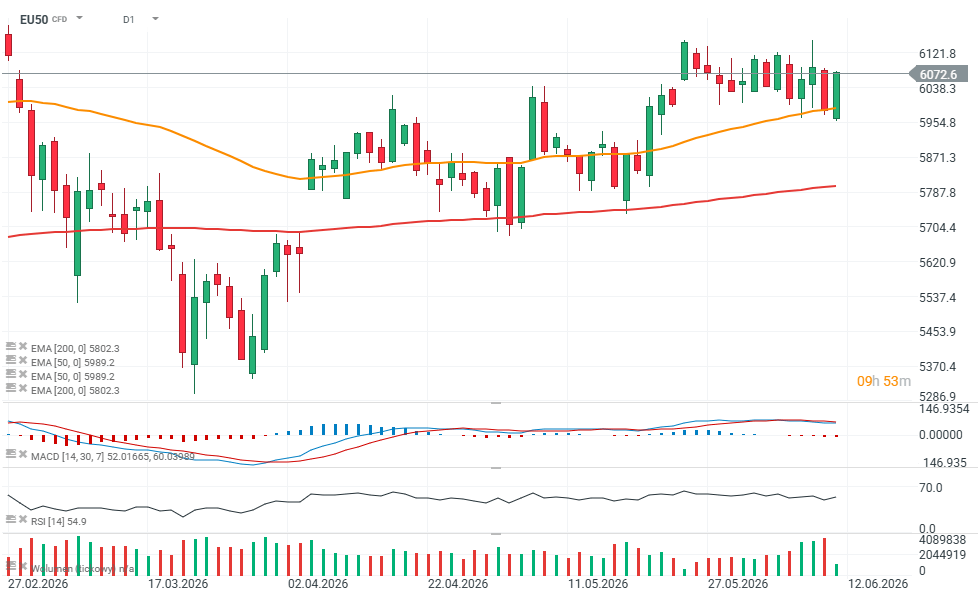

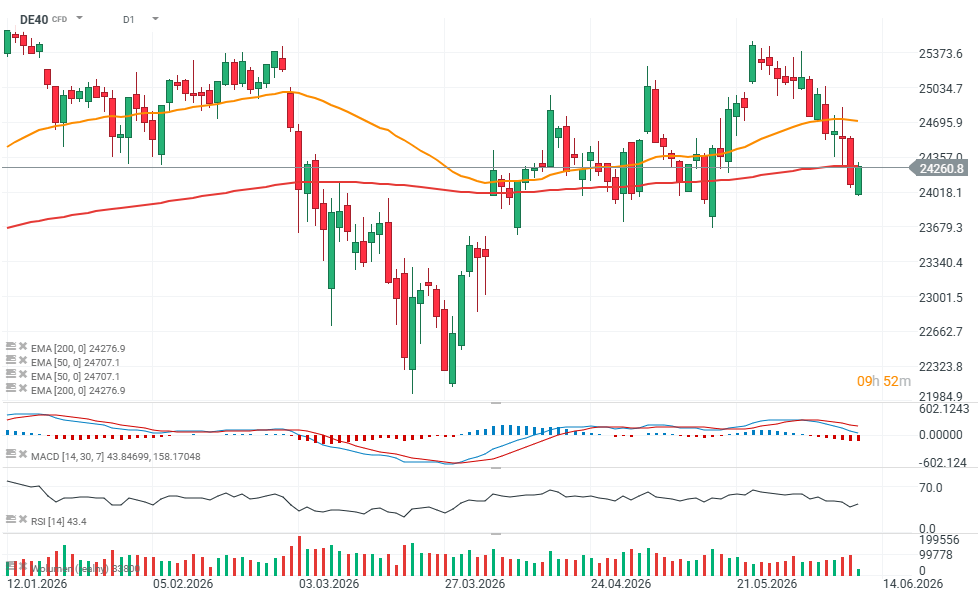

European equity markets are recovering from a recent sell-off as investors take advantage of lower valuations and buy into weakness. Uncertainty stems from escalating tensions between the United States and Iran, fueling concerns about Middle Eastern energy supplies and the inflationary implications of a prolonged conflict. Despite these headwinds, the "buy-the-dip" mentality remains intact across European markets.

Key Takeaways

- European equities are rebounding from recent declines and European Central Bank increased interest rates by 25 bps - in line with market expectations.

- Major European indices are holding up relatively well despite weakness across the technology sector.

- Rising bond yields and geopolitical tensions continue to limit risk appetite and increase uncertainty surrounding the sustainability of the market rally.

- Investors are looking beyond today's rate decision and focusing primarily on any signals from ECB President Christine Lagarde regarding a potential follow-up move in September.

Stocks in Focus

- SAP fell nearly 4% and Capgemini lost more than 3%, weighing on the European technology sector after Oracle unveiled aggressive capital expenditure plans.

- Hugo Boss gained more than 8% after Frasers Group launched a €2 billion takeover offer for the German fashion brand.

- Frasers Group declined around 2% as investors assessed the financial implications of the proposed acquisition.

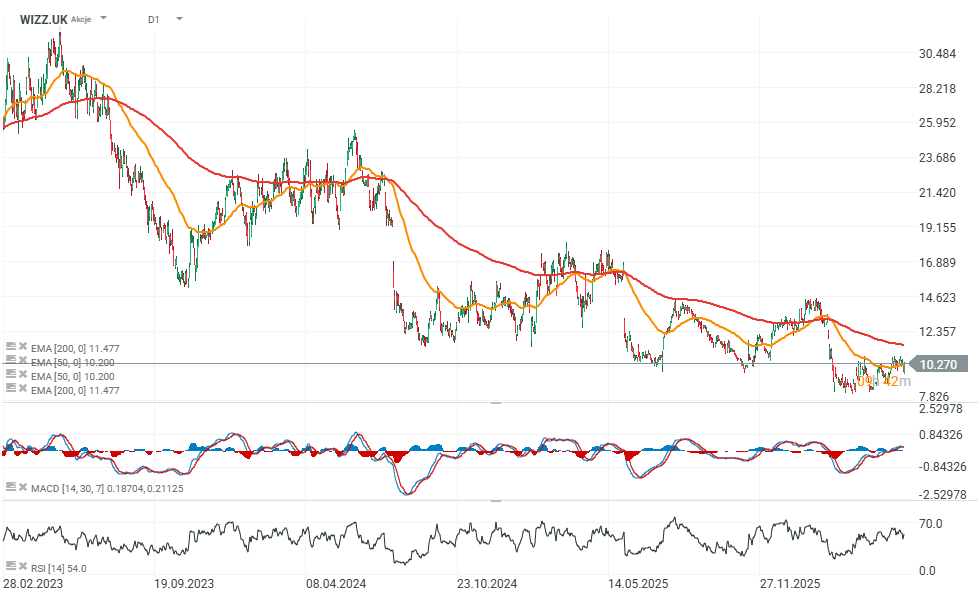

- Wizz Air advanced approximately 6% after reporting annual earnings that exceeded market expectations.

Source: xStation5

Source: xStation5

izz Air Returns to Profitability as Engine Headwinds Begin to Fade

Wizz Air delivered results that can be viewed as a major step toward the normalization of its business model after two exceptionally challenging years marked by Pratt & Whitney GTF engine issues. The airline returned to pre-tax profitability, improved cash generation, and maintained robust passenger growth despite ongoing operational constraints. Equally important, management signaled that the impact of aircraft groundings is gradually easing while highlighting potential growth opportunities arising from increasing pressure on weaker competitors. Investors welcomed the report, sending the stock up as much as 6% during Thursday's session.

Key Takeaways

- Wizz Air returned to profitability, generating €27 million in pre-tax profit and nearly €1 billion in free cash flow.

- The number of grounded aircraft related to Pratt & Whitney engine inspections declined from 42 to 30, with the issue expected to be fully resolved by the end of 2027.

- Management expects strong traffic growth in fiscal 2027 and sees opportunities to gain market share from financially weaker competitors.

Results Confirm Recovery of the Business Model

For the fiscal year, Wizz Air reported a pre-tax profit of €27 million, marking a return to profitability after previous losses. EBITDA increased 16% year-over-year, while passenger traffic rose 10% to 70 million passengers.

Cash generation was particularly impressive. Free cash flow reached almost €1 billion, up 22% from the previous year, despite the repayment of a €500 million bond in January 2026. EBITDA margin expanded to 23.2%, highlighting the company's ability to leverage scale and improve operational efficiency.

The balance sheet also showed meaningful improvement. Wizz Air ended the year with more than €2 billion in cash, stable net debt levels, and a reduction in net debt-to-EBITDA from 4.4x to 3.7x. Management reiterated its ambition to further reduce leverage toward approximately 2x EBITDA over time.

Engine Issues Still Matter, but Risks Are Gradually Declining

The Pratt & Whitney GTF engine inspections remain the airline's biggest operational challenge. For nearly two years, the issue has constrained capacity growth and forced the temporary grounding of a significant portion of the fleet.

However, recent developments indicate clear progress. The number of grounded aircraft fell to 30 from 42 a year earlier, and management continues to expect all affected aircraft to return to service by the end of calendar year 2027.

From an investor perspective, this is arguably the most important takeaway from the report. It suggests that the market is beginning to see a path toward unrestricted fleet utilization and a return to normal growth dynamics.

Wizz Air Refocuses on Europe and Prioritizes Profitability

Management continues to reshape the network, concentrating resources on its core Central and Eastern European markets. A significant portion of capacity previously allocated to the Middle East has been redeployed to Europe, where shorter routes allow for higher aircraft utilization and more frequent operations.

The airline has already exited Abu Dhabi and reduced exposure to several underperforming airports. Management also indicated that London Gatwick is not a major growth priority due to high airport charges and operational constraints.

Another notable strategic decision is the abandonment of a standalone Airbus A321XLR operating model. Instead, all A321XLR aircraft will be integrated into the standard A321neo fleet, simplifying operations and reducing complexity.

Growth Outlook Remains Very Strong

Management's guidance for the first half of fiscal 2027 points to continued rapid expansion. Available seat capacity is expected to increase by approximately 25% in the first quarter and by more than 25% in the second quarter.

Additional support should come from the gradual restoration of Tel Aviv operations and the continued return of grounded aircraft. Management also sees a favorable competitive backdrop as airlines across Europe face rising fuel costs, liquidity constraints, and aging fleets.

CEO József Váradi openly suggested that the second half of the year could create "market vacuums" and even trigger airline failures, creating opportunities for Wizz Air to capture additional market share.

Analyst View

Overall, the results should be viewed positively. Wizz Air not only returned to profitability but also demonstrated strong cash generation and improved leverage metrics. More importantly, the gradual resolution of the Pratt & Whitney engine issue suggests that the primary obstacle limiting growth over the past two years is beginning to fade. If management delivers on its fleet recovery timeline, Wizz Air could enter 2027–2028 with one of the youngest and most cost-efficient fleets in Europe. Combined with aggressive capacity growth, a renewed focus on profitable core markets, and the potential to benefit from industry consolidation, the company appears well positioned to improve earnings and strengthen its competitive position over the medium term.

Source: xStation5

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.