European equities edge lower on Friday, as investor caution builds ahead of the final weekend before EU-US trade negotiations conclude. The EU50 dips 0.2%, with Germany’s DAX leading losses, down 0.6%. Spain’s IBEX 35 drops 0.55%, while the FTSE 100 and FTSE MIB shed 0.3% and trade flat, respectively. In contrast, France’s CAC 40 ekes out a modest 0.1% gain, bucking the broader trend.

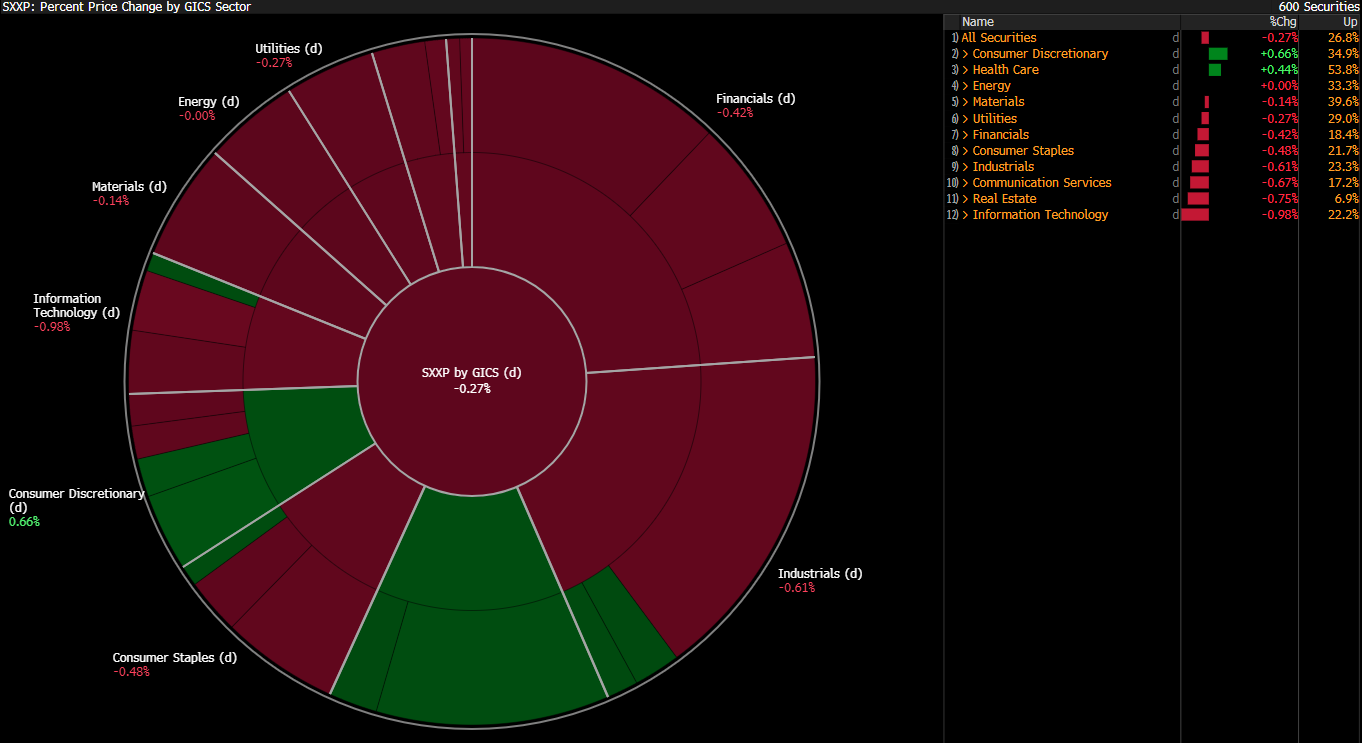

Among Eurostoxx 600 sectors, tech is performing the worst with companies like Nokia (-2.2%), ASML (-2%), Capgemini (-1%) and megacap SAP (-0.8%) weighing on the index. Consumer discretionary stocks show some resilience despite a broad disappointment in the apparel sector due to Puma’s earnings report. Healthcare sector also posted gains.

Volatility in Eurostoxx 600 sectors. Source: Bloomberg Finance LP

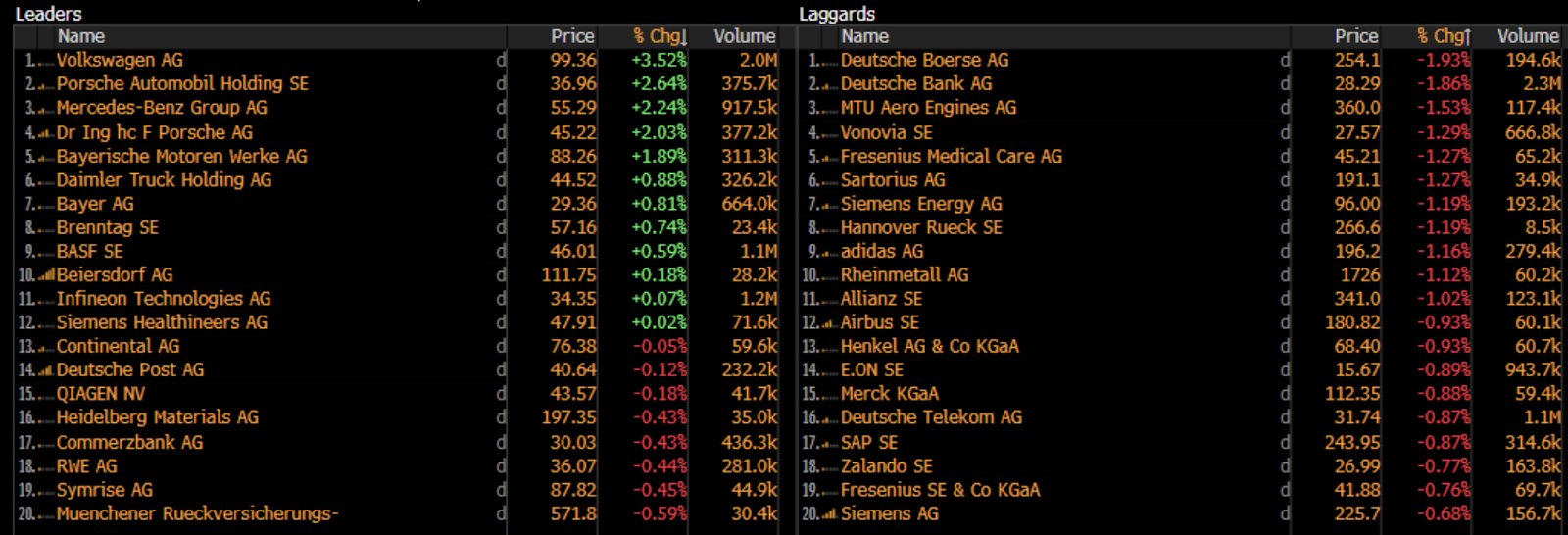

Performance of DAX-listed companies. Source: Bloomberg Finance LP

DE40 (H1)

DAX futures are currently consolidating around the 24,220 level, midway between the 61.8% and 78.6% Fibonacci retracement levels. The market appears to be completing a head and shoulders pattern, with sellers maintaining control below the 10-hour exponential moving average (EMA10, yellow). A decisive breakout above the closely aligned EMA30 and EMA100 (purple) could trigger a renewed rally toward recent highs near 24,640. However, further upside will largely depend on positive developments in EU-US trade talks. On the downside, any disappointment stemming from tariff news or earnings reports could deepen the correction, pushing prices below the 24,000 support level.

Source: xStation5

Company news:

-

Alten (ATE.FR), French tech and industrial consulting firm, reported a 1.1% H1 revenue decline, with activity falling 5.6% on an organic basis. Automotive slumped 15%, offset only partly by growth in Defense, Energy, and Rail. The group expects full-year organic contraction of 5.2–5.5% and operating margin of ~8%, citing weak demand and calendar effects. The stock is down 5.2%

-

Carrefour (CA.FR) agreed to sell its loss-making Italian business to NewPrinces Group for around €1 billion, aiming to boost growth and cash flow. The retailer posted a 4.4% like-for-like sales rise in Q2, led by France’s recovery, but profitability remains pressured with a 1.6% operating margin in H1. Shares surged nearly 7%.

-

Close Brothers (CBG.UK), a UK-based merchant banking group, will sell Winterflood Securities, its market-making unit, to Marex for £103.9 million in a strategic move to streamline operations. The deal reflects continued consolidation in the financial services sector and marks Marex’s latest acquisition as it expands its capital markets footprint. Completion is subject to regulatory approval. The stock rallied 9.2%

-

LVMH (MC.FR) posted a 9% drop in fashion and leather goods sales in Q2, missing estimates as demand waned, especially in China and Japan. Despite a €9bn H1 profit beating forecasts, shares slipped. Louis Vuitton plans a new Texas plant to offset tariffs. Dior enters creative transition under Jonathan Anderson.

-

Nokia’s (NOKIA.FI) earnings missed estimates by $0.02 per share, reporting $0.11 versus the expected $0.13. Revenue came in at $5.4 billion, below analysts’ consensus of $5.6 billion. The results reflect continued headwinds from competitive pressures and market uncertainties. Investors will closely monitor Nokia’s strategies to drive future growth.

-

Puma (PUM.DE) is currently the worst performer in Eurostoxx 600, with shares plunging 16.7% after posting a €247M Q2 net loss and slashing its 2025 outlook. Sales fell across all regions, with Apparel and Accessories missing forecasts. The firm now expects a full-year EBIT loss, citing tariffs, margin pressure, and elevated inventories. Capex was cut by €50M.

-

Valeo (FR.FR), French car part supplier, cut its 2025 sales outlook to €20.5B, citing a €750M currency hit and weaker customer markets. Q2 sales fell 6% to €5.35B. While most U.S.-bound products are tariff-exempt, analysts warn that softer demand may pressure margins despite cost pass-through to automakers. Tariffs remain a key industry risk.

-

Volkswagen (VOW1.DE) took a €1.3bn hit to H1 operating profit from U.S. import tariffs, forcing a cut in its 2025 profit margin forecast to 4–5%. The group warned that tariffs as high as 27.5% could become permanent. Despite progress on restructuring, including plans to cut 35,000 jobs by 2030, U.S. trade pressure has sharply dented export volumes and revenues. The stock shows resilience, gaining 3.3%.

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Hormuz Deal Moves Closer

US Open: AMD and SpaceX failed to impress, but the broader market remains resilient

Breaking: US services remain strong, inflation pressures rise

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.