Stoxx Europe 600 futures are rising more than 0.2%, with European equities extending positive momentum after record highs on Wall Street, fresh peaks across Asian markets, and a sharp decline in oil prices below $100 per barrel amid expectations of a potential agreement between the United States and Iran.

Eurozone retail sales declined by 0.1% month-over-month, compared to market expectations for a 0.3% decline; the previous reading stood at -0.2%. On an annual basis, retail sales increased by 1.2%, in line with consensus forecasts, although below the prior reading of 1.7%.

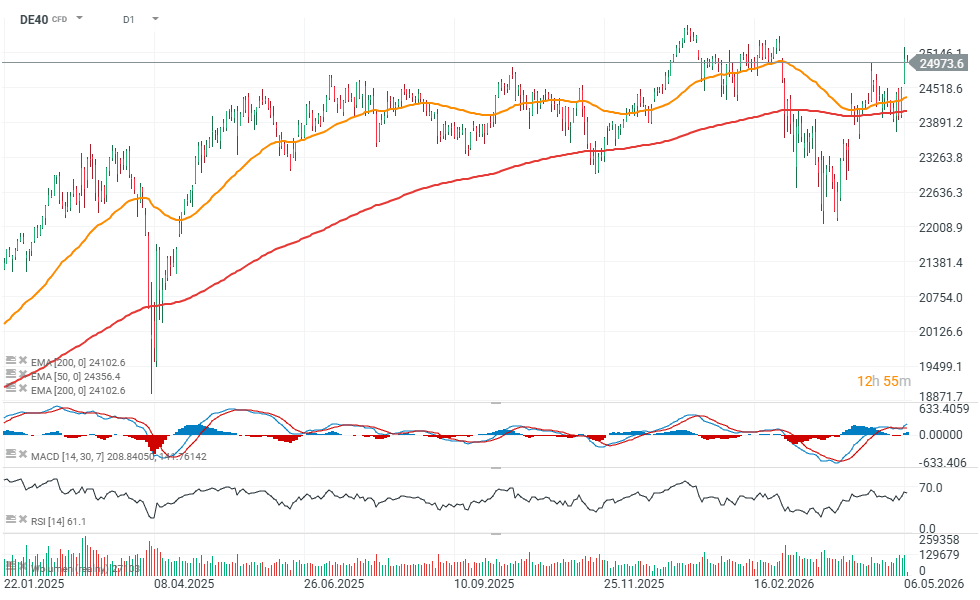

Global markets are also seeing a weaker US dollar and lower bond yields, supporting equities, precious metals, and Bitcoin. In Europe, Germany’s DAX is underperforming relative to the broader market, slipping around 0.1% despite the generally positive sentiment across the region.

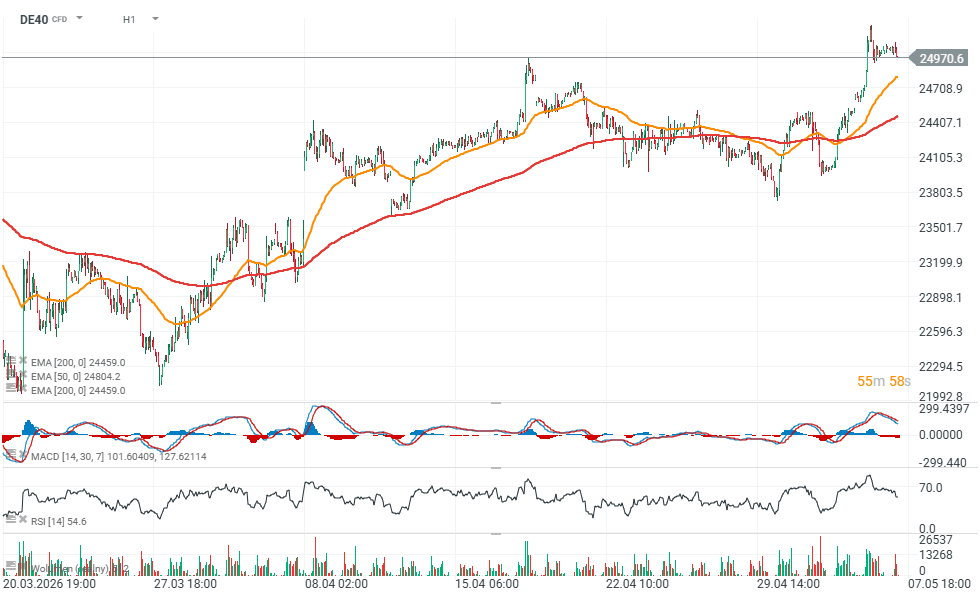

DAX (DE40) futures chart, D1 / H1 interval

Source: xStation5

Source: xStation5

Corporate earnings support sentiment across European markets

- Qiagen reported adjusted EPS of 54 cents, in line with analyst expectations.

- Lottomatica generated revenue of €600 million and stated that it expects 2026 adjusted EBITDA to come in at the upper end of previously issued guidance.

- Tenaris posted sales of $3.10 billion, beating market expectations of $2.99 billion.

- Endesa reported net profit of €725 million versus analyst estimates of €627.6 million.

- Jeronimo Martins posted EBITDA of €572 million, above consensus forecasts of €560.6 million.

- Banco Comercial Portugues reported net profit of €305.8 million, significantly above expectations of €283.4 million.

Elevated volatility across European equities following earnings releases

- Prosus gained around 3%, making it one of the strongest performers in the Stoxx Europe 600, while Henkel rose about 2% after reporting better-than-expected first-quarter organic sales growth.

- CSG NV advanced 1.7% and BE Semiconductor Industries climbed 1.6% amid continued optimism surrounding the semiconductor sector; STMicroelectronics also traded higher, gaining around 1.4%.

- Argenx rose 1.5% after reporting Vyvgart sales above analyst expectations.

- TUI and Lufthansa both added around 1%, supported by improving sentiment in the travel and airline sectors as oil prices declined.

- Prysmian gained 0.8% after comments suggesting an extended growth runway driven by data center investments and expansion in the US market.

- RENK Group fell around 1%, alongside BP, Novo Nordisk, Voestalpine, and Nokia, which were also under pressure ahead of the European open.

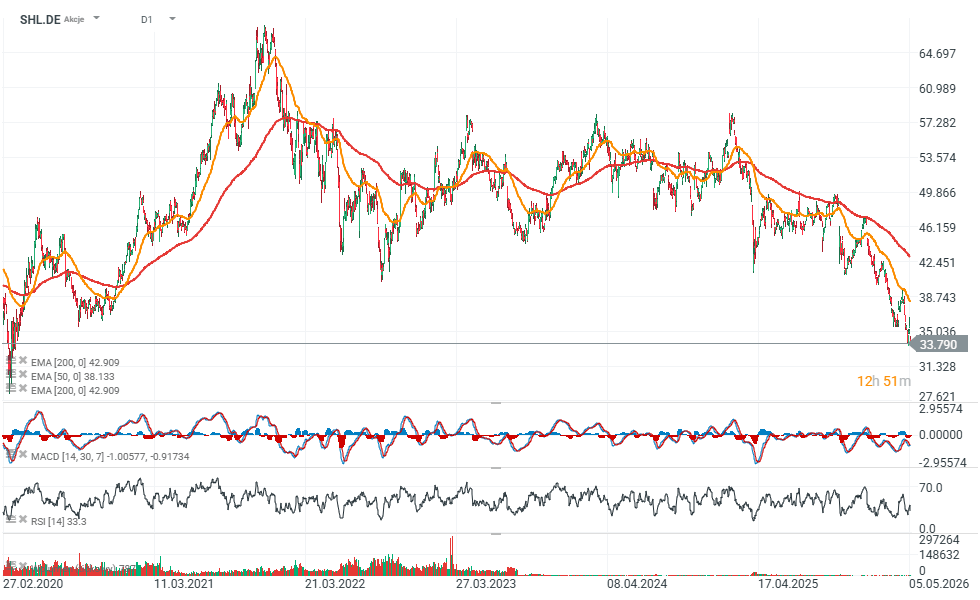

- Aumovio declined 1.7% despite reporting adjusted EBIT of €106 million versus expectations of €93 million, while Siemens Healthineers dropped nearly 5% after cutting its comparable sales growth outlook for the full fiscal year.

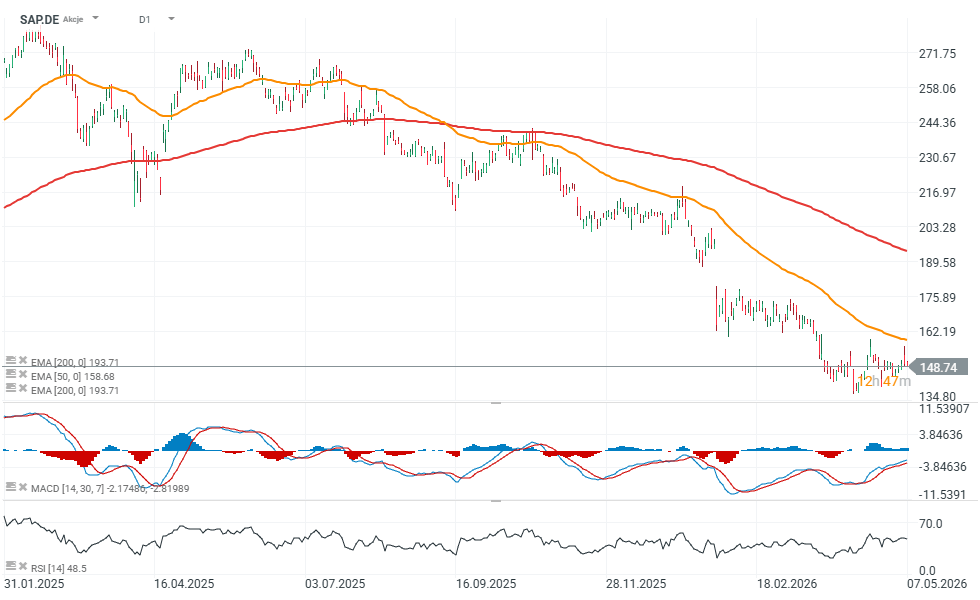

- SAP and OMV fell around 1.1%, while Andritz lost 1.3% following mixed earnings results.

SAP chart (D1 interval)

Source: xStation5

European companies continue to beat market expectations

- Flutter Entertainment reported revenue of $4.30 billion, above market expectations of $4.24 billion.

- AMS-Osram posted quarterly revenue of €796 million versus consensus estimates of €774.3 million.

- Aker BP reported pre-tax profit of $2.72 billion, significantly above forecasts of $1.89 billion.

- Avolta recorded organic revenue growth of 4.7%, exceeding analyst expectations of 4.55%.

- Sanoma posted second-quarter revenue of €221.1 million, above consensus estimates of €215 million.

- BNP Paribas Bank Polska reported net profit of PLN 375.3 million, well above expectations of PLN 306.5 million.

- Swiss Re delivered second-quarter net income of $1.51 billion versus forecasts of $1.19 billion.

- GN Store Nord maintained its full-year organic revenue growth guidance of 0–6% and EBITA margin guidance of 8–9%, compared to 7.6% achieved in 2025.

- Siemens Healthineers lowered its full-year comparable sales growth forecast to 4.5–5% from the previous 5–6% range, while the market had expected approximately 4.94%.

Siemens Healthineers stock chart (D1 interval)

Source: xStation5

- Nexi reported first-quarter revenue of €821.4 million versus expectations of €814.5 million.

- Lanxess reported first-quarter sales of €1.38 billion, compared to market expectations of €1.40 billion.

- Knorr-Bremse posted first-quarter EBIT of €245 million, slightly above consensus estimates of €244.8 million.

- Pharming reported quarterly revenue of $72.4 million; the market compared the result with $79.1 million achieved a year earlier.

- Vonovia reported adjusted first-quarter EBITDA of €711.6 million, above analyst expectations of €701.9 million.

- SAF-Holland posted adjusted first-quarter EBIT of €42.5 million, beating consensus forecasts of €41.6 million.

- Zealand Pharma reported a first-quarter net loss of DKK 43.94 million versus expected losses of DKK 68 million.

- Wacker Neuson posted first-quarter EBIT of €41.5 million, significantly above analyst expectations of €12.1 million.

- Solvay reported underlying first-quarter EBITA of €219 million versus market expectations of €228 million.

- Intrum reported adjusted first-quarter EBIT of SEK 50.1 million, well above expectations of SEK 17 million.

- FinecoBank posted first-quarter net profit of €162.2 million versus forecasts of €158 million.

- Veidekke reported quarterly revenue of NOK 965 million, above analyst expectations of NOK 895 million.

- Legrand reported organic revenue growth of 9.3%, significantly above market expectations of 6.81%.

- Davide Campari posted organic revenue growth of 2.9%, while analysts had expected a 5% decline; despite the strong results, cautious forward guidance triggered a sharp selloff in the stock.

Campari chart (D1 interval)

Source: xStation5

EU50 and OIL charts (D1 interval)

Source: xStation5

Source: xStation5

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.