Brent crude futures continued to decline on Thursday, approaching the $70 per barrel level and erasing virtually all of the gains triggered by the conflict between the United States and Iran. Investors are increasingly pricing in a lower risk of prolonged supply disruptions, with attention shifting back to market fundamentals, including U.S.-Iran negotiations, the upcoming OPEC+ meeting, and the outlook for global oil demand. Another factor helping calm the market is the gradual normalization of tanker traffic through the Strait of Hormuz, one of the world's most critical energy shipping routes.

Market prices in de-escalation

Brent crude fell to around $70.7 per barrel, its lowest level since before the outbreak of the U.S.-Iran conflict. U.S. benchmark WTI crude also declined, slipping below $67 per barrel.

During the conflict, both benchmarks rallied sharply as geopolitical risk premiums surged. However, most of those gains have now been erased following the 60-day ceasefire and the start of indirect negotiations aimed at reaching a lasting agreement.

Strait of Hormuz helps ease supply concerns

One of the strongest drivers behind the recent decline in oil prices has been improving conditions in the Strait of Hormuz. Tanker traffic through the strategic waterway has continued to recover, reducing concerns about potential disruptions to global energy supplies.

Before the conflict, roughly one-fifth of the world's oil and petroleum exports passed through the Strait, making any change in regional tensions an important driver of oil prices.

U.S. inventories fail to support prices

Additional downside pressure followed the latest report from the U.S. Department of Energy.

Crude oil inventories declined by around 2 million barrels, but the drawdown was smaller than the market had anticipated.

The data reinforced the view that the global oil market remains relatively well supplied, limiting the case for another leg higher in crude prices.

OPEC+ may increase production again

The next major event for the oil market will be this weekend's OPEC+ meeting.

According to media reports, the producer group is expected to increase output quotas by approximately 188,000 barrels per day starting in August. If confirmed, it would mark the fifth consecutive monthly production increase, reflecting OPEC+'s strategy of gradually restoring supply as prices ease.

Meanwhile, OPEC recently lowered its 2026 global oil demand growth forecast for a second consecutive month, cutting its estimate from 1.17 million to 970,000 barrels per day. Despite the downgrade, the organization continues to expect the global economy to remain resilient despite geopolitical uncertainty.

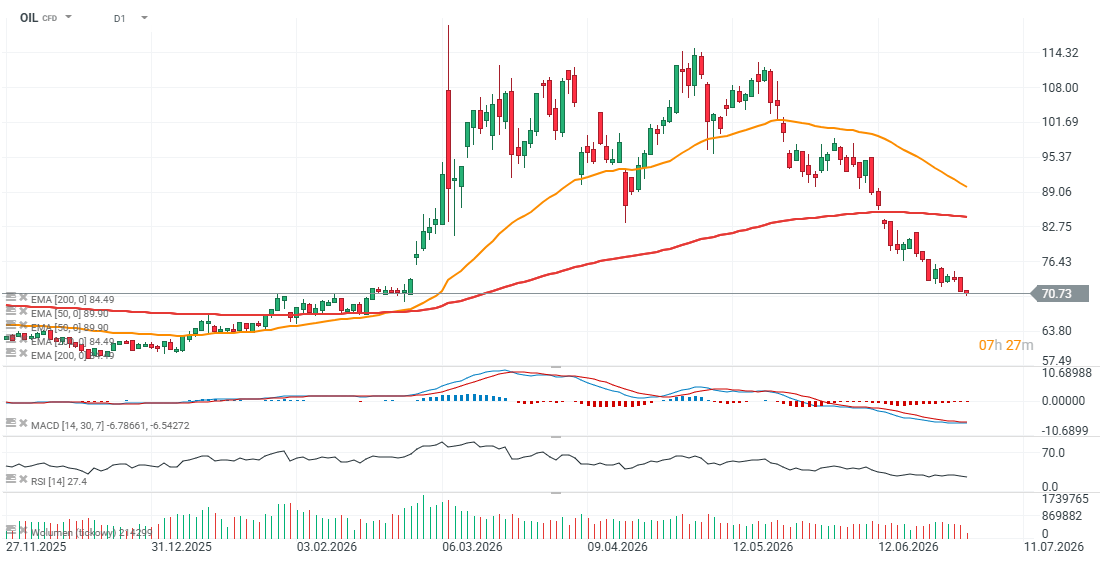

Focus shifts back to macroeconomics as the oil chart turns increasingly bearish (OIL, D1)

With geopolitical tensions easing, investors are once again focusing on central bank policy and the inflation outlook. Lower oil prices reduce the risk of renewed inflationary pressures, potentially allowing central banks to maintain a less restrictive monetary stance.

The coming weeks will determine whether negotiations between Washington and Tehran can produce a lasting agreement. If de-escalation continues and OPEC+ delivers another production increase as expected, crude oil could remain under pressure through the second half of the summer.

From a technical perspective, the picture has also become increasingly challenging for oil bulls. The OIL contract is down around 0.6% today, while the Relative Strength Index (RSI) has fallen to 27, signaling deeply oversold conditions following the sharp decline from the $115–120 per barrel area.

Source; xStation5

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

🔼 Gold gains 1.7%

🛢️Brent Crude Oil Tests $95 per Barrel

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.