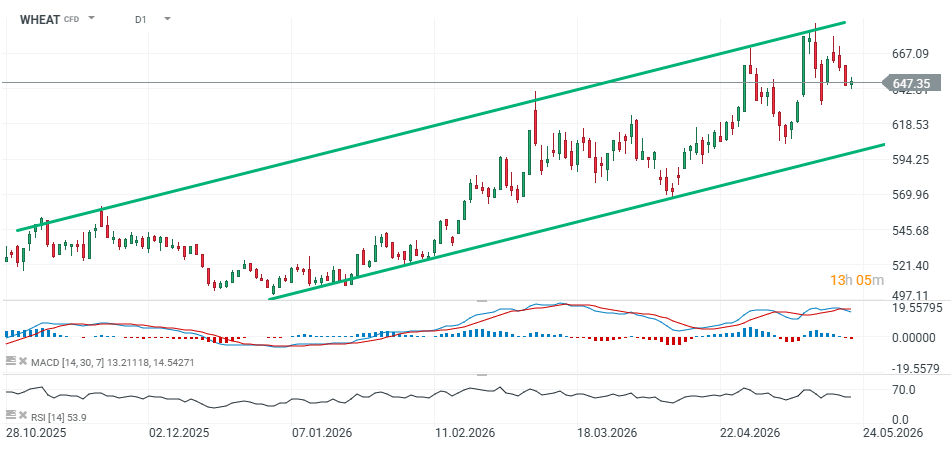

The wheat market recently entered a phase of very dynamic gains after the US Department of Agriculture (USDA) released exceptionally weak forecasts for the 2026/27 winter wheat crop. The scale of the downward revisions surprised even the most bearish market participants and triggered a strong rally in futures markets. Despite this, CBOT wheat futures have recently fallen back below the 650 level.

- On the other hand, according to ADM Investor Services, the arrival of rainfall in key US growing regions has largely neutralized earlier concerns over tightening grain supplies. Potential buying interest from China is currently being more than offset by improving weather conditions across the United States.

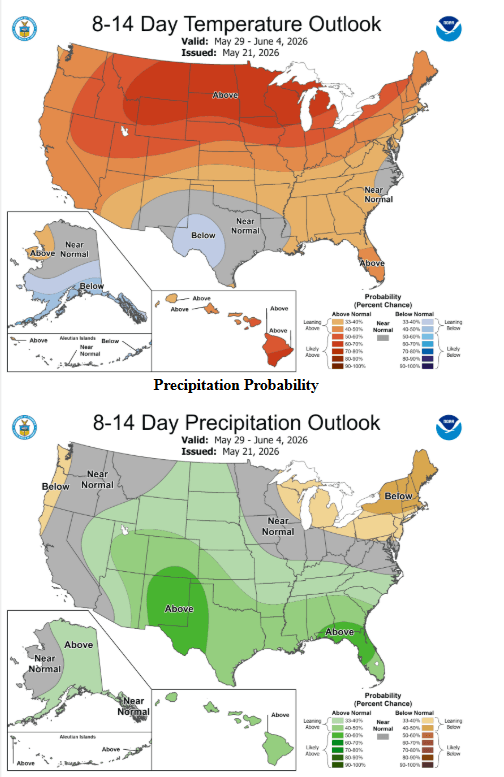

- The US Climate Prediction Center (NOAA) forecasts above-average rainfall across the Great Plains over the next 8 to 14 days, improving crop prospects. Meanwhile, AgResource notes that large speculative traders are reducing long exposure ahead of the weekend and amid ongoing political uncertainty.

Crop problems and speculative activity?

The biggest issue remains the catastrophic weather situation across the southern US Plains. Months of drought have severely affected regions responsible for hard red winter wheat production, particularly western Kansas, eastern Colorado, and the Panhandle area. USDA projects total US winter wheat production at just 1.048 billion bushels, down 25% from the previous season and the lowest level since 1965. Importantly, the initial USDA estimate came in around 160 million bushels below the average analyst forecast.

- Hard red winter wheat has been hit the hardest. Production for this segment is estimated at 514.8 million bushels, down as much as 36% year-over-year. In Kansas — the key state for US wheat production — USDA expects average yields of only 37 bushels per acre, compared to 51 bushels a year earlier.

- The market had been reacting to deteriorating crop conditions since the beginning of the year, but the May USDA report triggered the latest leg higher. If supply prospects continue to worsen, the market may attempt to extend the bullish move further.

- Fundamentally, the market has also received support from the global supply-demand balance. USDA expects smaller harvests not only in the US, but also among major exporters such as Argentina, Australia, and Canada. As a result, global wheat stocks are projected to decline by around 1.5%, while US ending stocks are expected to fall 17% to 775 million bushels — the lowest level in three years.

- Paradoxically, however, higher prices are beginning to reduce the competitiveness of US wheat on export markets. The spring rally pushed US winter wheat prices well above Russian offers. USDA forecasts that US wheat exports in the 2026/27 season will decline 15% from the five-year highs recorded a season earlier, falling to 762 million bushels.

- At the same time, USDA estimates that the average price received by US farmers will rise to USD 6.50 per bushel, USD 1.50 higher than in the 2025/26 season. For producers, this creates attractive selling opportunities.

Current price movements are largely being driven by speculative fund activity. Many funds previously held significant short positions in wheat, and aggressive short covering can trigger extremely volatile price action. Nevertheless, history shows that rallies in wheat often fade relatively quickly, as funds are usually reluctant to maintain long positions for extended periods.

WHEAT (D1 interval)

Source: xStation5

Source: NOAA

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.