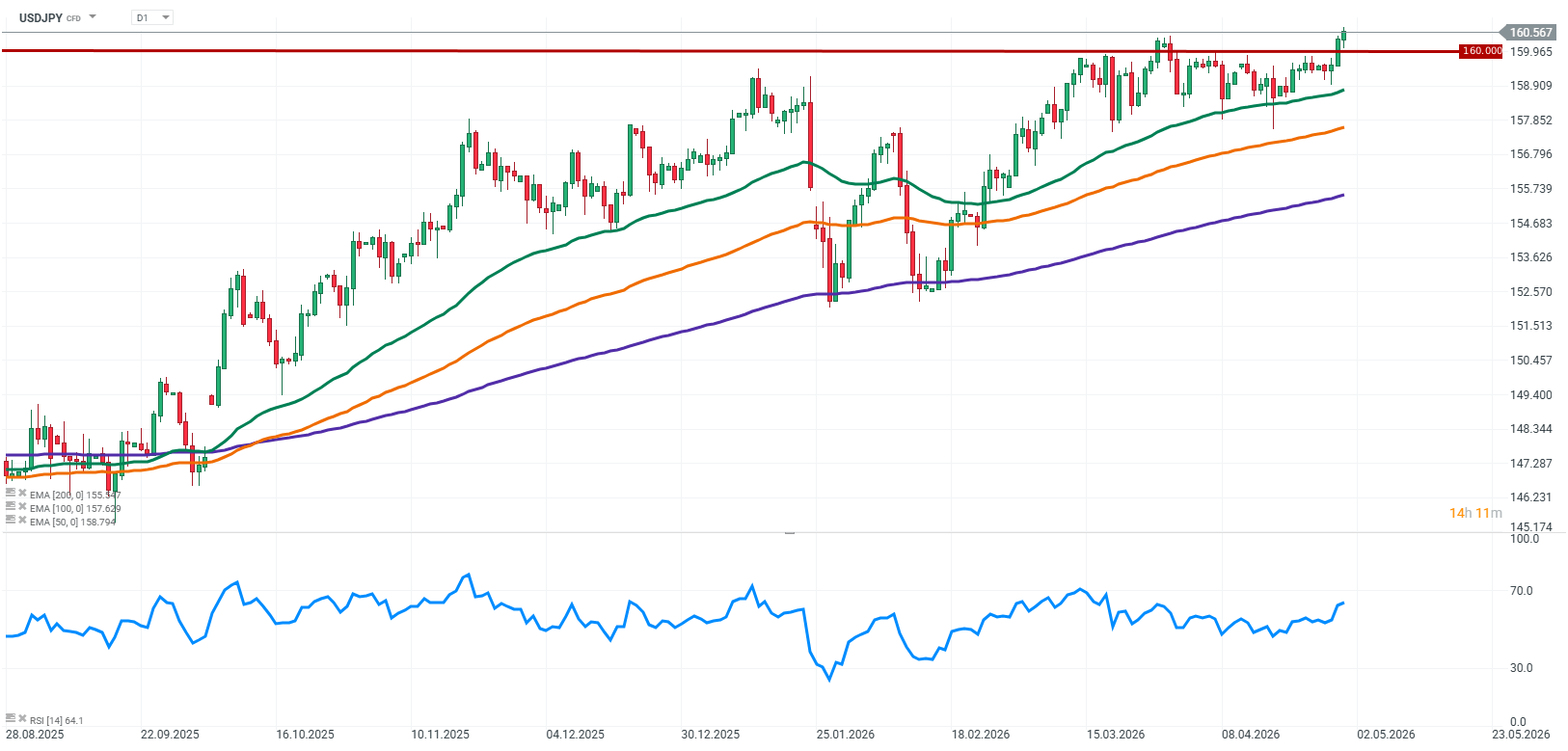

USDJPY has decisively broken through the psychological 160 level, reaching new multi-month highs and entering territory that was until recently treated as an informal red line for Japanese authorities. Importantly, the breakout has not been met with any strong verbal pushback from the Ministry of Finance, which the market interprets as a growing tolerance for further yen weakness, at least in the short term.

This move is not happening in isolation. It reflects the classic combination of two dominant macro forces: a persistently wide interest rate differential and mounting pressures within Japan’s real economy, which are becoming increasingly difficult to ignore.

Source xStation5

What is driving USDJPY?

Fed and BOJ stable rates, diverging narratives

Both the Federal Reserve and the Bank of Japan left interest rates unchanged, which in itself was not a surprise for markets. The key focus, however, was on communication nuances that further widened the divergence between the two economies.

The Fed remains relatively hawkish, emphasizing the resilience of the US economy and a lack of urgency to pivot toward rate cuts. As a result, the dollar continues to benefit from higher yields and the sustained attractiveness of carry trade strategies.

On the other side, the BOJ remains cautious, trying to balance the end of ultra-loose monetary policy with the risks of tightening too quickly. However, it is becoming increasingly clear that the issue is no longer only imported inflation driven by commodities, but also yen weakness itself, which is now amplifying domestic price pressures.

Japan trapped in a cost and commodities squeeze

Japan’s economic fundamentals are sending increasingly mixed signals. Retail sales suggest some resilience in consumer demand, while industrial production disappointed in March, partly due to supply chain disruptions and rising cost pressures linked to global commodity tensions.

Particularly important is the situation around the Strait of Hormuz, which continues to elevate risks for global oil and gas flows. For Japan, a heavily import-dependent energy economy, this translates into higher production costs and a deteriorating trade balance.

In this context, reports of a possible return of energy subsidies during the summer highlight the government’s attempt to cushion cost pressures, although such measures appear more like short-term stabilization tools rather than a structural response to persistent yen weakness.

160 as a psychological level and a test of market patience

The break above 160 is not purely a technical move. It represents a direct test of Japan’s tolerance threshold for currency weakness. Historically, these levels have been associated with heightened sensitivity from authorities, yet the lack of immediate reaction is encouraging the market to probe further.

At this stage, the balance of forces remains tilted toward fundamentals. A persistently wide US–Japan rate differential continues to support capital flows into the dollar, while weak Japanese industrial data and commodity-driven pressures leave the BOJ with little room to tighten policy aggressively in the near term.

Outlook

The current USDJPY move increasingly resembles a classic carry trade driven environment, where fundamentals and momentum reinforce each other. Unless there is a meaningful shift in BOJ policy or a more forceful intervention from the Ministry of Finance, the path of least resistance remains higher.

The key question is no longer whether 160 would be broken, but how long the market will continue testing the absence of intervention and where the true line in the sand ultimately lies.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.