The Non-Farm Payrolls (NFP) report scheduled for 14:30 is a key source of information on the condition of the U.S. labor market from the Fed’s and monetary policy perspective. Under normal conditions, the reading would be the main focus of financial markets, but much attention today is being diverted by the dramatic breakdown in relations between Donald Trump and Elon Musk. A reading below expectations would shift focus back to macroeconomic fundamentals, likely affecting Wall Street sentiment, especially given the series of weak ADP releases.

What are markets expecting? 📄

-

Job creation in May is expected to slow to around 125k (previous: 177k)

-

Unemployment is expected to rise to 4.3%, the highest level since October 2021

-

Wage growth is expected to remain stable, with average hourly earnings rising 0.3% m/m and 3.7% y/y

-

The expected job gain is still far from signaling a recession, but alignment between ADP and NFP data would be a clearer signal to the Fed that the labor market is starting to show signs of weakness.

-

According to Goldman Sachs, a reading below 100k could generate a drop in the S&P 500 of around 0.25–1.5%. Expectations for rate cuts in the U.S. could also rise sharply. The money market currently prices in two full cuts by the end of 2025.

Fed expectations 🎙️

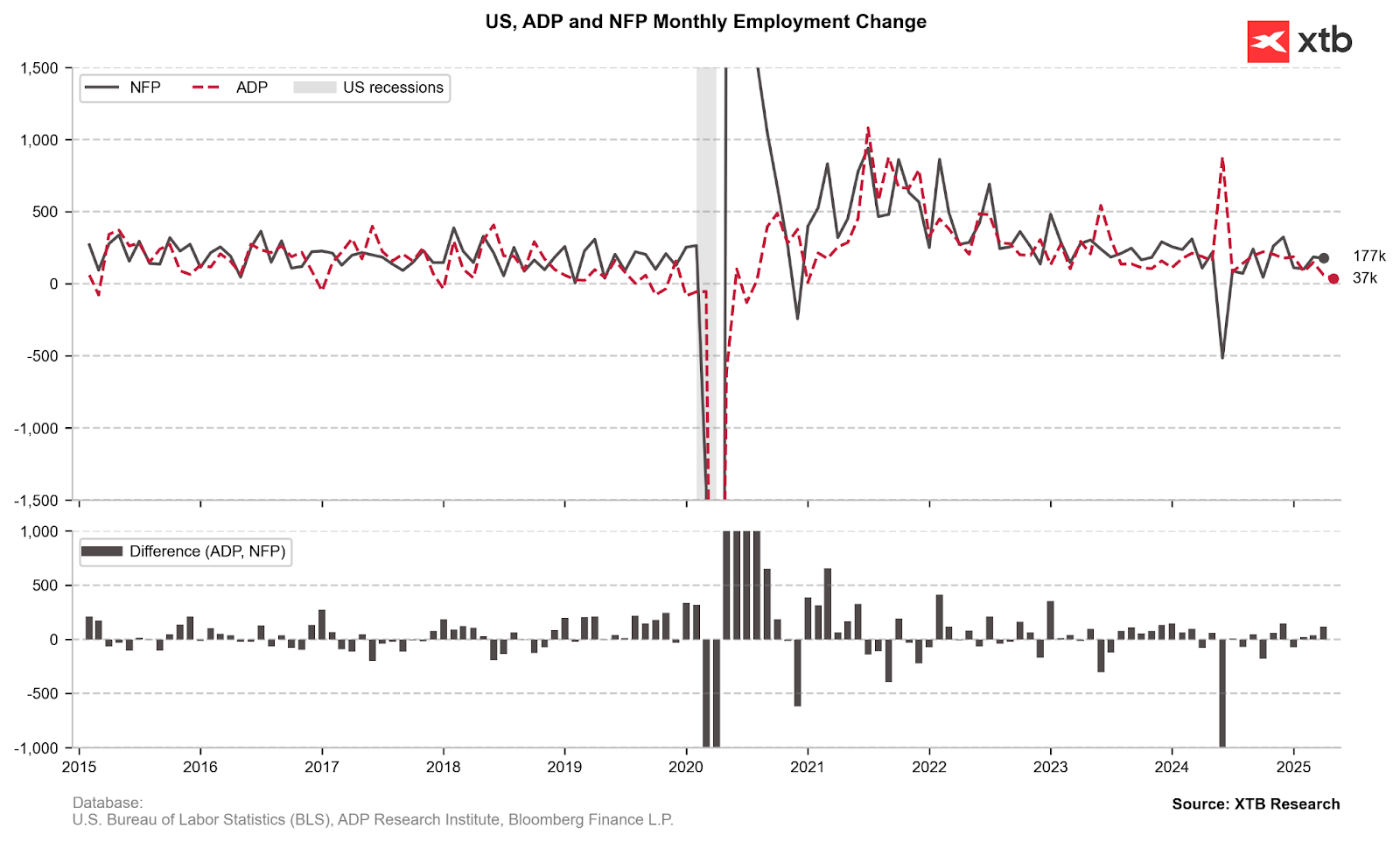

Ahead of the May NFP labor market report, the Federal Reserve faces a difficult challenge — balancing inflation risks with subtle signs of labor market weakness. Recent FOMC member comments indicate that the current interest rate level is seen as appropriate, with future decisions to be made cautiously, based on incoming macroeconomic data. However, if the upcoming NFP report proves as weak as the last two ADP readings, it could serve as a serious warning signal for the Fed. The ADP report published Wednesday showed that the private sector created only 37,000 new jobs in May — the lowest monthly increase since March 2023 and far below the projected 110,000.

Source: XTB Research

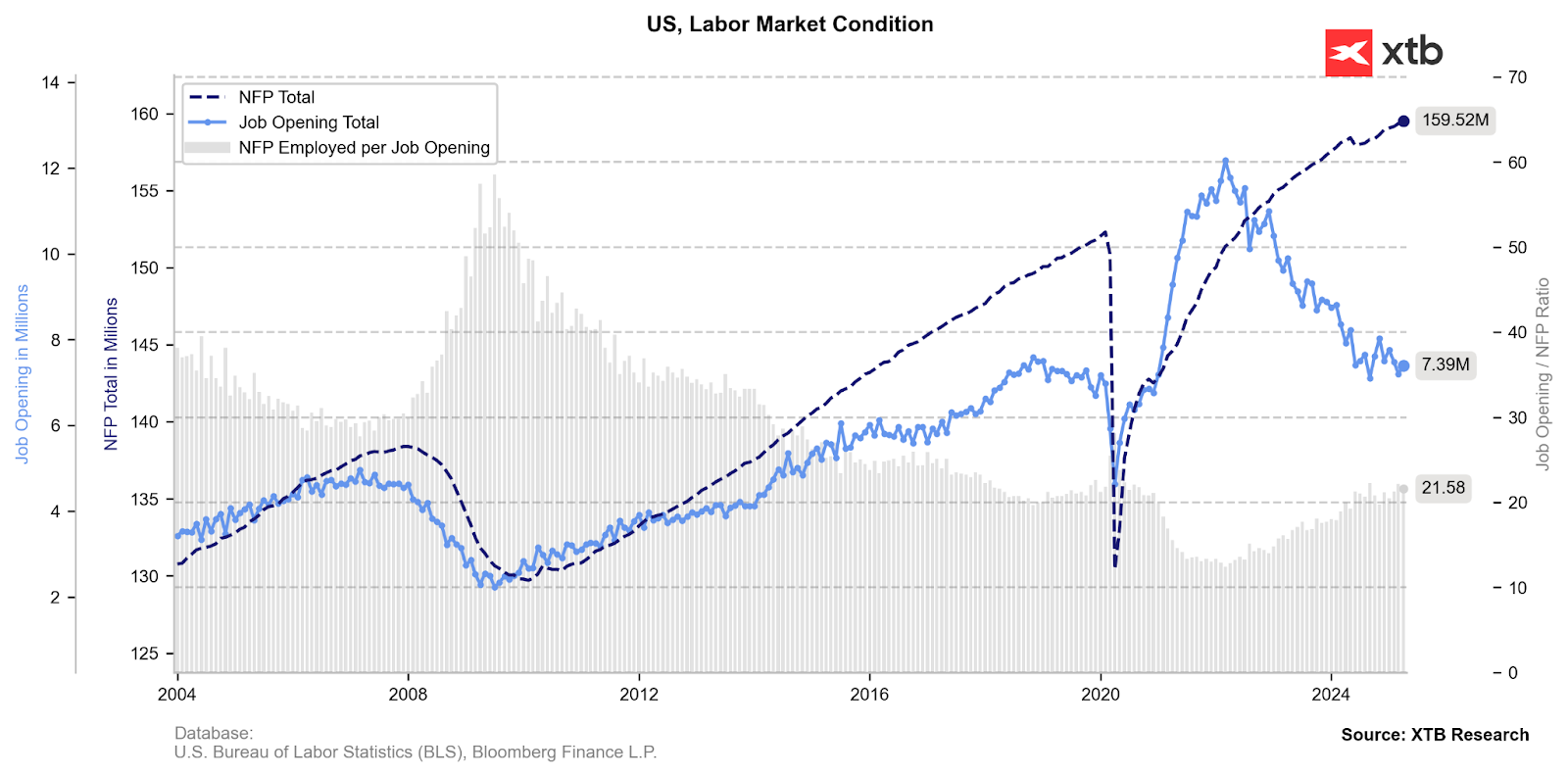

A somewhat more optimistic view of the labor market comes from job opening data. The April reading exceeded expectations, and the long-standing downward trend appears to be stabilizing at over 7 million openings.

Source: XTB Research

Potential scenarios 🖋️

Weak NFP report (below 100,000 new jobs):

- Implications: Significantly lower job growth may intensify concerns about a cooling labor market.

- Fed reaction: This outcome could increase the likelihood of considering a rate cut in the near term. On the other hand, the Fed is unlikely to act based on a single weak print.

Moderate NFP report (around 120,000–130,000 jobs):

-

Implications: A result in line with current forecasts, indicating gradual but non-alarming slowdown.

-

Fed reaction: The Fed may continue its "wait and see" strategy, maintaining current rates while monitoring further data.

Strong NFP report (above 160,000 jobs):

-

Implications: Strong job growth would suggest labor market resilience despite external pressures.

-

Fed reaction: This could be interpreted as a signal to maintain or even reinforce the current policy stance.

EURUSD (M15)

The euro is losing ground against the dollar today, in line with a mild rebound of the U.S. currency against all G10 currencies. After a series of declines, the dollar finds a moment of relief – earlier weakness stemmed from U.S.–China tensions and disappointing macroeconomic data this week (e.g. ADP, ISM). The EURUSD pair has fallen below both the short- and long-term moving averages on the M15 chart (SMA50 and SMA200), but remains above the new psychological support level at 1.14. The dollar’s recent weakness was driven by uncertainty and turmoil surrounding U.S. trade policy, but exceptionally weak labor market data (NFP) could spark speculation about potential Fed rate cuts, placing additional pressure on the dollar.

Daily Summary: A sell-off with a spin-off

Three Markets Worth Watching Next Week (17.07.2026)

Iran Escalation: What to Watch and What to Expect

US OPEN: The market extends losses as investor concerns grow

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.