- The US dollar is weakening ahead of the report's release.

- The market is pricing in no change to US interest rates through the end of the year.

- A weak reading could boost expectations for rate cuts.

- The US dollar is weakening ahead of the report's release.

- The market is pricing in no change to US interest rates through the end of the year.

- A weak reading could boost expectations for rate cuts.

The April NFP report on the US labour market is due to be released at 14:30, and will serve as a significant test for the dollar, which has been losing ground in recent days. The US currency remains under pressure despite this morning’s headlines, which cast doubt on the sustainability of the US-Iran ceasefire.

Latest reading

March saw a particularly strong reading. The number of non-farm payrolls far exceeded even the most optimistic expectations, reaching its highest level since December 2024 (178k). In contrast, the unemployment rate (4.3%) and wage growth (3.5%) fell unexpectedly. The reading signalled that the Fed is not forced to cut interest rates hastily, which, given the rapid rise in energy prices, was exceptionally valuable.

Geopolitical context

The situation on the geopolitical front remains tense. A glimmer of optimism came from Wednesday’s reports by Axios regarding work on a peace memorandum. Yesterday evening, however, the press was abuzz with speculation about a resumption of military action should a lasting agreement between the US and Iran not be reached before Trump’s visit to China. This is scheduled for 14–15 May.

Monetary policy

The data is of fundamental importance to the Federal Reserve, which has a dual mandate requiring it to focus on both price stability and maximising employment. The markets are undecided as to the direction the FOMC will take in the coming months. The inflation situation is causing growing concern, which led to a significant split within the committee at its last meeting – as many as three of its members opposed the so-called “easing bias”, i.e. the preference for lower interest rates in the medium term.

The April inflation reading, due next Tuesday, is expected to show the headline measure rising to 3.7%. However, policymakers will focus primarily on the core measure, wage growth and inflation expectations, as they are unable to exert much influence over inflation driven by supply-side factors, such as rising energy prices.

Markets are currently pricing in no change to interest rates until the end of 2026. A weak reading, suggesting that the labour market situation is deteriorating, moving away from the still relatively safe low fire-low hire status, may signal that the economy will need a monetary stimulus. This is, in any case, consistent with the rather dovish rhetoric presented by Kevin Warsh, who will take the helm of the FOMC from its next meeting.

A strong reading could, in turn, help the Committee to focus almost all its attention on the inflation situation, swelling the ranks of the hawks, which already appear to be numerous following the last meeting.

Current data

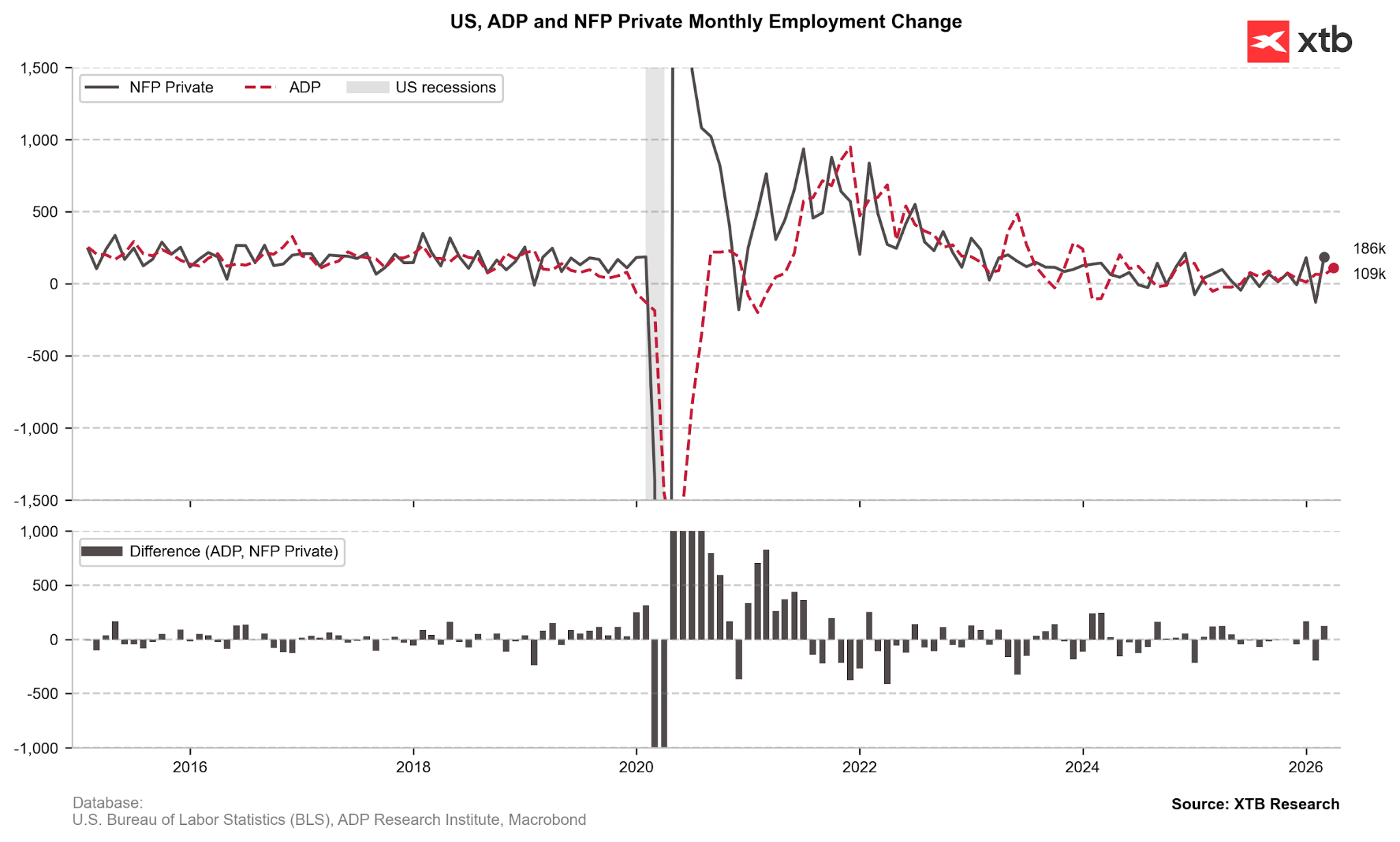

The most recent data – weekly jobless claims – are particularly noteworthy; a week ago they fell to 189k, the lowest level since 1969, remaining at low levels this week (200k). The ADP data also showed healthy levels (although since the pandemic, their correlation with the NFPs has been significantly weaker).

Chart: NFP and ADP data (2015 - 2026)

Source: XTB, 08/05/2026

Source: XTB, 08/05/2026

---

Michał Jóźwiak

Financial Markets Analyst at XTB

michal.jozwiak@xtb.com

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

BREAKING: BoE Keeps Rates Unchanged

🛢️Further escalation and tense situation do not drive oil further

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.