The oil market remains at the center of investor attention as markets prepare for the upcoming week across global equities. The US session will not take place today due to Easter holidays, while European markets also remain closed. Sentiment in Wall Street index futures is mixed.

- Asian equities ended the week higher despite ongoing elevated market volatility. Sentiment improved following reports suggesting that more trade may soon resume through the Strait of Hormuz.

- Thursday’s rebound in Asia followed improved sentiment on Wall Street, supported by news that Iran is working with Oman on an agreement to oversee commerce along the strategic shipping route, which has been largely blocked since the start of the conflict.

- Trading in the region remained limited, however, as many key Asian markets were closed for holidays. Major European exchanges were also shut.

- US Treasury futures in Asia traded close to flat levels, while the cash market remained closed until the US session. Meanwhile, the US dollar showed mixed performance against G10 currencies.

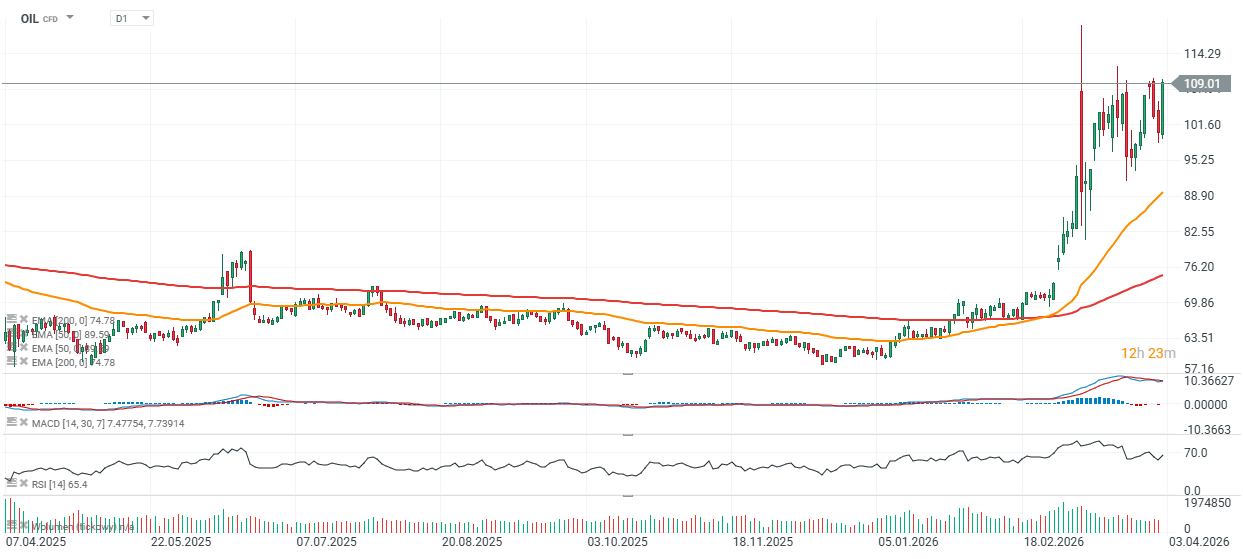

- The oil market remains under strong geopolitical pressure. Prices surged above $110 per barrel after Donald Trump issued new threats against Iranian infrastructure, aiming to increase pressure on Tehran during negotiations.

- WTI crude rose by 11%, while the global Brent benchmark settled near $109 per barrel, as shown in the chart below.

- Iran carried out additional attacks overnight and into Friday morning targeting sites in Gulf states, further sustaining tensions around the security of energy transport and maritime trade.

- A container ship signaling French ownership passed through the Strait of Hormuz, likely marking the first recorded transit by a Western Europe-linked vessel since the Iran conflict effectively disrupted this key route.

US index futures are slightly lower, with S&P 500 contracts down around 0.3%.

US macro data:

- Nonfarm Payrolls (March): +178K (forecast: 65K, previous: -92K)

- Average Earnings (YoY): 3.5% (forecast: 3.7%, previous: 3.8%)

- Average Earnings (MoM): 0.2% (forecast: 0.3%, previous: 0.4%)

- Government Payrolls: -8K (previous: -6K)

- Private Payrolls: +186K (forecast: 78K, previous: -86K)

- Manufacturing Payrolls: +15K (forecast: -5K, previous: -12K)

- Labor Force Participation Rate: 61.9% (forecast: 62%, previous: 62.0%)

- Unemployment Rate: 4.3% (forecast: 4.4%, previous: 4.4%)

- Average Weekly Hours: 34.2 (forecast: 34.3, previous: 34.3)

Revisions: January payrolls were revised up by 34K (from +126K to +160K), while February was revised down by 41K. In the initial reaction, Nasdaq 100 futures are gaining, with concerns about a US economic slowdown easing. However, the strong labor market data may also reinforce expectations that the Fed will remain cautious about rate cuts. The full market reaction may only become clear after US markets reopen next week. The report also showed that the number of discouraged workers rose sharply in March by 144K to 510K.

OIL (D1 timeframe)

Source: xStation5

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

The coffee market in the grip of weather and empty warehouses: The paradox of record Brazil harvests

Chart of the Day: Who suffers from the oil price drop? (28.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.