Inflation is clearly declining around the world, although it is still treated as a big problem by most central banks, so high interest rates must be maintained. Nevertheless, for some regions it can be seen that the battle against inflation is almost won. Will we be able to say this about the United States?

Expectations are quite optimistic looking at year-on-year changes, but still show an increase in inflation on a monthly basis:

- CPI for May is expected to fall to 4.1% YoY against the previous reading of 4.9% YoY

- Core CPI is expected to fall to 5.3% YoY against a previous reading of 5.5% YoY

- Monthly CPI is expected to rise by 0.2% MoM against a previous reading of 0.4% MoM

- Monthly core CPI is expected to rise by 0.4% MoM against a previous reading of 0.4% MoM

- The spread of expectations for the headline reading is small, indicating between 4% and 4.2%

As can be seen, the magnitude of the decline in headline inflation is expected to be sizable, mainly due to the negative impact of energy and food prices, although a sizable potential impact of the decline in services prices can also be seen. This in turn could lead to a higher decline in core inflation. Expectations for core inflation on a monthly basis alone are quite high, given the fall in services prices and the small fall in used car prices.

Key inflation charts:

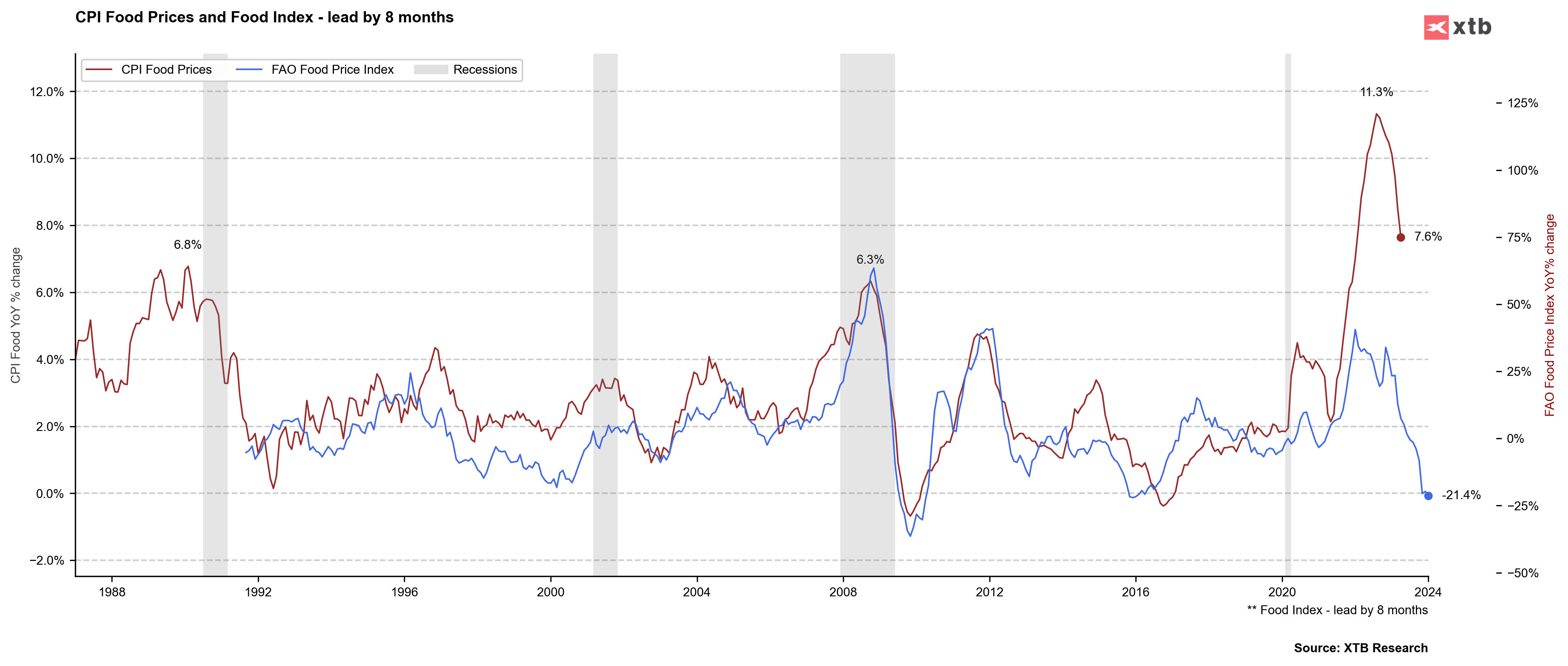

Food inflation has the potential for a massive drop, given changes in the FAO price index, which is falling at its strongest since late 2015 and early 2016. Source: Bloomberg, XTB

Food inflation has the potential for a massive drop, given changes in the FAO price index, which is falling at its strongest since late 2015 and early 2016. Source: Bloomberg, XTB

The price sub-index from the ISM services index remains above 50 points, but suggests a significant drop in headline inflation. Gasoline prices for May this year were also significantly lower than a year ago. The largest base effect related to energy prices will be for June, so the July increase may depend on the next inflation reading. Source: Bloomberg, XTB

The price sub-index from the ISM services index remains above 50 points, but suggests a significant drop in headline inflation. Gasoline prices for May this year were also significantly lower than a year ago. The largest base effect related to energy prices will be for June, so the July increase may depend on the next inflation reading. Source: Bloomberg, XTB

Inflation and the FOMC

We will learn the Fed's next decision tomorrow and it is expected that this could be the first holdout on a hike since March last year. The market only gives a 30% chance of a hike, but already sees a 60% probability for a hike in July. If, however, the Fed finds that the fight against inflation is having a positive effect, then there is a chance for the dollar to fall further and for Wall Street to accelerate towards its highs.

EURUSD

EURUSD is accelerating gains ahead of the CPI and Fed release and is breaking through the 1.0800 level. A decline in inflation to around 4% and a higher decline in core inflation could see the pair exit towards the 50.0 retracement of the recent downward momentum. EURUSD has maintained the range of the January-March correction, so in theory an attempt at a continuation of the long-term rise can be expected. However, for the moment, US yields still remain relatively high, which may suggest that the market still believes in the next Fed decision. If inflation surprises with a higher reading and the Fed clearly indicates that it may raise rates in July, then EURUSD could return to the 1.0700 level. Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Economic Calendar: Industry’s condition in the shadow of oil prices

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.