The world’s largest publicly traded company will report its results on Wednesday after the close of trading in the U.S. What are expectations, and what do they say about where markets stand?

A phenomenon observed repeatedly during earnings season has been the market’s anticipation of Nvidia’s results, which, simplified but broadly accurately, serve as a barometer of the strength of valuation expansion driven by the AI wave. This time is no different. However, the market is beginning to doubt not so much the investment thesis itself, but is bending under the pressure of the macroeconomic backdrop.

The massive CAPEX outlays that are a necessary condition for delivering the profits investors expect are now being questioned in light of rising bond yields.

Expectations for the results are conservative by the standards investors and technology leaders have grown accustomed to.

- Revenue is expected to be around $78.8 billion for Q1 2026, representing approximately 78% YoY growth.

- EPS is expected to come in at about $1.75, implying 127% YoY growth.

- This is expected to translate into an operating margin of 75% and a net margin of 55%.

It’s also likely that more important than headline revenue will be the growth rates of individual segments.

- While the compute segment (about 80% of revenue) is expected to grow "only" 78%, the networking segment is expected to grow by more than 150%.

Chance of Success

Despite the complexity of the financial and technical issues involved in investing in AI or semiconductor companies, and despite the many uncertainties around the quality and durability of growth in this sector, Nvidia is an unusually predictable player within it.

More than half of Nvidia’s revenue comes from just five companies: Microsoft, Amazon, SMC, Meta and Google, with Microsoft and Amazon alone accounting for 36% of revenue. In a typical market context, this would be a significant risk, but in Nvidia’s specific case it works in its favor. All of these companies continue to raise their CAPEX budgets, which they allocate largely to purchases from Nvidia. As long as their CAPEX continues to rise, Nvidia’s revenue should rise as well.

Is the Peak Behind Us?

While one should not expect Nvidia’s profits to decline in the near future - or even the growth rate of those profits - many figures suggest the company’s best period may already be behind it. Why?

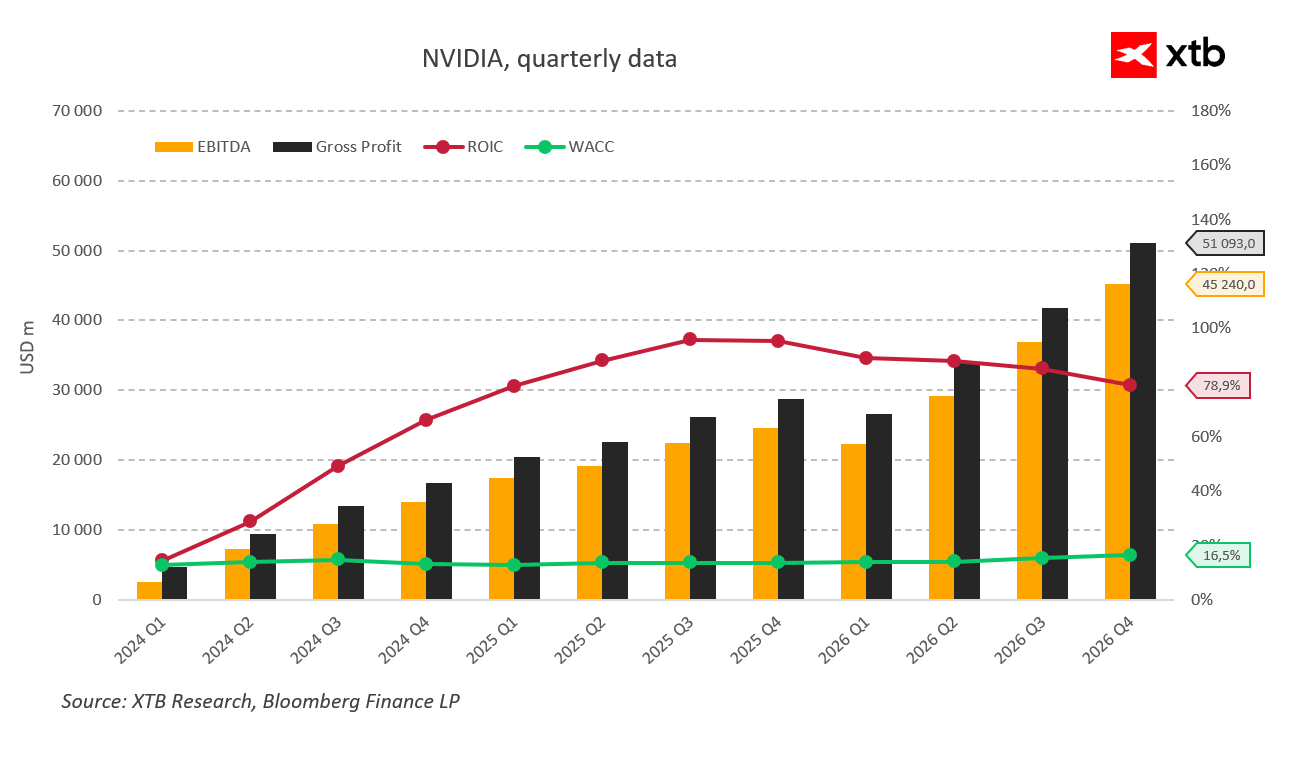

The key signposts are ROIC and WACC.

- Return on invested capital (ROIC) peaked in mid-2024 (fiscal Q3 2025) at 95%. Since then, it has been steadily declining to 78.9%. That is still an impressive level, but it is a clear signal that the segment Nvidia operates in has likely passed its most dynamic growth phase - even if it remains highly profitable versus the broader market.

- Financing conditions also matter. The weighted average cost of capital (WACC) rose over the last four quarters from 13.8% to 16.5%. This happened despite falling interest rates. It clearly indicates that excess liquidity in the market is fading. Nvidia itself is not under the same direct CAPEX financing pressure as hyperscalers are, but those hyperscalers are its main customers. Pressure on CAPEX is pressure on Nvidia’s results. A further rise in WACC could signal growing pessimism among lenders and investors, and the larger that increase, the greater that pessimism.

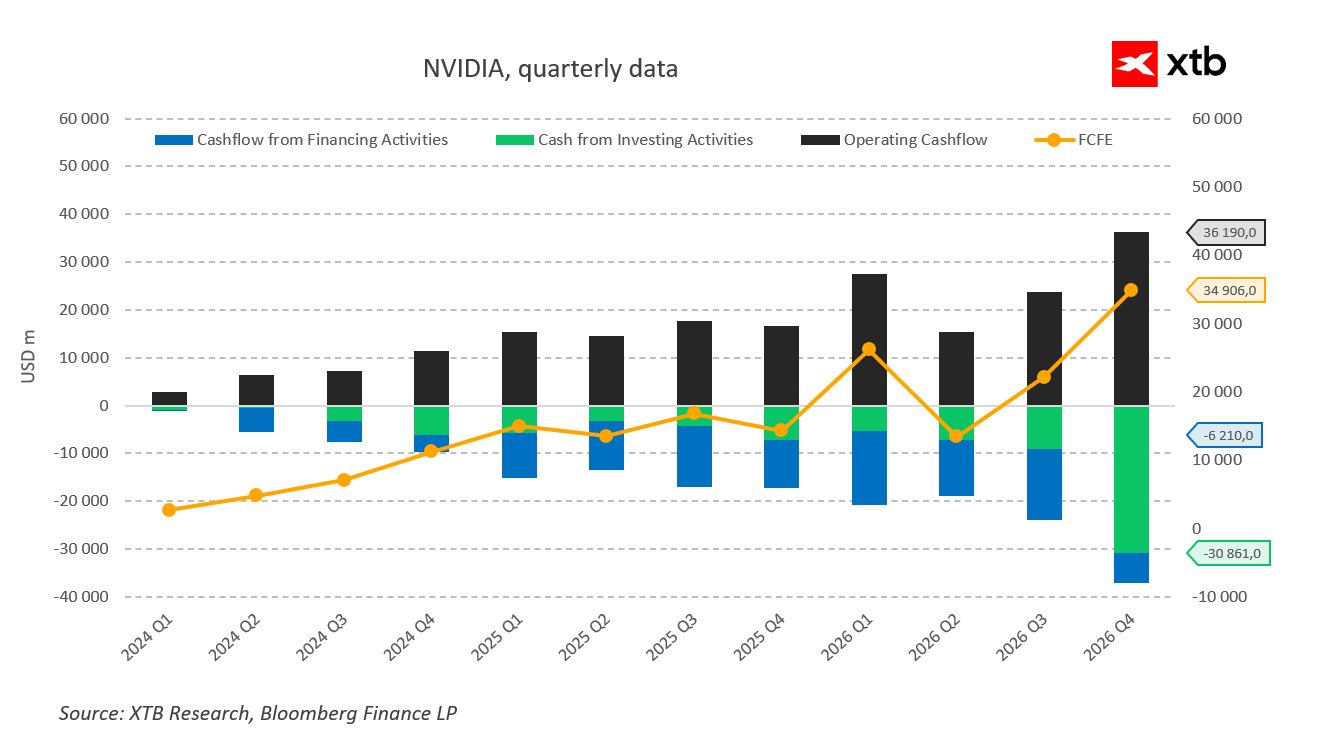

- But why would a company earning $42 billion in net profit quarterly need additional financing at all? Because to justify its valuation, it must simultaneously maintain its share buyback program while investing more and more.

- Negative cash flows in the “Other” investing category increased from $3.6 billion at the start of last year to $16.4 billion in the previous quarter - an increase of 450%.

- At the same time, share repurchases slowed from $13.7 billion to $3.8 billion. This is a clear sign of shifting priorities - from rewarding shareholders to investing. Investments that are becoming less and less profitable.

Conclusion

Historically, Nvidia’s growth remains phenomenal, and the company is still extremely profitable. Significant declines or disappointments in upcoming earnings calls should not be expected, although they are not impossible. However, regardless of delivered results and beats versus consensus, cracks are appearing in the background—cracks the market will likely ignore until the last moment. At the same time, earnings growth alone will not be enough to meaningfully lift already high valuations; optimistic guidance and new growth channels would be required - something for which there is currently no evidence.

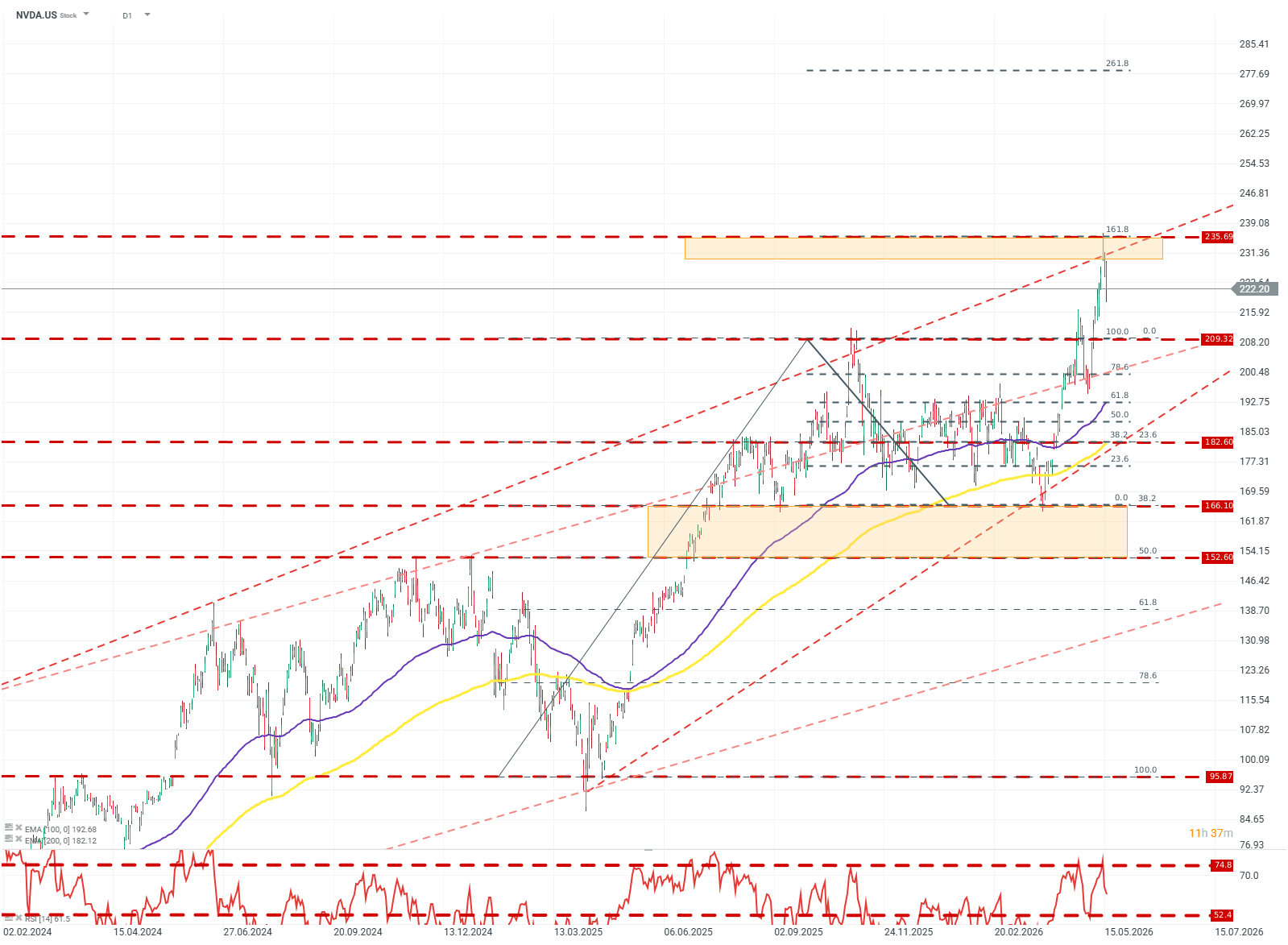

NVDA.US (D1)

The price broke out of a broad consolidation channel between $209 and $156, moving at the same time above the upper boundary of the 2024 uptrend line. After the breakout, the stock rapidly lost momentum after RSI crossed 74 and price reached resistance at the 161.8 Fibonacci level. At present, based on reactions at Fibonacci levels and the structure of moving averages, the base case would be consolidation in the $209–$235 range, with the potential for an upside break and a move toward the 261.8 Fibonacci level. Source: xStation5

Daily Summary - Oil gains due to uncertainty, market awaits inflation data

Bitcoin Near $64000 as ETF Inflows Return

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.