It is notable that from the lows at the beginning of this year, the EURUSD pair has risen by approximately 15% to its current levels. Such large movements in the foreign exchange market are extremely rare, and we are only halfway through the year. An increasing number of forecasts are now pointing to a sustained break above 1.20, although it is worth considering what has driven such a strong rally and what factors could influence future volatility.

General Dollar Weakness

Observing the EURUSD pair, we see enormous movements. However, if we consider other euro pairs, the volatility is not as pronounced. While the outlook for the European economy has certainly improved, even amid concerns about a trade war and the war in Ukraine, the primary driver of the pair’s rally has been a weak dollar.

Changes in the world’s major currencies against the euro since the beginning of this year. As you can see, not many currencies have gained against the euro, but at the same time, apart from the dollar and EM currencies, there is no major weakness. Source: Bloomberg Finance LP

This year, the American currency has been on the back foot due to the immense policy uncertainty surrounding Donald Trump. The dollar is losing its status as a safe haven, a trend also evident in the elevated bond yields. Amid fiscal uncertainty, Moody’s recently downgraded the US credit rating from triple-A, meaning that no major agency now considers US debt to be of the highest quality. While US debt remains robust and, crucially, is still the largest and most actively traded, even central banks are looking at the dollar with a hint of reluctance, preferring to increase their gold reserves instead. Over the past three years, central banks have added 1,000 tonnes of gold to their reserves annually.

Even with the US maintaining high interest rates, the dollar is faltering. Moreover, Trump’s questioning of Fed Chair Jerome Powell's position is also stoking global wariness towards the currency. The Wall Street Journal now suggests a new Fed head could be selected as early as this autumn, which could undermine Powell’s position for the remainder of his term, which expires next year.

Decomposition of factors influencing the shaping of the currency pair. The residual from the model (gray) has been positive since May, suggesting a potential overvaluation of the euro following its recent uninterrupted gains, especially in light of current monetary factors (higher interest rates in the U.S., dark green). On the other hand, geopolitical risk ("georisk", orange) is primarily supporting the common currency. Source: Bloomberg Finance LP, XTB Research

Improving Prospects for the Euro

Economic data from the United States has been mixed in recent months, as illustrated by the relatively low surprise index compiled by institutions such as Citi. In contrast, the same index for the euro area remains at quite high levels. The difference between these indicators is clearly favoring the euro, and furthermore, there is a prospect of further deterioration in the US and improvement in the euro area.

Economic surprise indices and EUR/USD. Source: Bloomberg Finance LP, XTB

Interest rates in the euro area are unlikely to be cut further, while those in the US are more likely to be reduced. However, it is worth noting that the level of interest rates in the euro area is significantly lower, which should benefit the economy. In the US, on the other hand, rates may still be high enough to dampen economic activity. This issue has been raised by Donald Trump, among others.

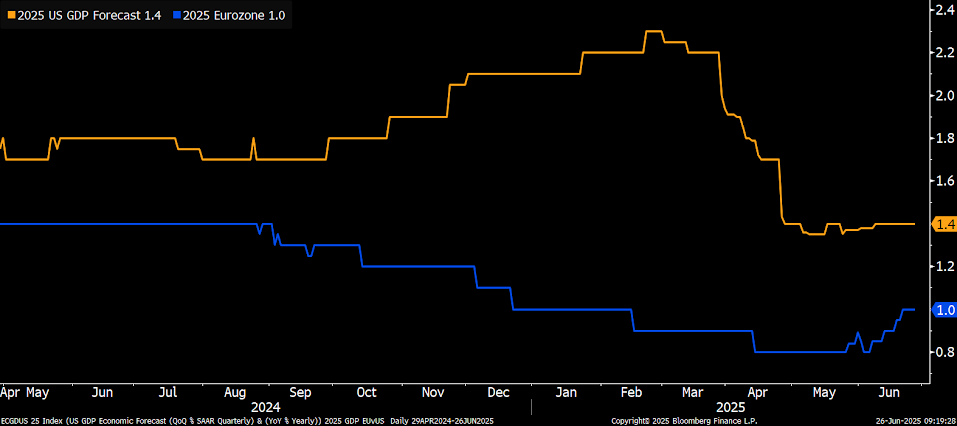

Growth prospects in Europe this year are improving significantly, while in the United States they have worsened, mainly due to the impact of Trump's trade tariffs. Source: Bloomberg Finance LP, XTB

There has also been significant discussion about a joint issuance of bonds in the euro area. History shows that the €750 billion joint recovery fund established at the beginning of the pandemic had a very positive impact on the European currency. In the event of a potential new euro area bond issuance, with funds earmarked for military and infrastructure spending, demand for safe European debt could also generate demand for the currency itself, not to mention stimulating the economy. According to Bloomberg, the euro appreciated by 15% in 2020, and a decision on joint debt could challenge the status of US debt and lead to further EUR/USD gains, potentially even reaching 1.40. This level was last seen in 2011.

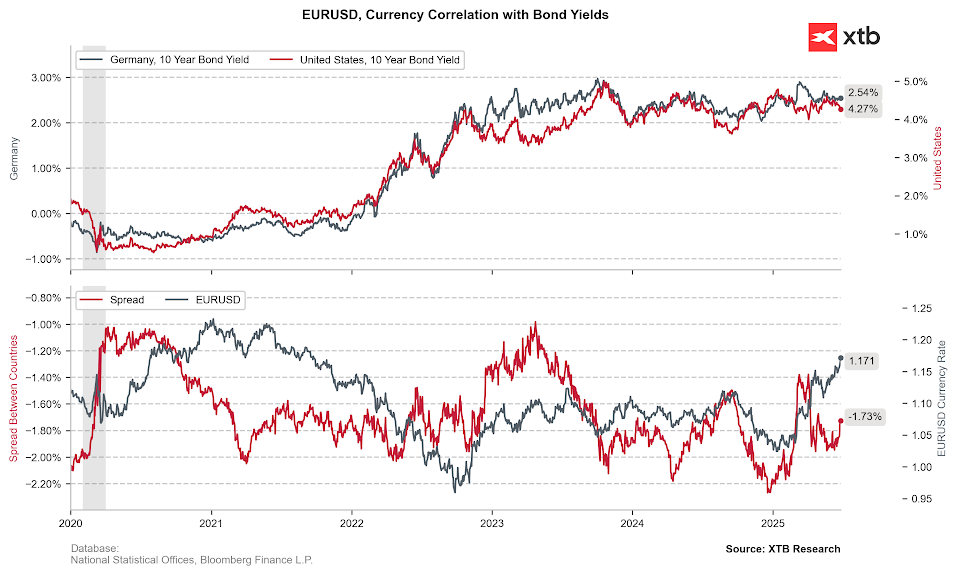

EUR/USD has not grown so dynamically since 2020. Nevertheless, the yield spread at the moment does not justify such high valuations, although it should be remembered that high US yields at the moment do not serve the dollar or the economy, given the need to service a huge debt at high interest rates. Source: Bloomberg Finance LP, XTB

A Weak Summer for the Dollar?

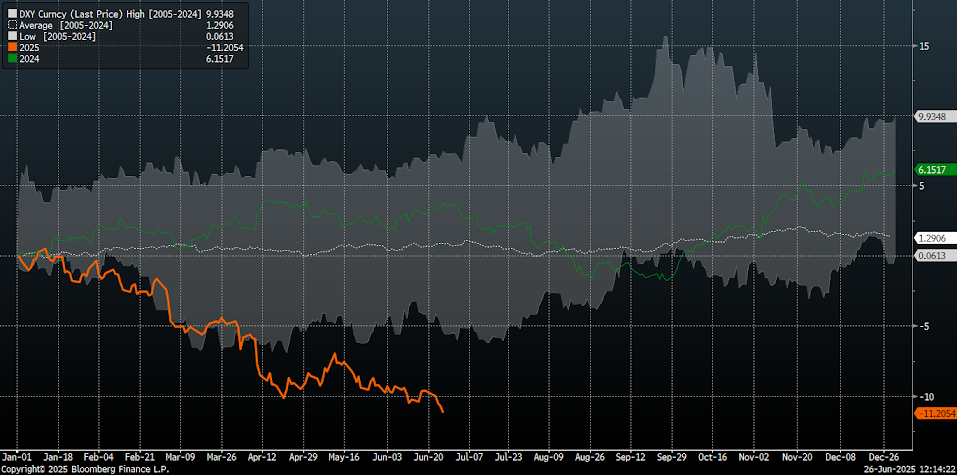

Historically, July has been a weak month for the dollar. This seasonality, based on the last 20 years, was also confirmed by last year's volatility. However, it is important to remember that July and August of this year will be highly significant for shaping the currency outlook. First, the suspension of reciprocal tariffs expires on July 9. Theoretically, new trade agreements could strengthen the dollar. In August, the US is also expected to hit its debt ceiling. While this event poses a risk to the dollar, it is most likely that the debt limit will ultimately be raised.

July is a seasonally weak month for the dollar, although it is worth noting that this year the dollar's weakness is already the biggest in 20 years. Source: Bloomberg Finance LP, XTB

EURUSD: A Technical Perspective

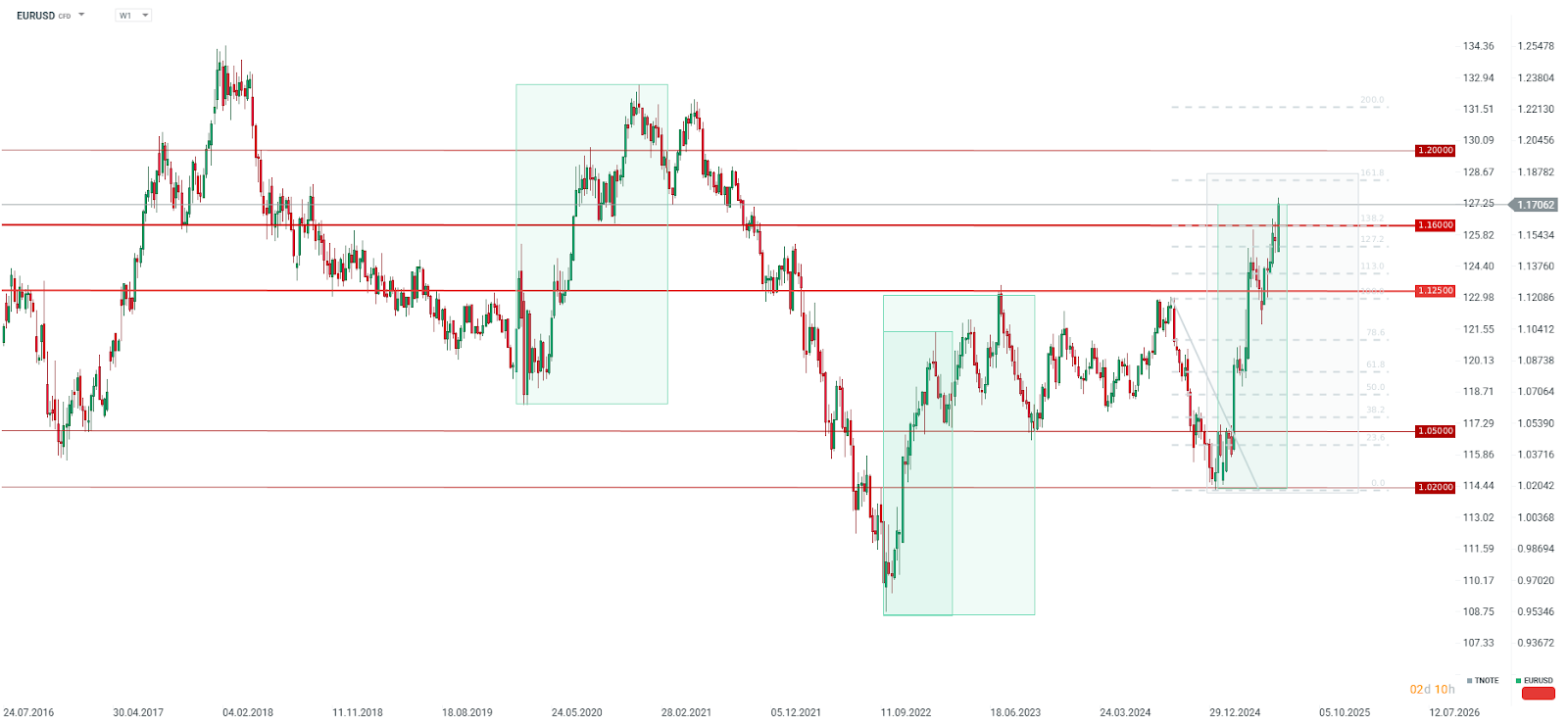

The EURUSD pair has broken above 1.16, following previous key resistance levels at 1.1250 and 1.1450. The next important resistance is now around 1.19, followed by 1.23, near the peaks of 2021. It is worth noting that EURUSD has risen similarly to the range seen in 2022/2023, but it has not yet completed the full range of the upward wave that began in early 2022 and 2020.

Source: xStation5

Dollar and Nasdaq facing a key test

Market Wrap: Tech lifts Europe to new record highs! Metals keep rallying despite stagnant USD (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

Economic Calendar: Will NFP Move the Market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.