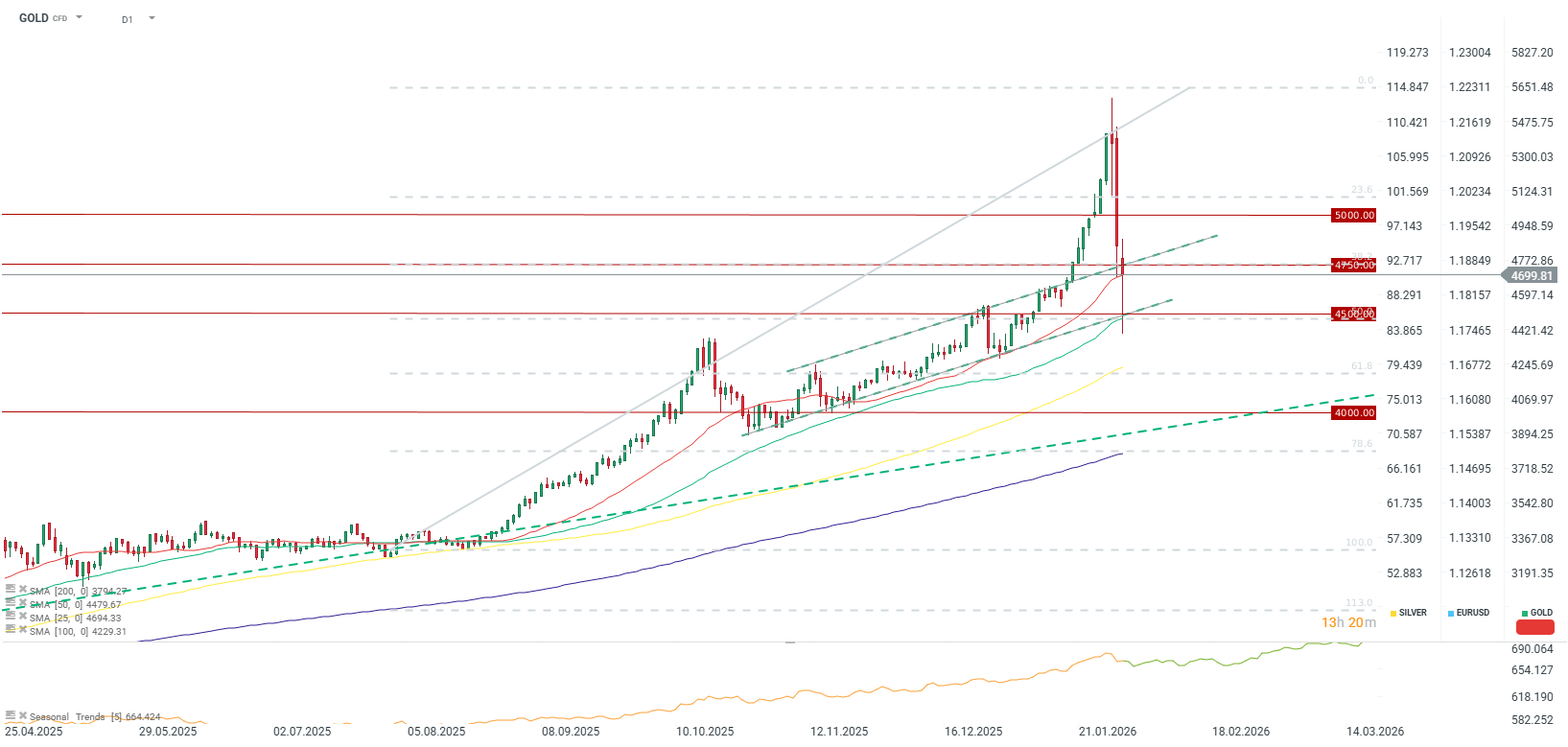

The gold price is significantly paring its losses, rebounding from near $4,400 per ounce to a level of almost $4,700. Notably, this bounce occurred around the 50.0 Fibonacci retracement level of the bull run that began in August 2025. Furthermore, the buffer zone between the 25 and 50-day Simple Moving Averages (SMA) remains intact for the time being.

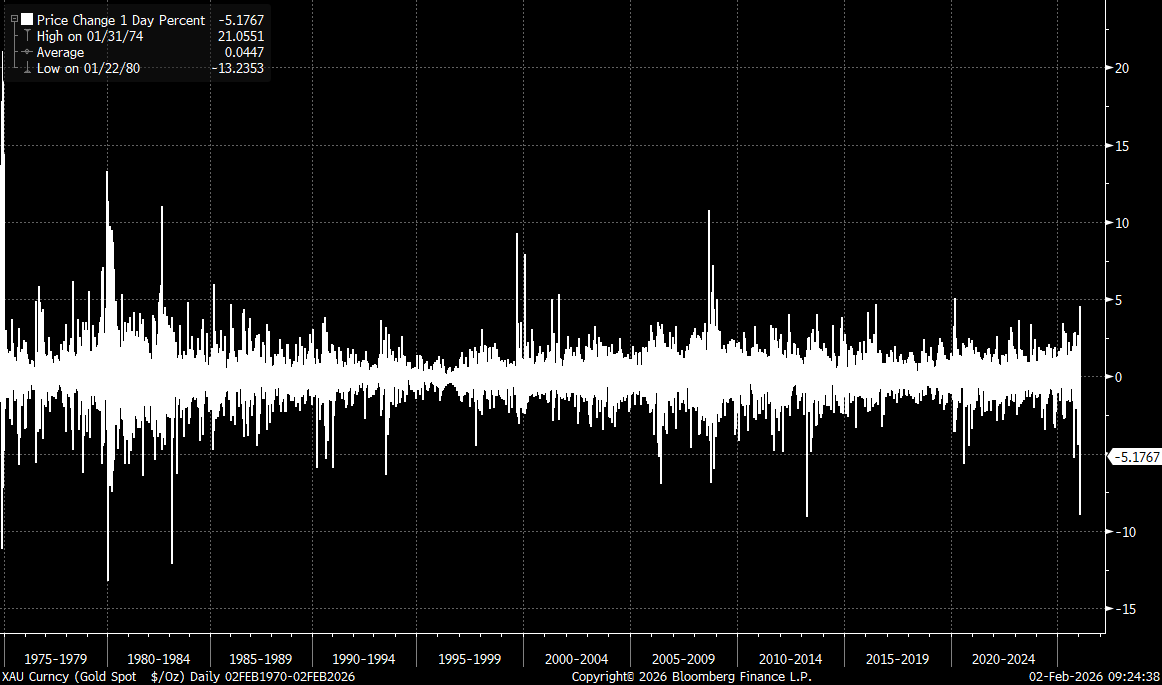

Friday’s price drop in the gold market was among the largest in history, yet it did not exceed 10%. By contrast, silver’s decline at one stage surpassed 30%. Source: Bloomberg Finance LP

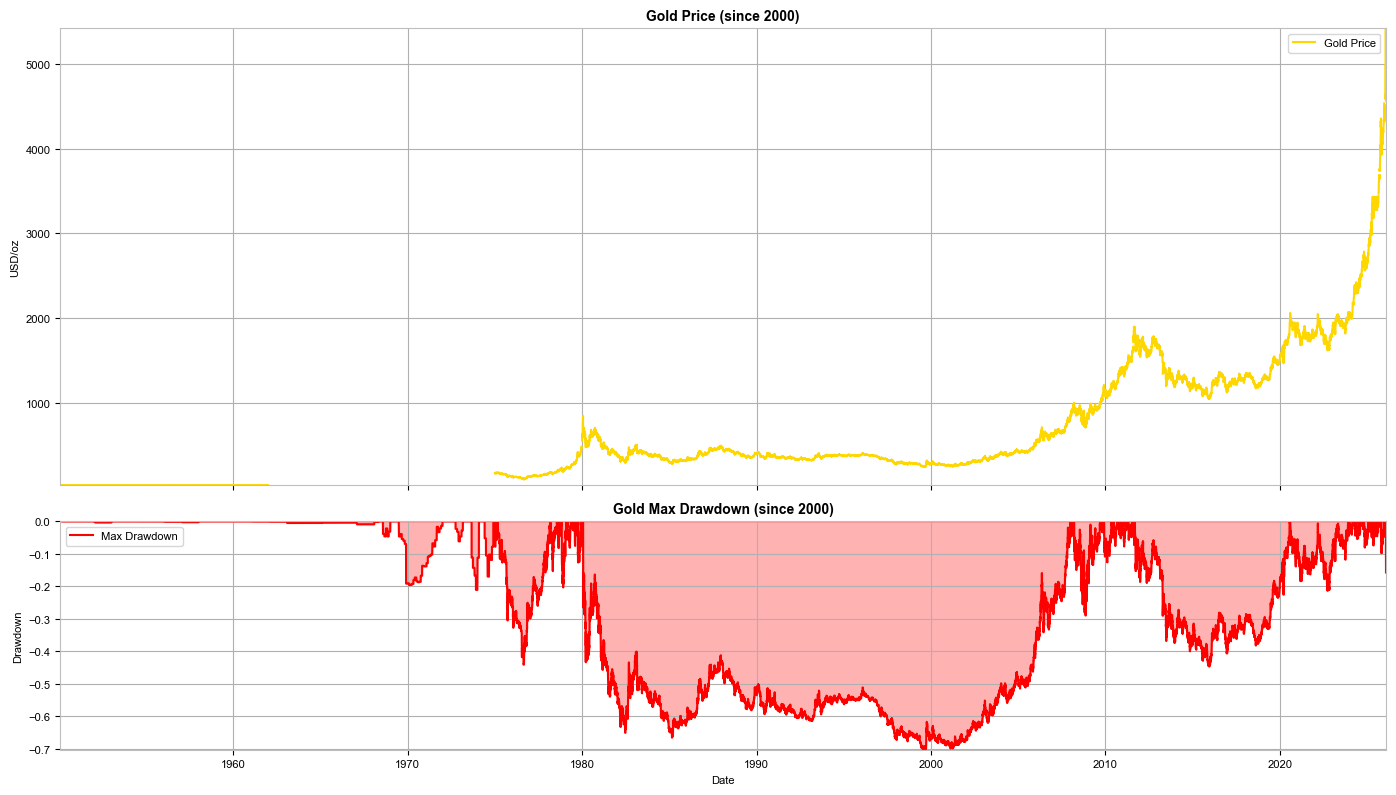

It is important to highlight that the demand structure for gold differs fundamentally from that of silver. In the gold market, we have not observed the same extreme signals from the options market, nor were there acute concerns regarding physical bullion delivery. Nevertheless, historical context is vital: in the past, gold corrections from all-time highs have reached as much as 40%, although the largest correction since 2020 has been limited to 20%.

Analyzing the period from 2020 onwards, the maximum correction reached 20%. Source: Bloomberg Finance LP

A daily close above $4,750 per ounce could signal that the correction in the gold market has run its course. In such a scenario, the objective would be a swift return toward the $5,000 psychological barrier. Conversely, should gold end the session closer to $4,500, the prospect of a deeper correction remains on the table. This could see prices retreat toward the long-term trend line, situated in the $4,000–$4,200 per ounce range.

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)

Cocoa loses 4% amid news from Ghana 🚩 What's next for the market?

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.