European stock markets opened Monday under slight pressure—the Stoxx Europe 600 is down about 0.2%, and Euro Stoxx 50 futures are trading slightly lower amid geopolitical uncertainty in the Middle East.

The main factor driving market sentiment is the lack of progress in negotiations between the U.S. and Iran—over the weekend, there was an exchange of attacks, including an Iranian strike on a base in Kuwait and U.S. “defensive strikes” on Iranian radar installations, which has pushed back the prospect of a deal and the reopening of the Strait of Hormuz.

Geopolitical tensions are driving up oil prices—Brent crude jumped more than 3%, approaching $94 per barrel; in the foreign exchange market, the dollar remains relatively stable, with the DXY index hovering around 99, though the EUR/USD pair is down slightly, trading at 1.1645.

Weak macroeconomic data is adding to the pressure on market sentiment—the European manufacturing PMI fell to 51.6 in May from 52.2 in April, while production costs rose to their highest level in four years due to supply chain disruptions and high energy prices.

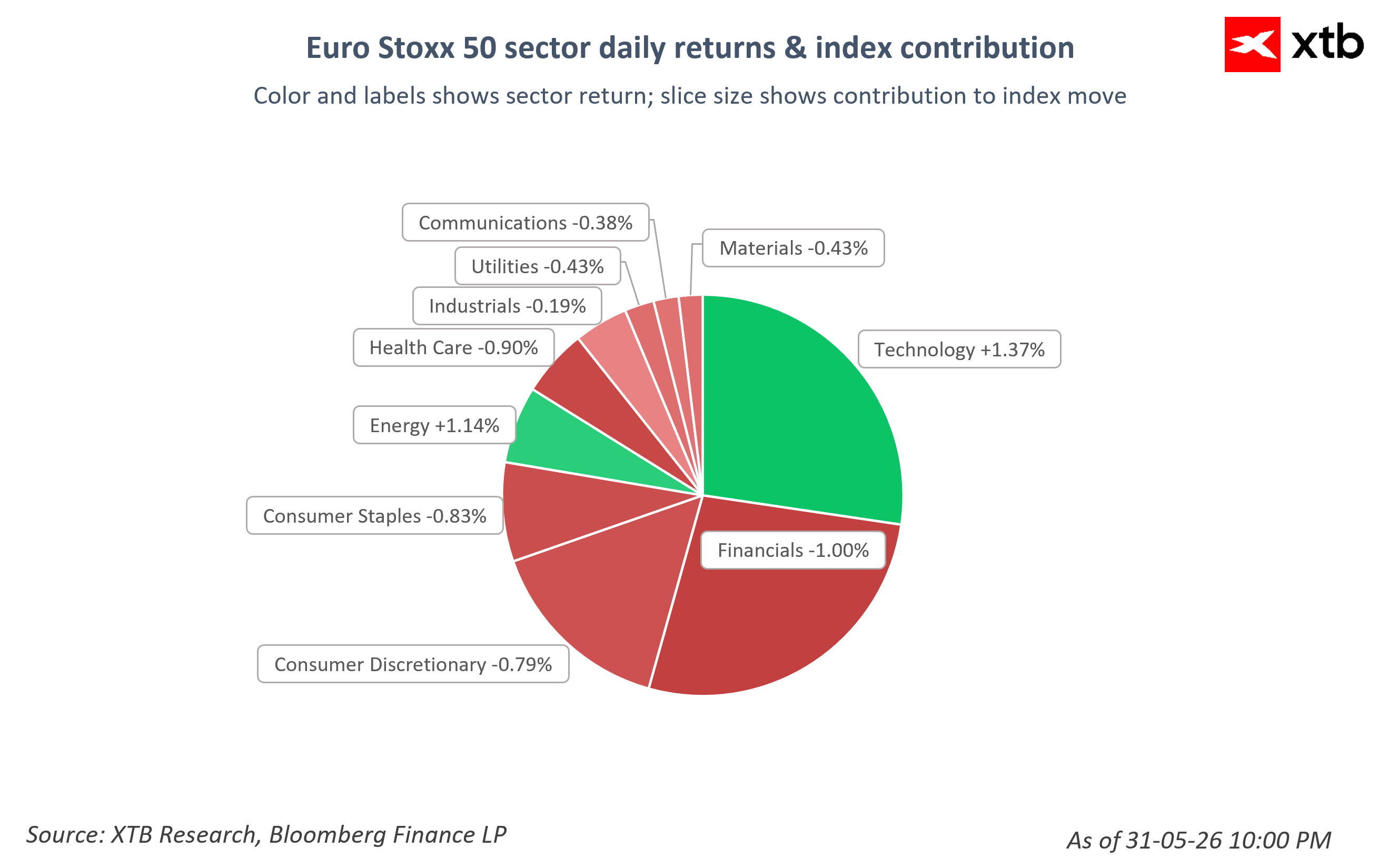

In terms of sector performance, technology (+1.37%) and energy (+1.14%) stand out positively as the only sectors posting gains—the technology sector is being driven by AI-related companies (SAP +5.6%, Infineon +2%), while the energy sector is being buoyed by a surge in oil prices.

On the other side of the spectrum, the worst performers are the financial sector (-1.00%) and healthcare (-0.90%); discretionary consumer goods (-0.79%) and staples (-0.83%) are also under pressure.

Company Information

-

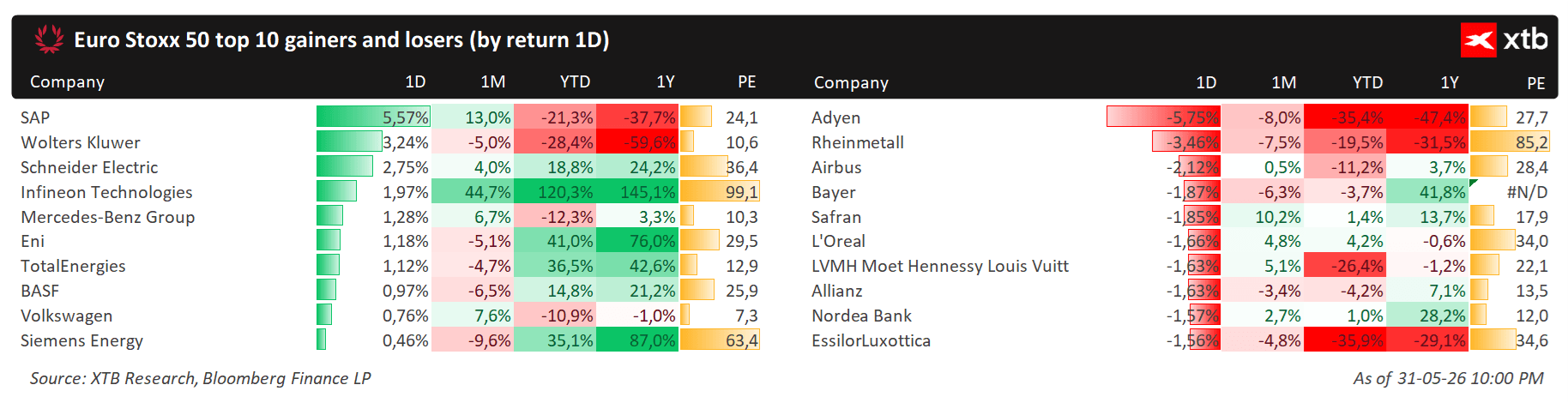

EasyJet rose by more than 10% after private equity firm Castlelake revealed it was considering a takeover of the British carrier—Castlelake holds approximately 2.14% of EasyJet’s shares, and any potential offer would have to be at least 403.23 pence per share; EasyJet’s management has not yet entered into talks and described the approach as “highly opportunistic.”

-

Barclays analysts (PT 480p) note that EasyJet’s share price has already fallen 22% year-to-date—the largest decline among the European airlines they cover—and the SOTP model shows the largest discount to net asset value among the carriers they cover; Oddo BHF notes that Castlelake’s interest signals a broader undervaluation of the entire European airline sector.

-

SAP is today’s top gainer on the Euro Stoxx 50 (+5.6%), driven by AI sentiment following comments from Jensen Huang (Nvidia) dismissing concerns about issues with large cloud platform models, as well as a broad rebound across the software sector; despite the gains, the company is still trading 21% below its levels from the start of the year.

-

Wise plummeted by about 15% after the Bureau of Investigative Journalism revealed that Belgian prosecutors had launched an investigation into the company regarding suspicious transactions worth half a billion euros linked to money laundering.

-

Universal Music Group is down about 2.9% after its board rejected an unexpected takeover bid from Bill Ackman’s Pershing Square fund, deeming it inadequate relative to the company’s value.

-

Rheinmetall is down 3.5% following the defense sector’s strong rally in recent weeks—investors are taking profits, especially since a potential U.S.-Iran agreement would reduce the war premium built into defense sector valuations.

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.