According to the head of Portugal's central bank, today's decision will be “easy.” This means that ECB interest rates will be cut by 25 basis points. The market is pricing the probability of this decision minimally above 100%. However, the key will be the bank's communication and future forecasts, which may determine the reaction on EURUSD. Of course, one should also keep in mind the impact of other events like the Fed decision next week or the publication of macroeconomic data not only from the Eurozone, but also from the US. ECB will decide at 1:15 PM BST.

Market expectations

- The consensus among analysts clearly indicates a 25 basis point cut in interest rates.

- This will be the second reduction in the current cycle. The ECB has announced that each decision is made separately, but the ECB may pause for more than one meeting before deciding to cut again

- This suggests that the next cut after the September one will be possible in December. Then we will know the next set of macroeconomic projections

- Most macroeconomic projections are expected to be kept unchanged, with a possible lowering of the economic growth outlook for the current year, based on weak PMI data or limited growth in some economies

- Inflation is expected to return to target in the latter part of 2025 and fall below target in 2026

- Market predictions are that the deposit rate will be cut in the 12-month horizon to 2.5% from the current level of 3.75% (the prospect of a cut at each meeting at the end of the quarter)

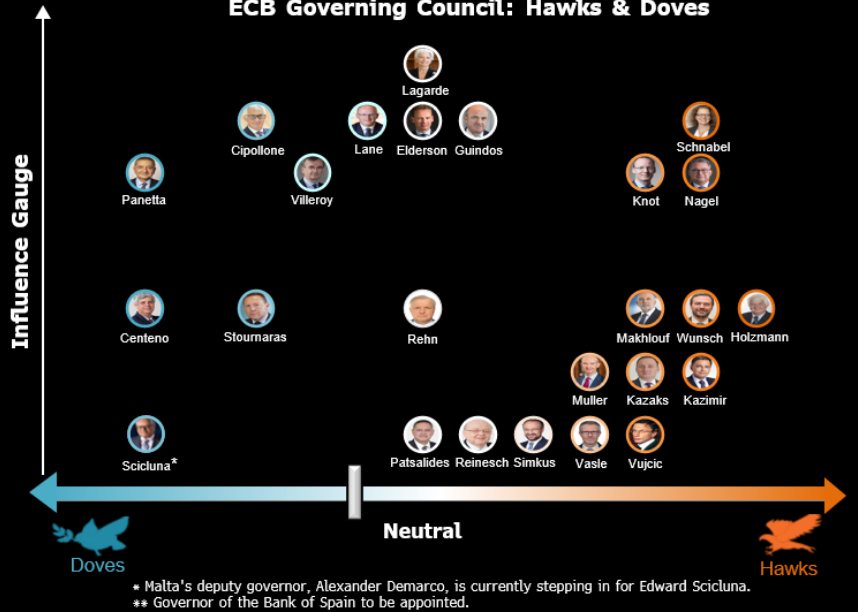

- The vast majority of members at the ECB are more hawkish, but a softening of communication cannot be ruled out given the weak macroeconomic data and the decline in wage growth, which remains key from the ECB's perspective

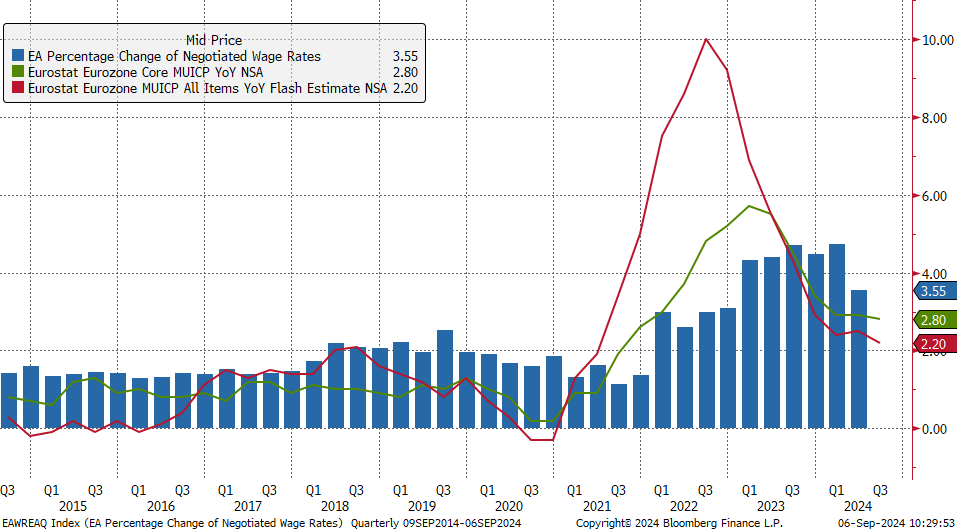

Eurozone inflation fell for August to 2.2%. Core inflation remains slightly elevated at 2.8%. Negotiated wage growth fell quite noticeably, which is an important indicator from the ECB's perspective. On the other hand, the ECB still has a problem with inflation in the services sector, which remains stable above 4%. Source: Bloomberg Finance LP, XTB

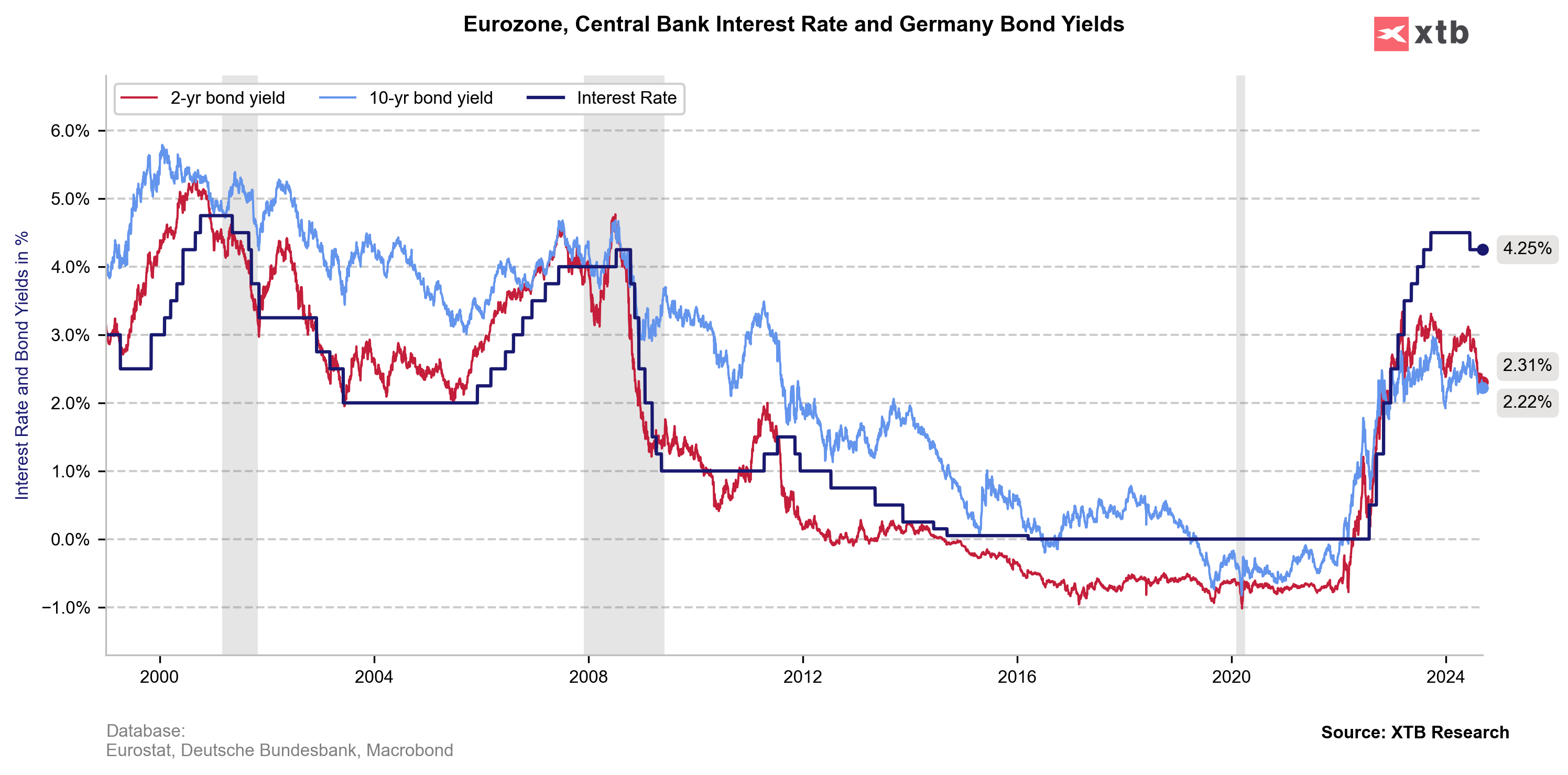

A large portion of ECB members remain hawkish, so the chances of accelerating the pace of cuts are rather slim. Of course, there is room for more reductions, given the stagnation in the European economy. Source: Bloomberg Finance LP Bond yields suggest that the target rate should be around 2.25-2.5%. Source: Bloomberg Finance LP, XTB

Bond yields suggest that the target rate should be around 2.25-2.5%. Source: Bloomberg Finance LP, XTB

How will the market react?

Today's decision is fully priced in by the market. Market participants are expecting a rather balanced communication from Christine Lagarde during the conference, which will start at 1:45 PM BST. Lagarde has maintained a neutral stance at recent meetings, indicating that decisions will be made from meeting to meeting. Maintaining the current tone should support the euro, given the likelihood of faster reductions from the Fed than from the ECB, however the economic situation in the eurozone remains weaker and markets may see this dynamic as even more important.

Any softening of communication from the ECB, however, could clearly weaken the euro, as this could suggest more rate cuts. However, this is not the baseline scenario at the moment. Maintaining the current tone and indicating that rates do not need to be cut soon due to existing inflationary risks (statements about service inflation or insufficient decline in wage growth) could strengthen the euro. In the first scenario, it will be possible to break through the support near 1.10 and fall further towards the support at 1.0950. On the other hand, it seems that the euro should recover, and the pair may test the level of 1.1050, supported also by expected Fed rate cut and better global markets sentiments after yesterday session on Wall Street. Given the high positioning on the euro, support from investors for a rebound remains significant.

Source: xStation5

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Breaking: US services remain strong, inflation pressures rise

GOLD eyes 4200 USD 🟡

US ADP employment below estimates! EURUSD extends gains 📈

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.