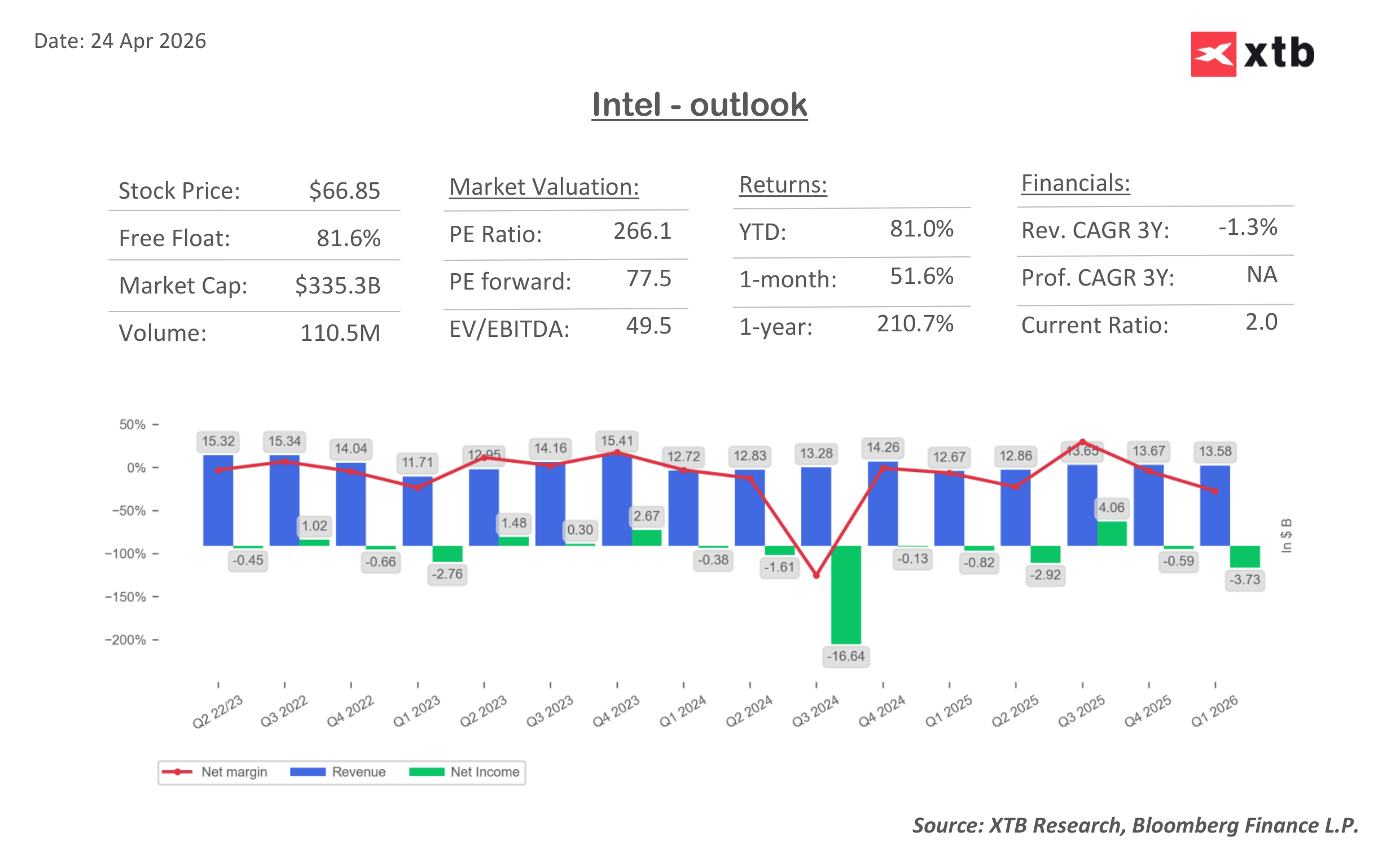

Intel’s results for the first quarter of 2026 clearly reinforce the view that the company is beginning to emerge from a multi-year period of operational weakness. The report itself delivered a solid beat versus expectations, but even more important are the forecasts for the coming months, which give the release a distinctly more growth-oriented tone and acted as a catalyst for a strong market reaction.

Key financial highlights for Q1

-

Revenue $13.58 billion, 7.2% YoY, above consensus

-

Adjusted EPS $0.29 vs expectations around $0.01

-

Gross margin 41% vs 34.5% forecast

-

Data Center & AI $5.05 billion, 22% YoY

-

Foundry $5.42 billion, 16% YoY

-

Operating income $1.67 billion vs $0.69 billion a year earlier

The scale of the positive surprise is visible not only in revenue, but above all in profitability. The increase in gross margin to 41% suggests improvements in both the sales mix and cost efficiency. This indicates that actions taken in recent quarters are starting to translate into tangible financial results.

The Data Center & AI segment remains the primary growth driver, posting 22% YoY. This confirms that artificial intelligence is already generating real and growing demand, particularly in server infrastructure. Increasing importance of inference and edge-related applications is reinforcing the role of CPUs within the broader ecosystem.

The first phase of the AI boom was largely driven by GPUs, where NVIDIA established a dominant position. However, there are growing indications that the next phase could shift the center of gravity toward CPUs, especially in the context of scaling and broader adoption of AI applications.

The foundry segment is expanding at 16% YoY and is gradually becoming a more meaningful part of the business mix. Improved capacity availability suggests that previous supply constraints are easing, supporting both shipment volumes and pricing.

Guidance remains the key focus for the market. For the second quarter, the company expects revenue in the range of $13.8 billion to $14.8 billion and EPS of $0.20, clearly above prior expectations. In addition, projected gross margin of around 39% points to continued improvement in profitability.

On a broader view, the company signals sustained strong demand and the potential for above-seasonal growth in the coming quarters of 2026, supported by AI expansion and improved supply conditions. This suggests that the momentum seen at the start of the year could continue into the second half.

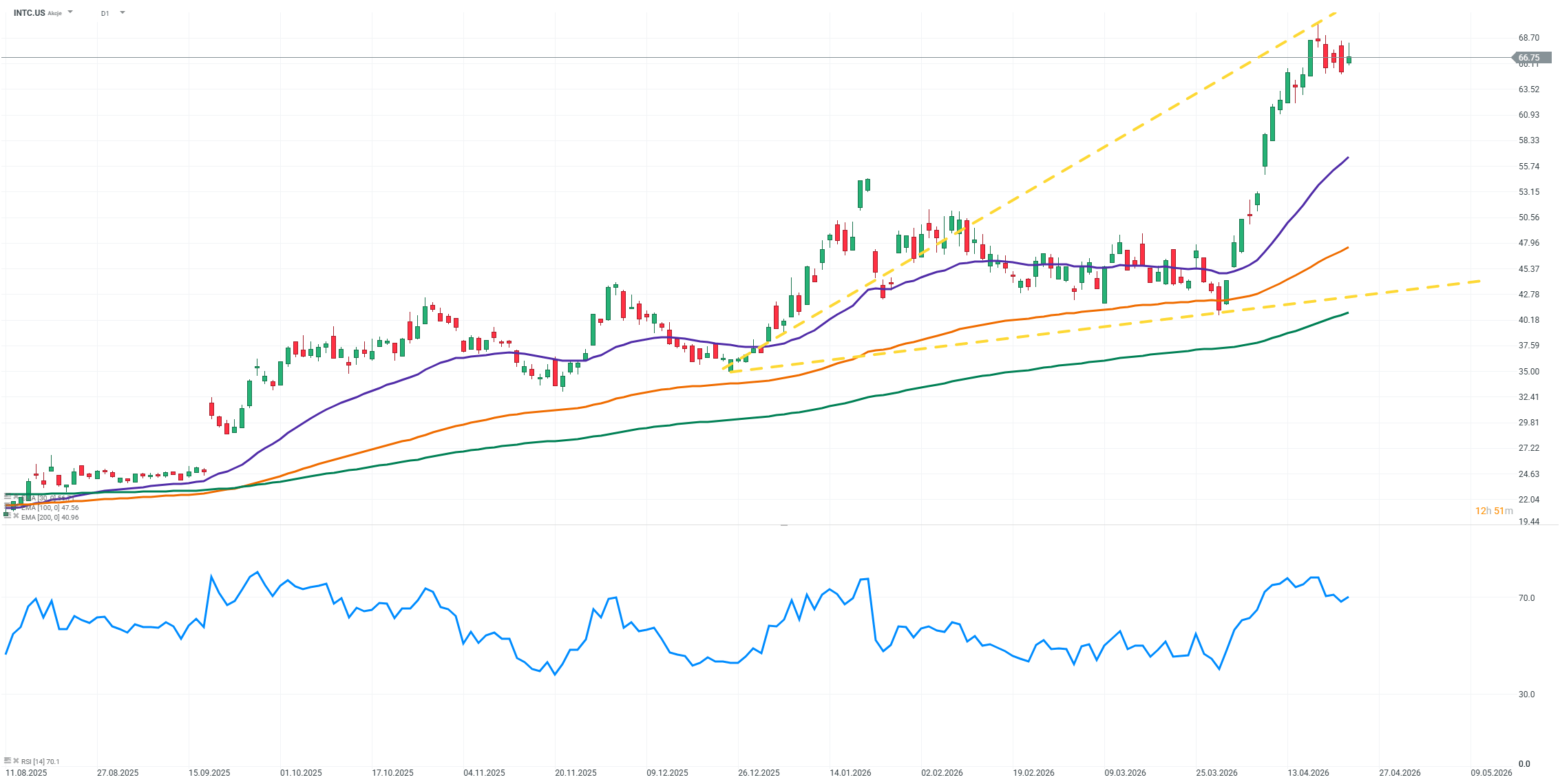

The market reaction was very strong, with the stock rising more than 20% in premarket trading, also lifting other companies in the semiconductor sector. It is worth noting that Intel shares have already gained more than 70% year-to-date.

Despite the clear improvement in results and increasingly visible operational stabilization, the company still faces a number of significant challenges. The most important among them remains the pressure from very high capital expenditures, which are necessary to execute the long-term strategy of rebuilding its position in the semiconductor manufacturing segment and expanding its own production capacity. The scale of these investments continues to weigh heavily on cash flows, meaning that the improvement in accounting earnings has not yet fully translated into a comfortable cash flow situation.

It is also important to remember that the company is still generating a net loss, which has slightly widened in the most recent period. This shows that the improvement at the operating level has not yet been fully reflected in the bottom line, largely due to persistently high restructuring and investment costs.

At the same time, the business transformation process remains complex and multi-stage, which means that the current improvement is to a large extent transitional in nature and requires continued disciplined execution of the adopted strategy. The company is simultaneously developing high-growth segments such as AI and foundry, while restructuring its traditional businesses, which requires maintaining a careful balance between investment spending and near-term profitability.

Overall, the reported results and forward-looking guidance point to a more credible improvement in the company’s fundamentals. Support from rising demand for AI solutions, improved capacity availability, and increasing operational efficiency creates a solid foundation for further performance improvement in the coming quarters. At the same time, higher market expectations mean that maintaining this trend will be crucial for the stock’s continued performance.

Source: xStation5

Who Will Surprise With Earnings Next Week? (07.08.2026)

US OPEN: Shallow rebound in the shadow of a weak labor market

Dollar and Nasdaq facing a key test

Market Wrap: Tech lifts Europe to new record highs! Metals keep rallying despite stagnant USD (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.