One of the most striking developments in recent months is how completely sentiment and expectations have diverged - clearly visible in the difference between commodity-market analysts and equity-market analysts.

Commodity analysts are sounding the alarm and warning of a catastrophe stemming from the loss of around 20% of global oil and fuel supply. At the same time, equity analysts are explaining successive upward revisions to EPS forecasts. Who is right?

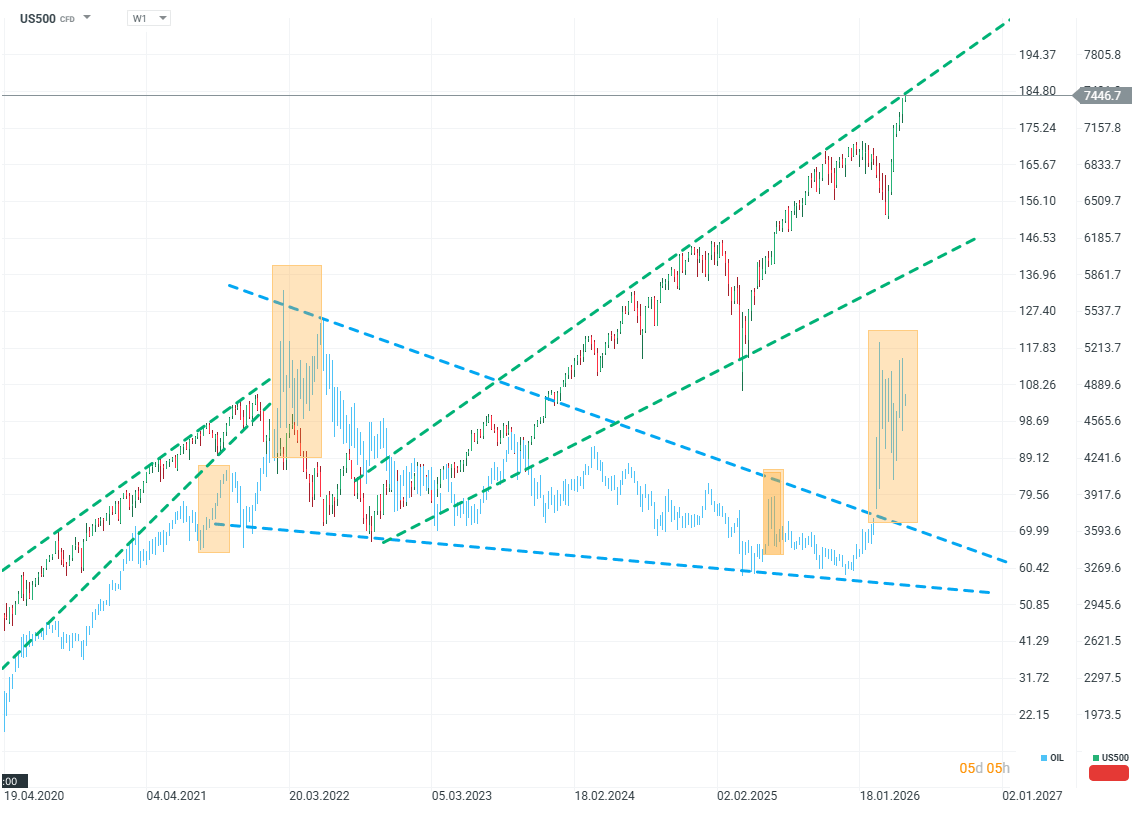

US500 vs OIL (W1)

Source: xStation5

For now, a mysterious stalemate can still be observed - indices and stock prices are setting new records even though oil prices are far above the levels expected just a few months ago.

Saudi Aramco is the world’s largest energy company, controlling an industry built around crude oil in Saudi Arabia. The company’s CEO has commented on the market situation.

The CEO uses strong language. According to Amin Nasser, the market is in a period of deep imbalance between supply and demand. He estimates that even if the Strait of Hormuz were reopened tomorrow, the market would need about a year to normalize. The company’s president speaks of a loss of one billion barrels of oil supply and points out that the scale of the crisis is unprecedented.

It is also hard to say that the current situation is not beneficial for the company. Saudi Arabia built the powerful “East–West” pipeline across the Arabian Desert precisely for a scenario like the one unfolding now. At the same time, the company’s results show that the surge in oil prices drove net profit up by nearly 25% in Q1 2025.

What could be the reason why oil prices seem to be reacting rather cautiously to a crisis of this magnitude?

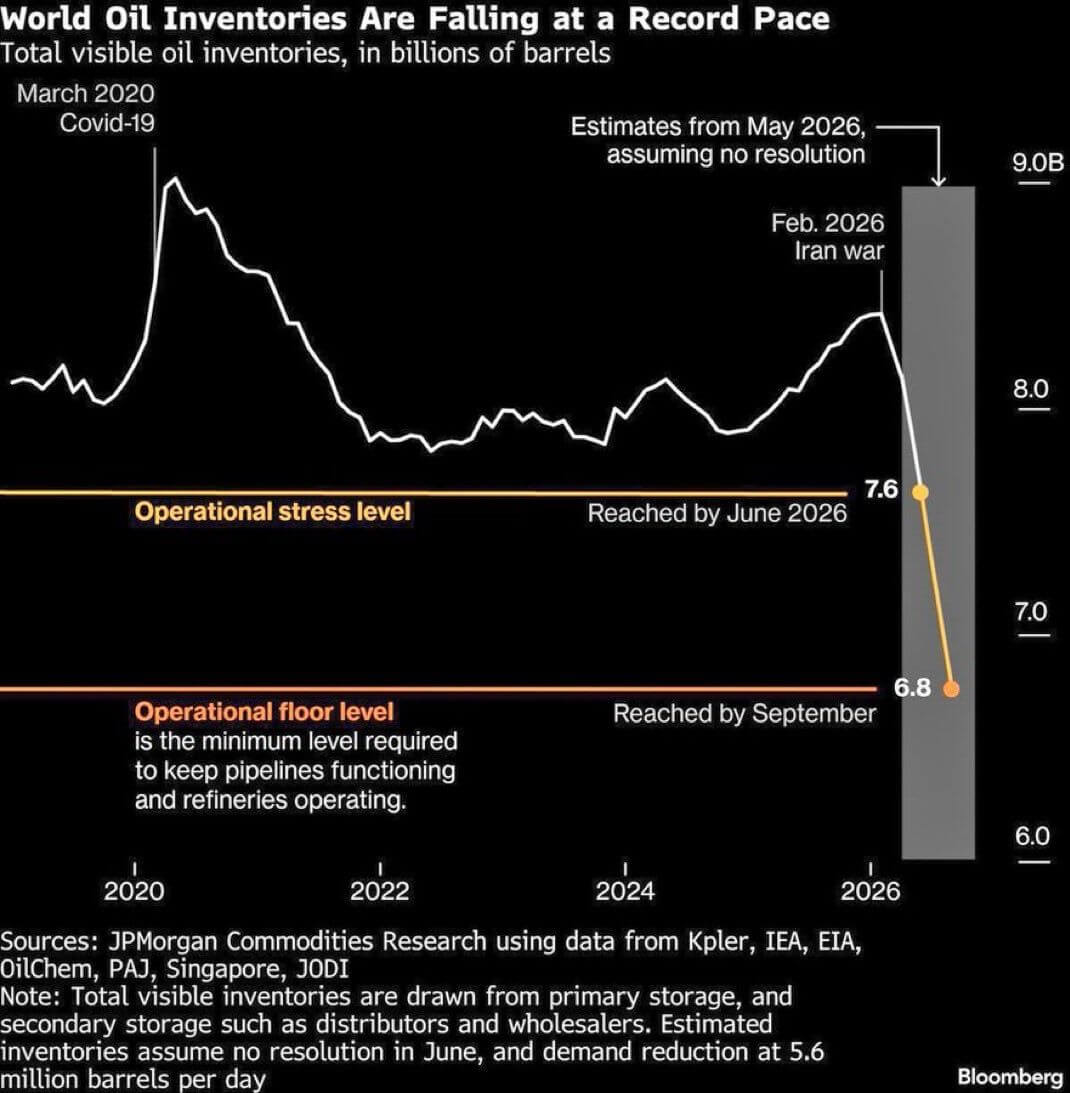

Source: Bloomberg Finance Lp

One factor highlighted by both Morgan Stanley and Bloomberg analyses is inventories - oil stockpiles are among the most important elements.

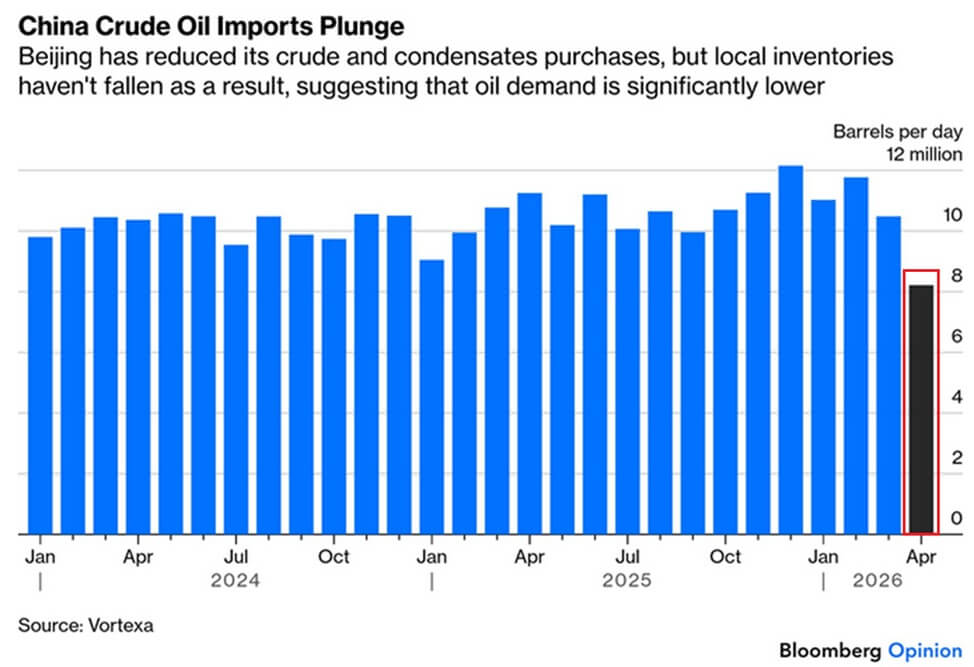

The most important player in this context is China. China imported about 25–35% of its oil from the Persian Gulf. At the same time, the latest data show that China’s oil imports fell from 12 million barrels to just over 8 million—a drop of more than 3 million barrels, or over 30%. This is no coincidence: China used falling oil prices in 2025 to build a huge stockpile of crude. Were these stockpiles built precisely for such a contingency?

Source: Bloomberg Finance Lp

It’s impossible to say - and in practice it doesn’t matter. What it effectively means is that, due solely to China’s actions, we may see a significant delay in how reduced supply feeds through into prices. China is absorbing shortages and inflationary pressure—and has a strong incentive to do so. Chinese industry remains in a slowdown phase, while maintaining trade with the West is an imperative for China.

Higher domestic inflation could, under current circumstances, help reduce the real burden of rising debt and stimulate consumption and investment. Meanwhile, the West avoids a recession - sone that would be just as painful for China as it would be for the West itself. What's crucial to understand is that this market freeze will persist as long as China continues to de facto subsidize global disinflation. This may be one of the key yet rarely mentioned issues in the context of the upcoming Trump-XI meeting.

Kamil Szczepański

XTB Financial Markets Analyst

BREAKING: BoE Keeps Rates Unchanged

🛢️Further escalation and tense situation do not drive oil further

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

Not so hawkish words, dovish dodges. EURUSD at 1.1450 during Kevin Warsh's Q&A

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.