Summary:

- Price growth in the third quarter slowed down, though a deceleration was a touch smaller than expected

- Core prices keep hovering slightly below the midpoint of the RBNZ’s target

- RBNZ’s Bascand signals more rate cuts could be needed

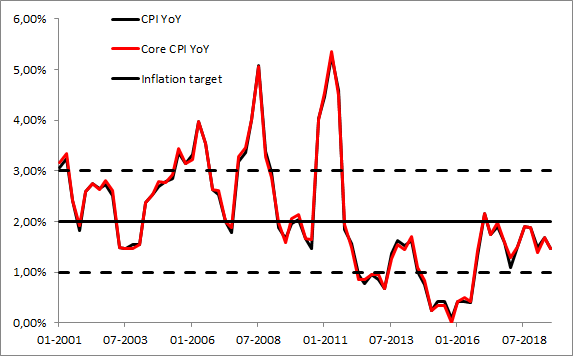

New Zealand’s inflation kept losing momentum during the third quarter slowing to 1.5% from 1.7% in annual terms, the result turned out to be a bit better than expected though as the consensus had called for a 1.4% YoYo pick-up. In quarterly terms, price growth remained unchanged at 0.6%. Although the outcome proved to be stronger than the RBNZ predicted in August (1.5% vs. 1.3% expected by the central bank), it does not mean any rapid change in monetary policy there. Moreover, the NZ economy could even require more monetary accommodation going forward, as a RBNZ’s member Bascand said on Wednesday. Let us recall that the RBNZ does not expect to reach its inflation target until late 2021, as per August forecasts. Other details showed that tradable price fell 0.7% from a year earlier mainly due to cheaper fuel, while non-tradable prices increased 3.2% in annual terms, reaching its highest pace since 2011. Taking into account a current stance of the NZ central bank it is hard to envisage any more sustained rally in the NZ dollar in the foreseeable future.

Price growth in New Zealand remains lacklustre suggesting the currency may not already be out of the woods. Source: Macrobond, XTB

Price growth in New Zealand remains lacklustre suggesting the currency may not already be out of the woods. Source: Macrobond, XTB

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

Euro Area core inflation above estiamtes! EURUSD under key resistance!

BREAKING: US GDP below estimates! EURUSD struggles for direction!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.