This week was particularly important, as several macroeconomic publications started to show a weakening labor market, which is considered a lagging sector. Mid-week, the job openings report showed a sudden drop in open vacancies. Today, at 1:30 p.m. BST, we received another labor data pack, which showed the unemployment rate unexpectedly rising above forecasts to 3.8%. The actual report indicated a small beat in both non-farm and private payrolls. Wage growth data came in slightly lower than expected at 4.3% YoY. The ISM index, on the other hand, registered a ninth consecutive month of contraction in the manufacturing sector, with key sub-indices such as New Orders and Imports still showing contraction. The Production Index showed marginal improvement. Industry respondents pointed to continuing soft demand, supply constraints, and economic uncertainties. Despite weak customer orders, some improvement was noted, such as a decrease in the percentage of manufacturing GDP that contracted, suggesting cautious optimism for stabilization in the sector.

Regarding the NFP report, a total of 187,000 jobs were added in August, beating consensus estimates. However, this was offset by downward revisions for June and July by 110,000 jobs. The unemployment rate rose unexpectedly to 3.8% from the 3.5% expected, as 736,000 workers joined the labor force.

What next? 🔍

Now, only the CPI report for August remains to be published on September 13, before the meeting on September 19-20, 2023. Therefore, the labor data publications this week had significant implications for the US economy, as they were one of the last readings before the next FOMC meeting.

What will the Fed do? 🔮

It should also be noted that the FOMC expects the unemployment rate to pick up by the end of the year. The Federal Reserve may view the latest labor data as a mixed bag that does not necessarily warrant immediate action on interest rates. These factors could give the Fed some room for caution. It can be interpreted that the labor market is gradually normalizing but not overheating. Federal Reserve FOMC member Mester commented that the job market is still strong but achieving a better balance. She pointed out that the 3.8% unemployment rate is still low and highlighted that inflation remains too high. Mester suggests that future policy will be data-dependent, focusing on the balance between over-tightening and under-tightening.

What market anticipates after this week? 🔴

After the publication, the probability rate suggests that the Federal Reserve will not raise interest rates in the next meeting, with the probability of the next interest rate hike dropping to just 7%. Market expectations are now shifting towards the possibility of a rate cut, with Fed Swaps fully pricing in such a move in May instead of June. Additionally, the lowered odds in Fed Swaps suggest that another rate hike this year is becoming less probable.

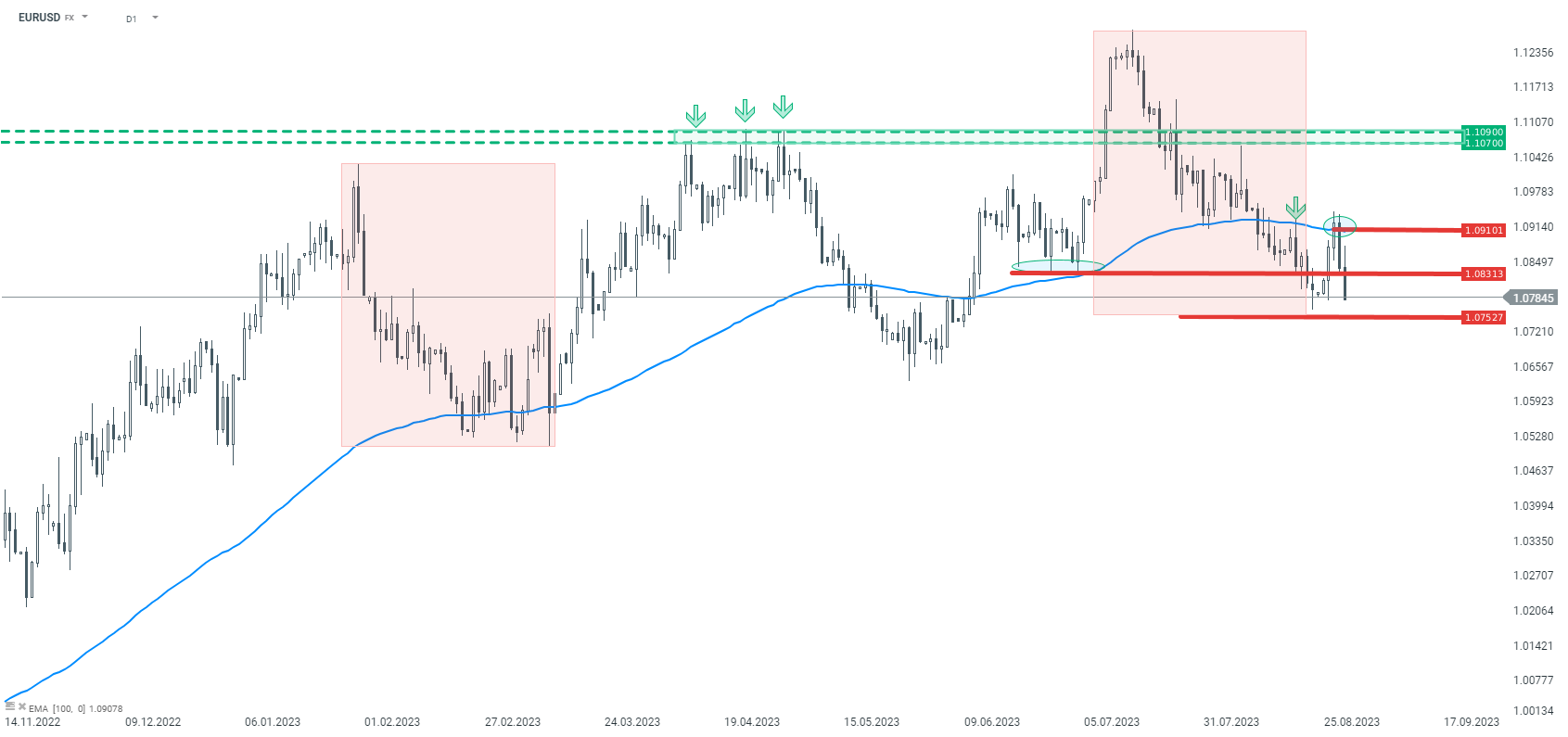

EURUSD erased entirely the rally that occurred just after the release of the labor market report. The pair not only wiped out the increases, but also fell below the level of $1.08. Currently a move towards the support at 1.0750 which results from the broad geometry pattern of 1:1 (marked as red rectangles) is probable. According to the overbalance methodology, as long as the price does not fall below 1.0750, the long-term trend is upward. However, in the short term, it seems that as long as the price does not return above 1.0830, the base scenario is further downside movement. A possible breach of the mentioned 1.0750 could lead to a breakdown of the trend and acceleration of the decline.

EURUSD erased entirely the rally that occurred just after the release of the labor market report. The pair not only wiped out the increases, but also fell below the level of $1.08. Currently a move towards the support at 1.0750 which results from the broad geometry pattern of 1:1 (marked as red rectangles) is probable. According to the overbalance methodology, as long as the price does not fall below 1.0750, the long-term trend is upward. However, in the short term, it seems that as long as the price does not return above 1.0830, the base scenario is further downside movement. A possible breach of the mentioned 1.0750 could lead to a breakdown of the trend and acceleration of the decline.

Source: xStation5

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

US OPEN: Shallow rebound in the shadow of a weak labor market

NFP much below expectations! 🚨EURUSD spikes 📈

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.