-

Current monetary policy stance remains appropriate.

-

Implications of the Middle East situation are uncertain.

-

Inflation expectations have risen sharply, mainly due to rising oil prices.

-

Inflation projections revised upward for the current year.

-

Long-term inflation expectations remain consistent with reaching the 2% target within the forecast horizon.

-

The Fed continues to remain in a mode of responding to inflation and labor market conditions.

-

Previous rate cut decisions should support the labor market.

-

Inflation likely to rise in the short term, but hard to predict in the long term.

-

The Fed will decide meeting by meeting.

-

Balanced statements from Powell. The Fed seems to remain in wait-and-see mode, at least until the end of Powell's current term.

-

Inflation remains on a downward path, even despite the recent oil crisis (duration unknown).

-

Previously, there were many signs in inflation that it was starting to fall (progress in limiting tariff impacts on product prices).

-

If no progress in inflation decline is seen by mid-year, rate cuts will be hard to expect.

-

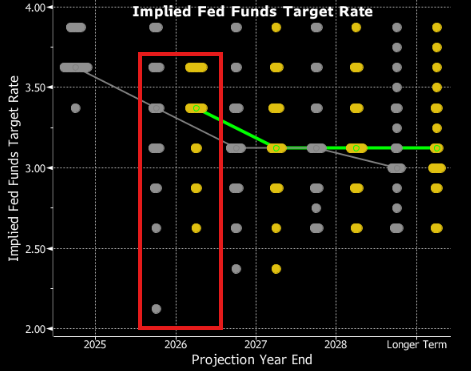

Slightly fewer FOMC members now support a cut, but consensus still points to it. Dollar strengthening.

-

Note that while consensus for a 2026 cut remains unchanged, fewer FOMC members now indicate it.

Source: Bloomberg Finance LP

- Oil shock may show in core inflation. If no inflation progress, no cuts.

- Slower tariff progress led to higher inflation forecasts.

- Partially higher forecasts due to elevated oil prices.

- Fed cannot fully assess how the oil shock will impact the economy.

- Oil shock could be partially or fully offset by increased domestic energy production (higher oil, gas extraction, etc.).

- Interest rates balance on the neutral-restrictive boundary.

- Key now to keep rates slightly restrictive but not overly so.

- Fed in a tough spot, balancing various risk factors.

Several somewhat hawkish comments led to sharper EURUSD drop below 1.150.

- Powell does not intend to leave his position while the DOJ investigation into irregularities continues.

- Powell has not yet decided whether to remain as a Fed governor after his term as chair ends. He will decide based on serving the American people and economy best.

- The labor market shows some signs of weakness, primarily in job creation. The balance of risks is negative.

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.