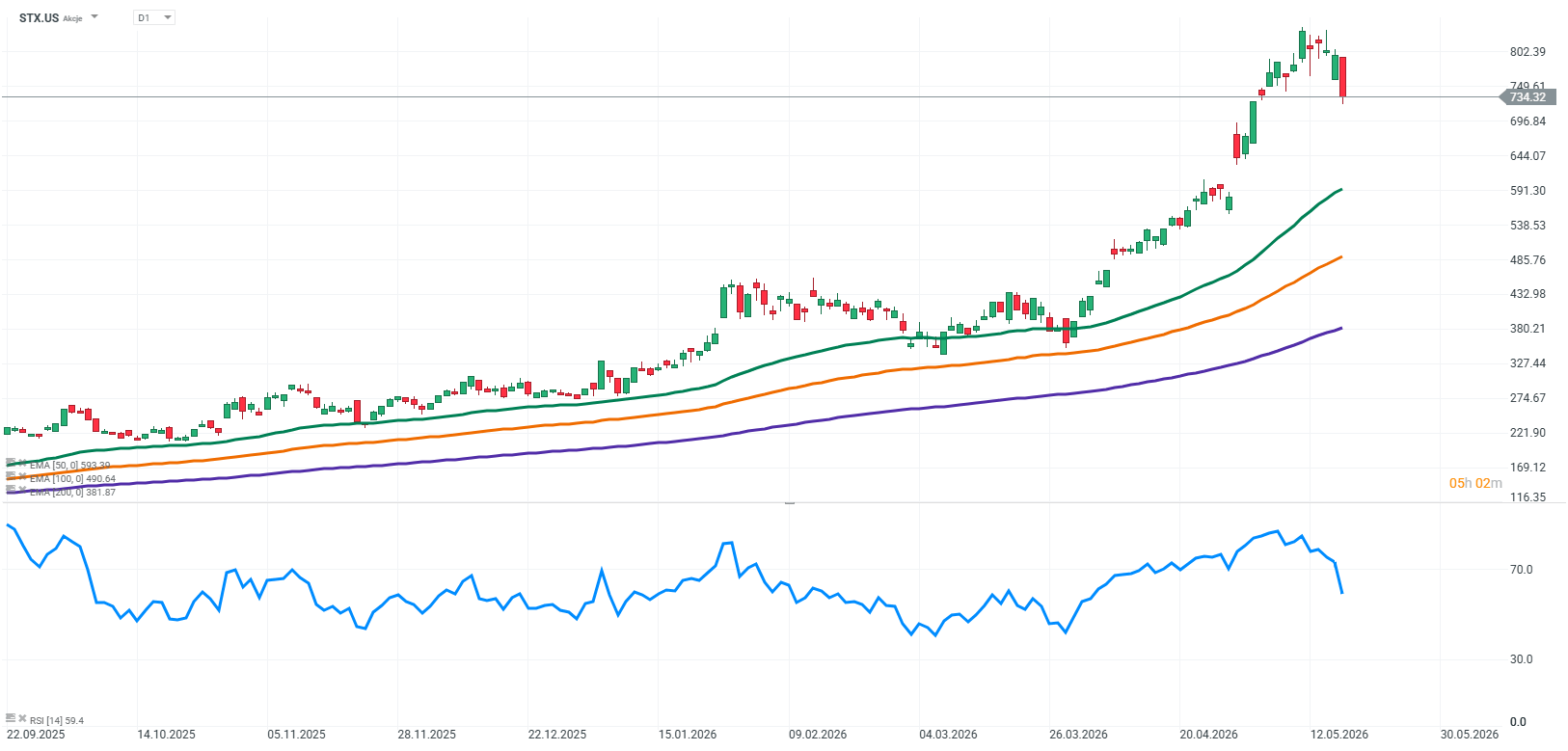

Seagate Technology is a U.S.-based technology company primarily engaged in the production of hard disk drives (HDDs) and data storage solutions, commonly referred to as storage. In this context, storage refers to the infrastructure and devices used for the long-term recording and retention of massive volumes of digital data. In practice, this includes systems that store data generated by applications, cloud platforms, AI systems, streaming services, and enterprise databases, all of which must remain accessible, secure, and scalable. Seagate mainly supplies data center operators and large cloud providers, making the company directly exposed to the global growth in data volumes and the expansion of artificial intelligence.

Today’s decline in Seagate shares fits into broader weakness across the semiconductor sector and companies tied to data infrastructure. The selling pressure was driven by management commentary highlighting long lead times and a cautious approach to expanding production capacity. The CEO suggested that building new factories under current technological and cyclical conditions would take too long to effectively meet near-term demand, which the market interpreted as a signal of limited aggressive supply expansion. In practical terms, despite very strong demand from data centers, Seagate does not plan to rapidly scale up output, which investors interpret in two ways: on one hand as supportive for pricing and margins, but on the other as a constraint on revenue growth potential.

Additionally, previous industry data indicates that production capacity in the data center HDD segment is already tightly constrained and largely allocated for upcoming quarters, which theoretically supports pricing levels but limits the ability to scale the business quickly. At the same time, the AI supercycle narrative remains in place, where rising demand for data storage has been viewed as a key growth driver for companies like Seagate. However, it is important to remember that markets tend to be forward-looking and often aggressively price in future expectations, meaning that even neutral or cautious management commentary can be received negatively when it conflicts with an already elevated growth narrative.

It is also worth emphasizing that the hard drive and storage industry is historically highly cyclical and prone to sharp shifts in sentiment. In such an environment, key customers, primarily hyperscalers, can dynamically adjust their order pace depending on their capital expenditure budgets and evolving priorities in AI infrastructure. As a result, the market remains highly sensitive to any signals regarding CAPEX trends and future data center expansion plans. The current price action in Seagate and across the semiconductor space can therefore be interpreted more as a reflection of profit-taking and reduced exposure after a strong rally, rather than a deterioration in underlying fundamentals.

Source: xStation5

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.