Netflix (NFLX.US) will report its Q1 2026 results after the market close on April 16. The company enters the release with strong share price momentum and elevated investor expectations, meaning that merely meeting consensus may not be enough to sustain the rally. The key question is not only whether Netflix delivers on revenue and earnings per share, but whether it can confirm the durability of its two core growth engines: subscriptions and advertising.

Wall Street expects revenue of approximately $12.16–12.20 billion, implying around 15% year-over-year growth. Consensus EPS stands at roughly $0.76–0.78. The market is therefore pricing in a solid quarter, and with the stock already up more than 18% year-to-date, the focus shifts from simply “beating estimates” to the quality of growth and the outlook for the coming quarters.

Netflix Q1 2026 earnings: market looking for confirmation of growth durability

Netflix will release its Q1 2026 results after the close on April 16. The company enters the report with strong market momentum, with shares rising significantly year-to-date. Additional support for sentiment came from the company’s decision to walk away from a planned transaction involving Warner Bros. Discovery, which resulted in a $2.8 billion termination fee. However, for investors, the one-off effect is less important than whether Netflix can confirm the sustainability of its growth model in an environment of higher pricing, increasing reliance on advertising, and elevated full-year expectations.

Consensus points to a solid quarter, but expectations are high

Wall Street expects revenue in the range of $12.16–12.20 billion, representing roughly 15% year-over-year growth. Consensus EPS is estimated at $0.76–0.78. This setup suggests the market is already anticipating a strong quarter, meaning that simply meeting expectations may not be sufficient to drive a positive share price reaction. The focus will be on growth quality, monetization structure, and management commentary on upcoming quarters. Analyst sentiment also remains constructive, with the majority of recommendations still positive and price targets from major brokerages above current trading levels.

Subscriber growth after price hikes will be the first major test

The most important area of the report will be the pace of paid subscriber growth following recent price increases. Netflix has successfully combined scale expansion with improved monetization in recent quarters, but the market now wants to see whether this model remains resilient after the March pricing changes. Commentary on churn and the regional distribution of growth will be particularly important. Investors will look for confirmation that international markets—especially Asia and other high-growth regions—continue to offset the more mature U.S. market. If the company demonstrates resilience in its user base despite higher prices, it would support the narrative of continued revenue expansion.

Advertising is becoming the second growth pillar

The second key focus will be the development of the advertising segment. For the market, advertising is no longer a secondary feature of the subscription model but is increasingly viewed as a second core pillar. Investors will assess not only the growth rate of advertising revenue, but also the adoption of the ad-supported tier and its impact on ARPU and the overall customer mix. If management shows that advertising is scaling without materially weakening the quality of subscription revenues, this could support further valuation expansion. Conversely, weaker commentary on advertising could raise concerns that current expectations are too optimistic.

In this context, investors will also monitor the expansion of live content, which may enhance the attractiveness of Netflix’s advertising offering. During the quarter, the company expanded its live programming, including streaming a BTS concert from Seoul and the 2026 World Baseball Classic. The market will evaluate whether such content can support further advertising revenue growth and strengthen Netflix’s positioning with advertisers.

Margins and cost discipline remain central to the investment case

The third area of focus will be operating profitability and cost control. Netflix guided for an operating margin of around 32% for the quarter, and investors will assess whether the company can maintain cost discipline while continuing to fund a high level of content investment. This is critical, as the current investment thesis is no longer based solely on scale growth, but on the company’s ability to translate that scale into higher cash flow and more predictable profitability. A margin beat could reinforce positive sentiment, while signs of cost pressure would likely weigh on the stock.

It will also be important whether management signals a continued balance between content investment and profitability. The company has previously indicated that content and advertising will be the main drivers of growth, and the market will evaluate whether this strategy continues to support financial performance without significantly increasing cost pressure.

Full-year guidance may matter more than the quarter itself

Ultimately, the most important element of the report may not be the first-quarter results themselves, but management’s commentary on full-year 2026 guidance. Consensus currently assumes revenue growth in the range of 12–14% for the year, and the market will be highly sensitive to any indication of an upward revision. Given the strong share price performance and elevated expectations, it is likely that forward guidance—rather than the quarterly figures—will drive the post-earnings reaction. A failure to raise guidance, even with solid Q1 results, could trigger profit-taking.

The market is looking for confirmation, not just solid numbers

From a market perspective, this is a high-stakes report. Netflix needs to demonstrate not just growth, but that growth remains durable after price increases, that advertising is scaling as expected, and that there is room to improve full-year expectations. If these elements are confirmed, the company may maintain its leadership within the media sector. If not, the high bar set by current expectations could quickly weigh on the stock.

In practical terms, this report will test whether Netflix can simultaneously raise prices, expand its paying subscriber base, scale advertising, and sustain strong profitability. At current valuation levels and after a strong run in the share price, investors are no longer looking for a solid quarter alone. They are looking for confirmation that further growth is achievable and that the existing valuation premium remains justified.

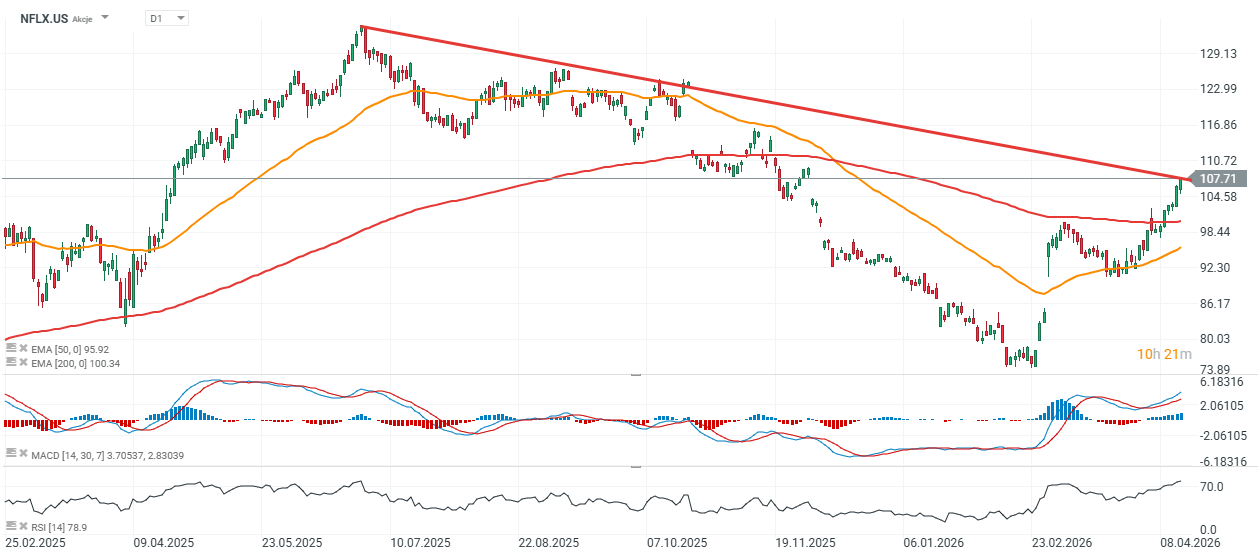

Netflix stock technical setup

Netflix shares are trading around 10% above the 200-day moving average (EMA200), which may act as a key support level in a downside scenario. The stock has recently approached resistance near $108. A breakout above this level could signal an acceleration of the uptrend, while a move below $100 would suggest weakening medium-term momentum.

Source: xStation5

Mercedes earninigs: Is optimism justified?

ASML sell-out: Dreams and rumors will not break the monopoly

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.