GEOPOLITICS AND THE MIDDLE EAST

• Iran has put forward a three-phase peace proposal, separating the issue of the Strait of Hormuz from the nuclear negotiations. Tehran proposes first opening the strait and lifting the naval blockade, with talks on the nuclear program to take place at a later stage. The proposal was conveyed to the White House through Pakistani mediators.

• Trump rejects the logic behind Iran’s proposal and intends to maintain the naval blockade as his primary leverage. In an interview with Fox News, he warned that Iran’s oil infrastructure could “collapse within days,” and that the damage would be “lasting and irreversible.” At the same time, he signaled his willingness to hold telephone talks with Iran.

• Trump canceled the planned trip by envoys Witkoff and Kushner to Islamabad, deeming it a waste of time given the lack of progress. “No one knows who’s in charge, including themselves. We hold all the cards; they hold none!” he wrote on Truth Social. The Iranian Foreign Ministry confirmed that no meetings with Washington are planned.

• Iranian Foreign Minister Araghchi is engaged in an intensive diplomatic marathon. Following his visit to Pakistan, he traveled to Oman, where he met with Sultan Haitham ibn Tariq—they discussed safe transit through the Strait of Hormuz and presented a “feasible framework” for a lasting resolution to the conflict. Iran and Oman agreed to continue consultations. On Monday, Araghchi is scheduled to fly to Moscow for a meeting with President Putin.

• The ceasefire between Israel and Lebanon has collapsed—both sides are exchanging rocket attacks, which is worsening the regional security situation. The three-week extension of the truce announced by Trump last week proved to be short-lived. Hezbollah is actively undermining the ceasefire.

• Reports of an attack on a cargo ship south of the Bab al-Mandab Strait are raising concerns that a second front in the conflict with Iran may be opening up. Disruptions to shipping could spread far beyond the Strait of Hormuz, affecting another key trade route.

ECONOMY AND MACROECONOMIC DATA

• Chinese industrial profits rose 15.8% year-over-year in March—the fastest pace since September 2025. For the first quarter as a whole, profits rose 15.5% year-over-year (vs. 15.2% previously). The driving force is the AI boom – chip imports rose 54% y/y in March alone, with total exports up 15% y/y in Q1. The data suggests that Chinese industry is weathering the energy shock better than expected, though weak domestic consumption remains a structural risk.

• China may see its first quarter since 2021 in which imports exceed exports—due to a sharp rise in AI chip imports. Producer prices have begun to stabilize after years of deflationary pressure, allowing companies to rebuild their margins. A diversified energy mix and strategic oil reserves provide China with some cushion against a shock from the Strait of Hormuz.

• A crucial week lies ahead for central banks: the Fed’s decision on Wednesday (potentially Powell’s last meeting as chair—the Department of Justice has dropped its criminal investigation, clearing the way for Warsh’s confirmation), the ECB and BoE on Thursday (expected to keep rates steady while leaving the door open for hikes), as well as the BoJ and BoC. Data: US PCE, GDP, and ISM Manufacturing PMI.

• India has signed a free trade agreement with New Zealand as part of Prime Minister Modi’s global FTA strategy.

STOCK MARKETS – WALL STREET, EUROPE, AND ASIA

• The S&P 500 and Nasdaq Composite closed last week at new all-time highs. April is shaping up to be a strong month of recovery—the S&P 500 is up over 9% month-over-month, the Nasdaq over 15%, and the Dow over 6%. The rally continues despite tensions in the Middle East and concerns about AI spending.

• Futures fell by about 0.3% at the open following the cancellation of Witkoff’s mission to Islamabad and the continuation of the blockade—gold rose, stocks fell in a classic risk-off move. Sentiment reversed after Axios published Iran’s peace proposal – S&P 500 futures returned to positive territory (+0.02%), Nasdaq 100 futures +0.17%. The market shifted into “buy the dip” mode.

• European markets are expected to open slightly higher – DAX +0.3%, CAC 40 +0.2%, FTSE MIB +0.26%, FTSE 100 unchanged (IG data). Sentiment is buoyed by hopes for a diplomatic breakthrough despite the ongoing stalemate. Deutsche Börse is set to report earnings, and GfK consumer confidence data from Germany will be released.

• The Nikkei 225 rose 1.24%, standing out against the backdrop of mixed Asian markets. The Hang Seng (CHN.cash) fell 0.34%.

CURRENCIES

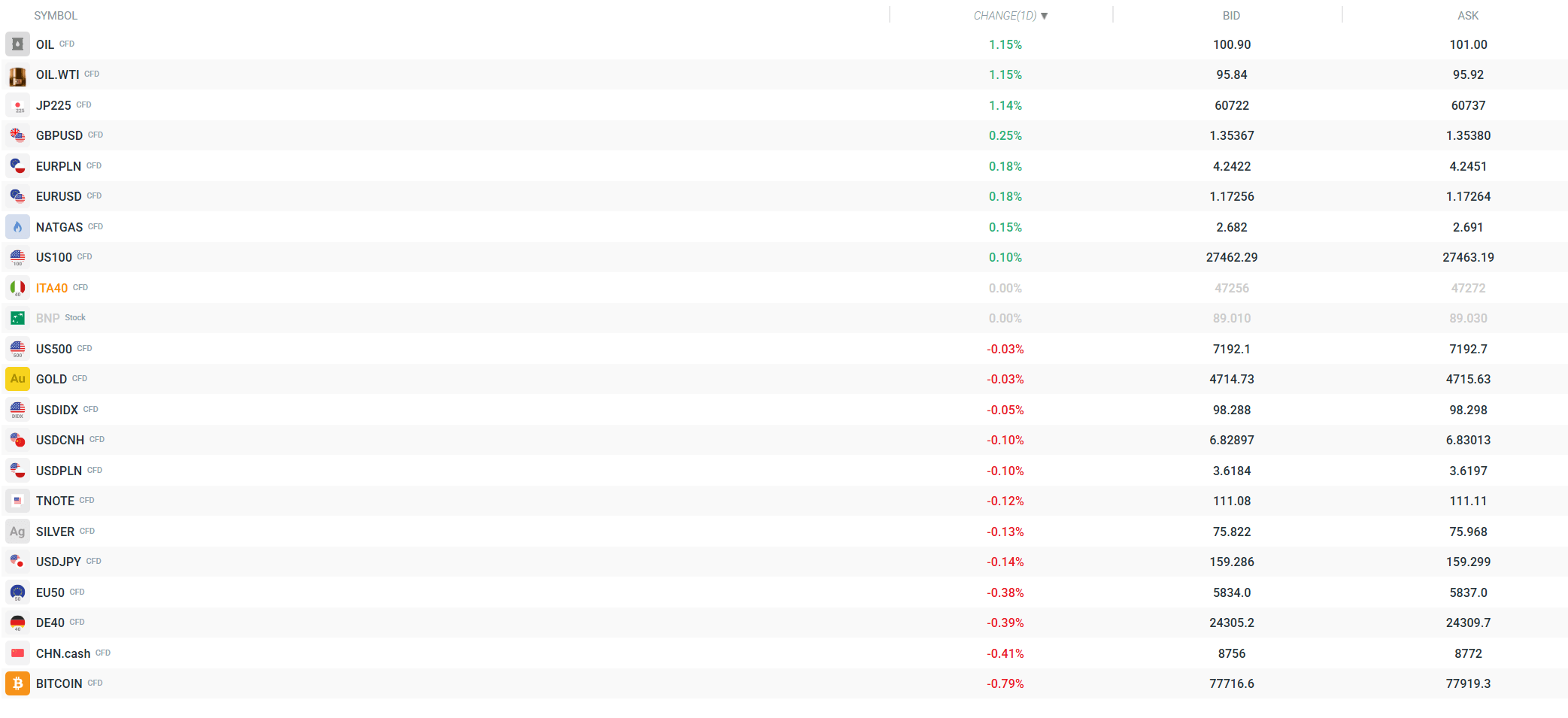

• The dollar opened the Asian session stronger, but reversed course during the day and weakened significantly. The currency strength index shows the USD as the weakest major currency of the day, while the AUD and NZD are the strongest. The USDIDX is down 0.05% to around 98.3.

• USDJPY fell to 159.27 (-0.15%) – the yen is strengthening ahead of this week’s BoJ decision (the market is on a knife’s edge – rates are expected to remain unchanged, but there are hawkish signals regarding June). EURUSD gains 0.18% to 1.1725, GBPUSD rises 0.24% to 1.3537 – the pound is at its strongest in weeks.

COMMODITIES

• Oil started the week with gains, but those gains were partially erased following the release of Iran’s proposal to reopen the Strait of Hormuz. Brent is up 1.28% to ~$101, while WTI is up 1.21% to ~$95.90. WTI retreated from its daily high of $96.68 to around $95.35 in response to diplomatic reports. A potential opening of the Strait of Hormuz without a resolution to the nuclear issue could trigger a sharp correction in oil prices.

• Gold is virtually unchanged (+0.01%) at ~$4,717 per ounce—it gave up earlier gains following an improvement in market sentiment. Silver is up 0.21%. Natural gas (NATGAS) is up 0.11%.

COMPANIES

• "Magnificent Seven" Earnings Week – Five of the seven largest tech companies are reporting in the last week of April. This is a crucial test for the market – the S&P 500 and Nasdaq remain at historic highs, and the semiconductor sector (SOXX) recorded 17 consecutive sessions of gains last week.

CRYPTOCURRENCIES

• Bitcoin is down 0.41%, trading around $78,000. Saturday’s crypto summit at Mar-a-Lago featuring Trump (for the 297 largest holders of the $TRUMP meme coin) failed to generate a sustained upward momentum. Cryptocurrencies remain under pressure from broader risk-off sentiment at the start of the week, though sentiment improved following the release of Iran’s peace proposal.

WHAT TO EXPECT FROM TODAY'S SESSION

• Trump is convening a Situation Room meeting with his top national security advisors to assess the stalemate in negotiations with Iran and consider next steps. Any news coming out of this meeting could send shockwaves through the markets—particularly oil and futures contracts.

• Iran’s peace proposal is the main catalyst of the day—markets are reacting positively, but Trump has made it clear that he does not intend to lift sanctions until Iran makes nuclear concessions. The White House has stated that it “will not negotiate through the press” and will accept only an agreement that permanently prevents Iran from obtaining nuclear weapons. The stalemate continues.

• A key week for macroeconomic and corporate news: the Fed (Wednesday – Powell’s final meeting?), the ECB and the BoE (Thursday), the BoJ, and the BoC. Data: US PCE, GDP, ISM Manufacturing PMI. Five companies from the “Mag 7” are reporting earnings – any disappointment at current valuations could trigger a sharp correction from historic highs.

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

Silver breaks above $59 and attracts capital again. Gold remains in the shadow of its younger sibling

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.