-

Crude oil remains stable ahead of the upcoming US–China summit. Brent oil is holding at a high level of around $107 per barrel after strong gains during the first two sessions of this week.

-

US equity index futures are recovering losses following the release of higher US inflation data. The US500 is currently up 0.3%, while the US100 is gaining as much as 0.8%. After yesterday’s declines, media narratives around so-called “buying the dip” have re-emerged. A similar rebound was also observed on the South Korean market.

-

Nvidia is rising by up to 2.5% in pre-market trading, supported by reports that Jensen Huang may accompany Donald Trump on his visit to China, potentially opening the door to new chip-related deals.

-

Global attention remains firmly focused on Beijing. As a reminder, a two-day visit by US President Donald Trump to China begins tomorrow. Key topics are expected to include Iran and the Persian Gulf, although observers do not anticipate any major breakthroughs.

-

France: Today’s April data showed mixed signals. CPI inflation came in at 2.2% y/y and HICP at 2.5%, both in line with expectations. However, the unemployment rate rose to 8.1%, indicating some weakening in the labour market.

-

Eurozone: The latest data confirm a slowdown in economic activity. Q1 GDP stood at 0.8% y/y, while industrial production fell by 2.1%, coming in well below expectations and highlighting continued weakness in the manufacturing sector.

-

GBPUSD is down nearly 0.2%, testing the 1.35 area amid political uncertainty in the United Kingdom.

-

Gold remains stable above $4,700, silver continues its upward trend, while copper has broken above $14,000.

Equities and corporate news:

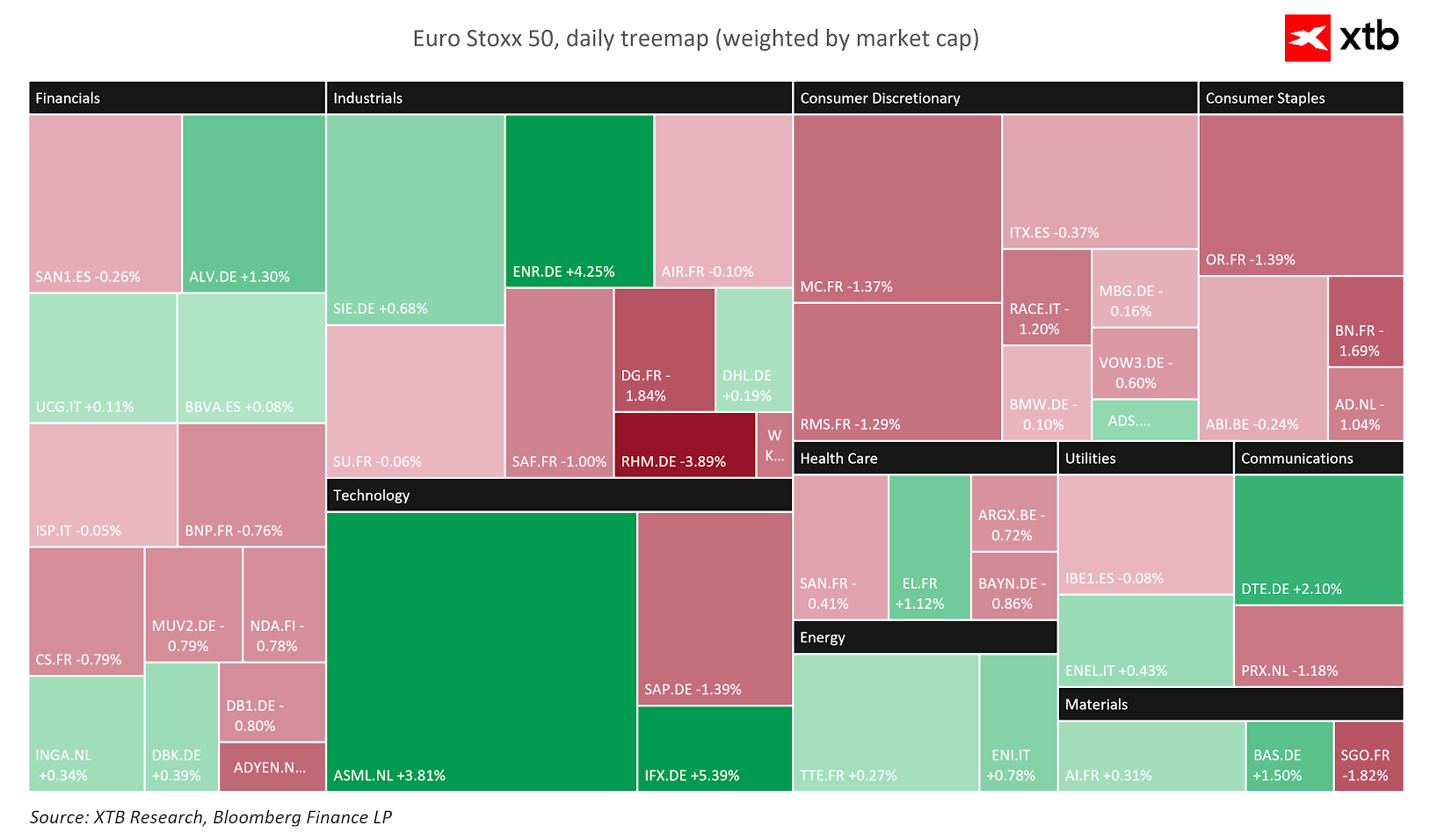

Deutsche Telekom (DTE.DE) delivered a strong start to the year, reporting a 6.5% increase in adjusted net profit and stable cash flows. The results were strong enough for management to raise its full-year 2026 guidance for operating profit and free cash flow.

Allianz (ALV.DE) generated €53 billion in revenue, while PIMCO and AllianzGI attracted €21 billion in new capital inflows.

Siemens (SIE.DE) reported a mixed set of results: revenue and net income slightly disappointed, but new orders came in strongly at €24.1 billion, significantly beating expectations. Despite some pressure on industrial margins, the company maintained its growth outlook and announced a large share buyback programme of up to €6 billion.

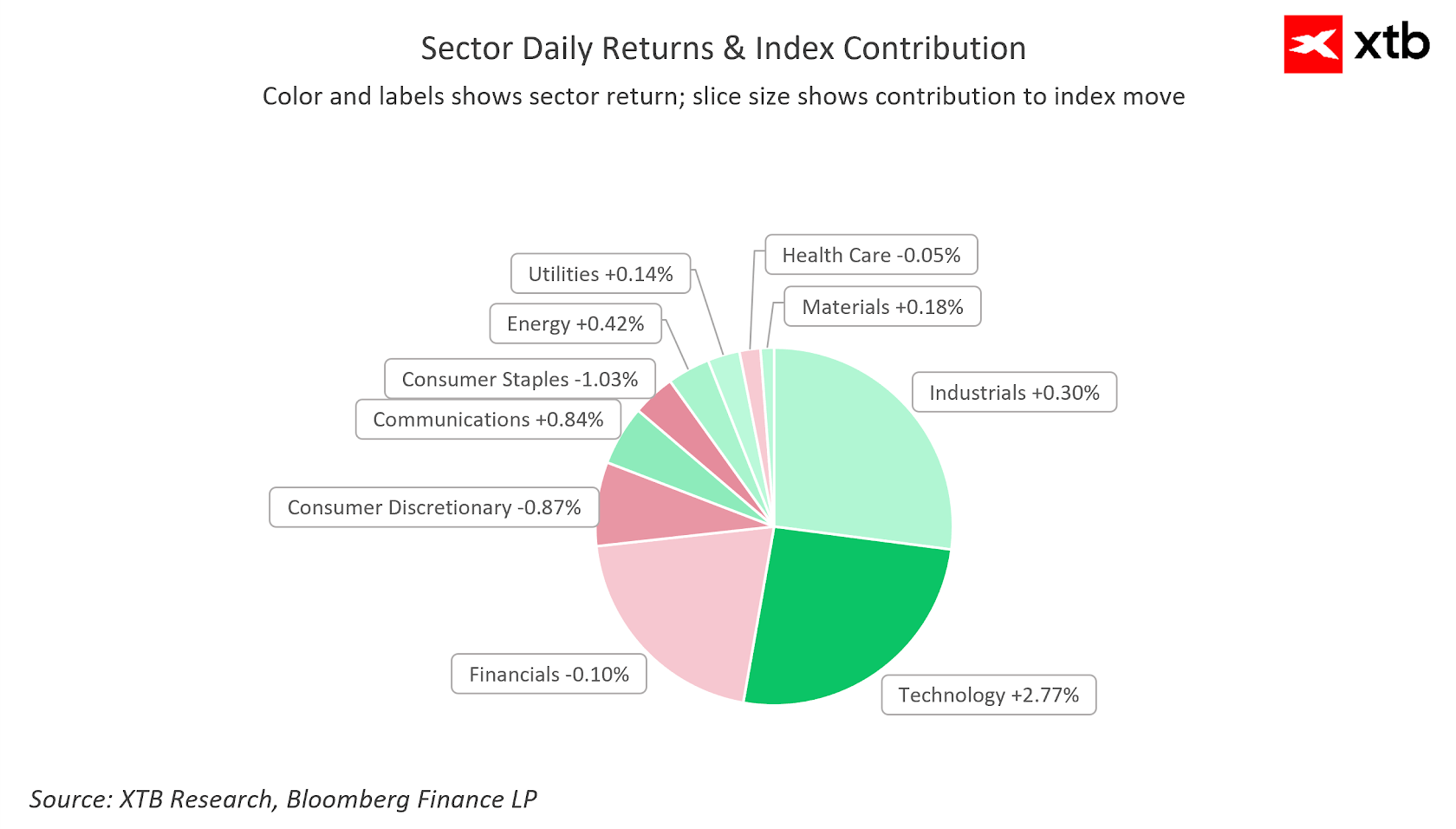

Volatility is visible today across major sectors of the economy. Notably, there is a renewed strong rebound in the technology sector. Source: XTB

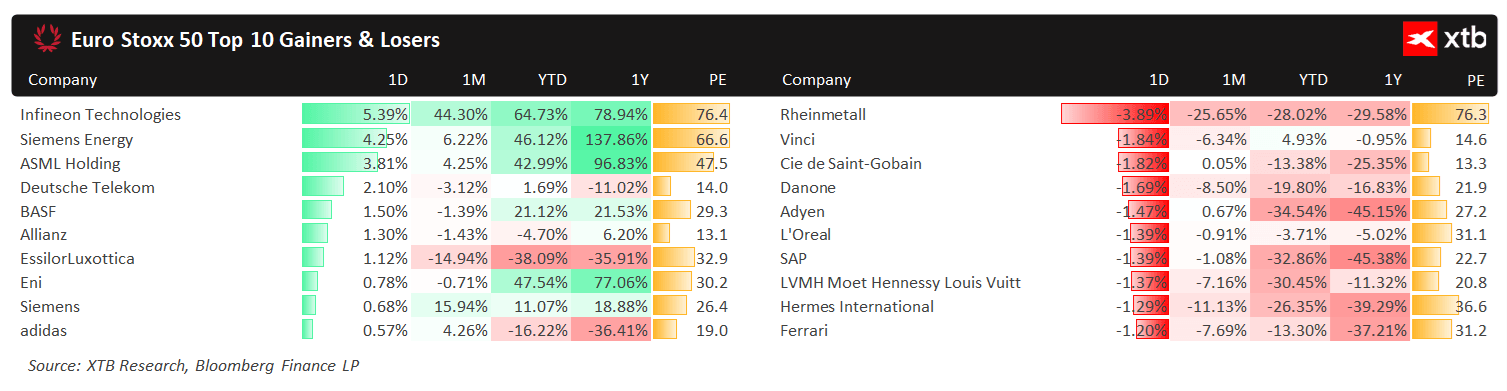

Sector dispersion highlights strong gains in ASML and Infineon, while consumer sector stocks are underperforming. Source: XTB

Among the most closely watched companies today are Siemens and Deutsche Telekom, both gaining on strong earnings. Meanwhile, Rheinmetall is extending its recent decline. Source: XTB

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.