The defence industry is gradually wrapping up its earnings season. Thursday will be dominated mainly by Europe’s sector leaders. Against the backdrop of a persistent threat environment and the escalation of armed conflicts worldwide, expectations for companies’ results in this sector are becoming ever higher, and increasingly difficult to meet.

Safran

One of the largest companies in its class. The French aerospace group, in addition to military supplies, also has a large and fast-growing civil segment.

The market reaction suggests the company delivered exactly what investors expected, and that meaningful growth, along with its characteristics, was already priced in.

Revenue rose 18.8% year on year to EUR 8.48bn, slightly beating the market consensus of around EUR 8.3bn.

Segment details were mixed.

- Revenue in “Equipment & Defense” delivered organic growth of 13.5%, reaching EUR 3.36bn, with “OE” sales up 15.3%.

- Revenue in propulsion systems grew organically by 33% to EUR 4.5bn, with sales up 35%.

- The “Aircraft Interiors” segment grew organically by 9.2% (though it is worth noting that in nominal terms it declined) to EUR 700m.

Management confirmed its commitments regarding FY2026 guidance, calling for revenue in the “low teens” (in EUR billions), recurring operating income above EUR 6.1bn, and FCF of at least EUR 4.4bn.

The company also noted it is monitoring the situation in the Middle East and highlighted initial initiatives in the region, such as cooperation with Qatar on building an air-defence system.

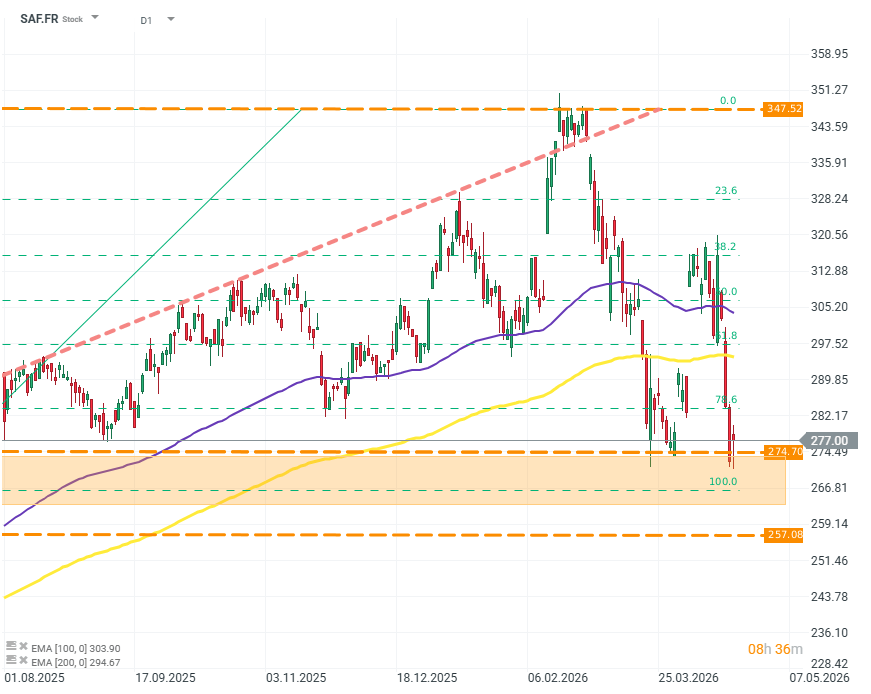

SAF.FR (D1)

The stock shows high price-change dynamics with high frequency. This may point to equally dynamic shifts in investors’ expectations regarding the company’s outlook, although given the market and geopolitical environment, uncertainty should arguably skew more pro-growth. Source: xStation 5

Saab AB

The Swedish group delivered a very strong quarter, with significant growth and operational optimisation across most areas. However, the market reaction here as well may indicate that much of the growth was already “in the price”. In addition, a decline in orders casts a shadow over the strong results.

- Orders fell to SEK 18.2bn, translating into an order backlog worth SEK 274bn.

- Sales revenue increased to SEK 19.2bn, representing organic growth of 23.6%.

- A particularly positive surprise was operating profit, which rose 32% to SEK 1.92bn, lifting the EBIT margin to 10%.

- Management pointed to exceptionally strong demand growth for surveillance and monitoring systems. Sales in this segment rose by more than 30%.

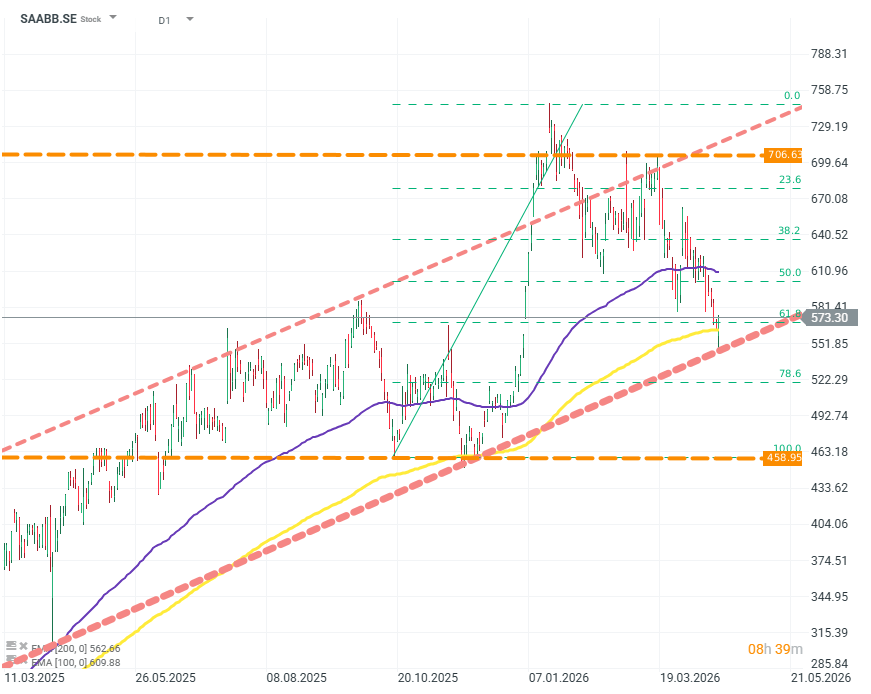

SAABB.SE (D1)

On the chart, the earnings release coincided with the defence of key levels: the EMA200 moving average and the lower boundary of the long-term upward channel. Source: xStation 5

Lockheed Martin

Expectations for the company were high ahead of the earnings release. On the back of current and anticipated increases in defence spending, shareholders expected Lockheed to justify the more than 40% rise in valuation since the beginning of the year. Investors were looking not only at revenue but also at profitability, the company still has a margin gap to close versus competitors.

- Revenue expectations were around USD 18.3bn, with EPS of about USD 6.75.

However, the company failed to meet market expectations.

- Sales revenue came in at only USD 18.0bn.

- EPS was USD 6.44.

- This implies net income of USD 1.44bn and an operating margin of 8.9%.

On a segment basis, the disappointment is concentrated in avionics and missiles.

- The avionics segment posted a year-on-year decline in sales to USD 6.95bn. The company cited losses of USD 325m and a revaluation of F-16 fighter-jet contracts that cost USD 145m. The C-130 program is also causing issues. Ultimately, operating profit in this segment fell 14%.

- The missiles segment performed better, but given the scale of demand from the U.S. government and allies, growth is well below expectations. Sales revenue rose only 8% to USD 3.64bn. The margin was unchanged at 13.7%.

- Management highlighted USD 190m in revenue related to expanding production capacity for PAC-3, JASSM, LRASM and PrSM missiles. These munition types currently represent one of the most acute shortages for both the U.S. and NATO as a whole.

- Rotary-wing aircraft and command-and-control systems is another segment that posted a meaningful decline. Revenue fell to USD 3.9bn, operating profit dropped by more than 20%, and the operating margin slid to 10.6% (previously 12%). The declines stem from a mix of weak sales volumes, internal restructuring, and revaluations of the CH-53K, Seahawk and Black Hawk programs.

- The space segment picture is mixed. Revenue increased to USD 3.42bn, but operating profit and margins fell by nearly 30%. The company attributed this to low profitability in the commercial/civil initiatives in which it participated.

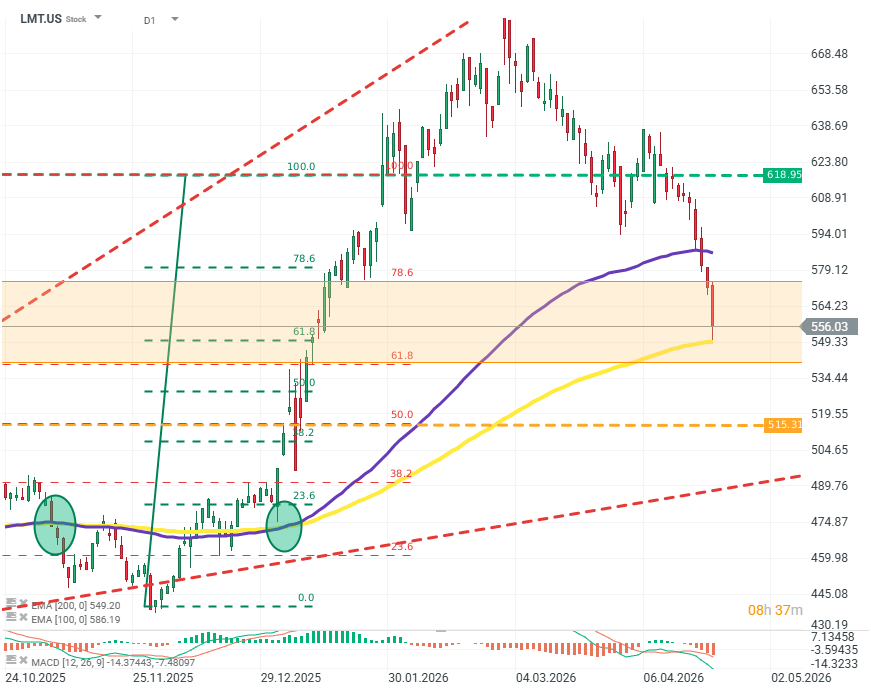

LMT.US (D1)

After paying its dividend in early March, the company lost momentum and reversed trend, falling by around 20% from the local peak. The price only clearly stabilised at the EMA200 moving average. From a technical perspective, to prevent further declines, the stock must at least hold within the consolidation channel between FIBO 68 and FIBO 71; buyers should also aim to defend the EMA200. Source: xStation 5

US Open: AMD and SpaceX failed to impress, but the broader market remains resilient

Shopify earnings: "Monstrous quarter"

Arista Networks Beats Expectations and Provides Fresh Support for the AI Investment Cycle

Market wrap (05.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.