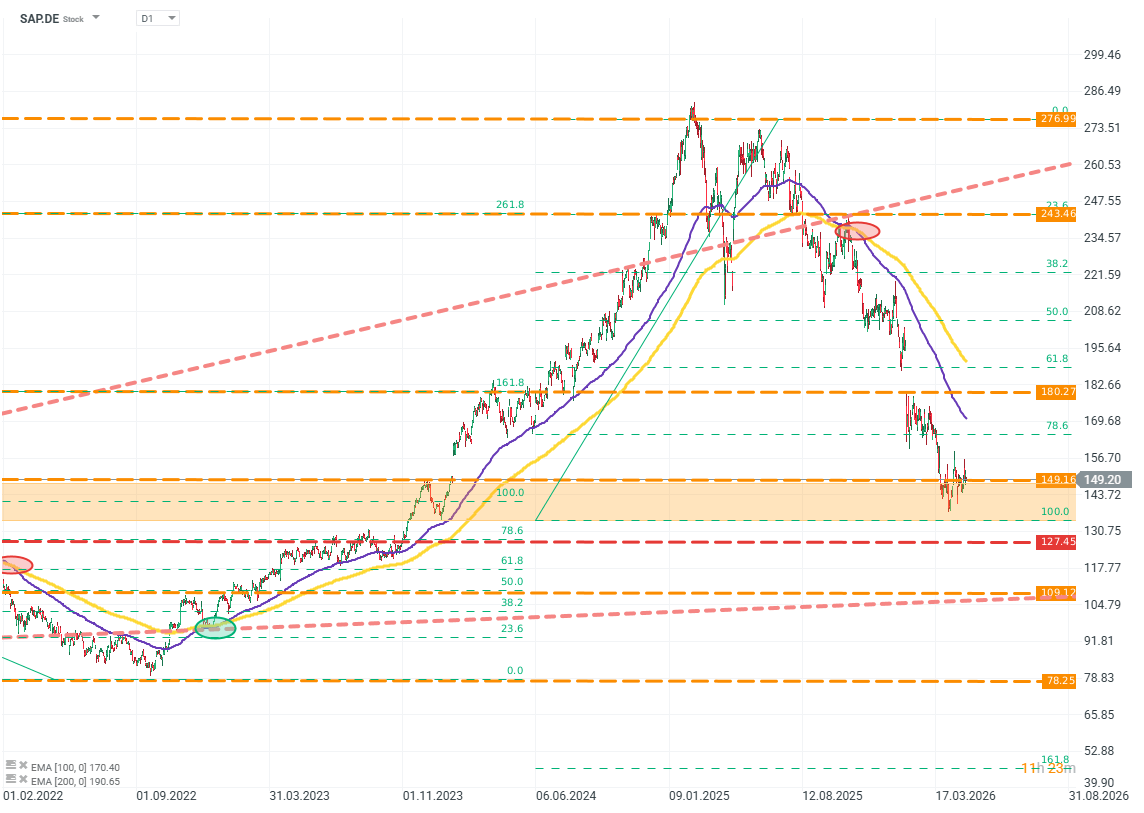

SAP, the German leader in the business software segment, has been through a very difficult period in terms of valuation. Since its all-time high in 2025, the company has lost about 50% of its value, with roughly 30% of that decline occurring in 2026 alone.

SAP.DE (D1)

Source: xStation5

The company’s results, however, show nothing that would justify such deep sell-offs. What does the market see in SAP that is not visible at first glance in the financial statements - and, more importantly, has the company actually deserved such steep declines?

“SaaS-pocalypse” is a journalistic term for a market phenomenon we have been observing for several quarters. It is characterized by deep (often very deep) sell-offs in companies based on “SaaS,” i.e., “Software as a Service.” This is not due to a sudden or fundamental loss of attractiveness of this business model. Rather, it is a consequence of expected, but poorly defined, “reshuffling” in the market as AI becomes more broadly and deeply integrated.

SAP Is Surrounded by an Ocean, Not a “Moat”

The assumptions are simple: if AI models reach a sufficiently high level, they will be able to recreate the products and services offered today by SaaS companies. Supporters of this thesis argue that sufficiently advanced AI models will be able to reduce the cost, requirements, and time needed to create software to such an extent that interested parties will be able to build it themselves - without having to buy expensive licenses or waste time on implementation.

This thesis, however, is built on such a far-reaching mental shortcut that it loses almost all of the context and nuance along the way, context and nuance on which these companies built their business models.

SAP and similar ERP systems are not a typical “app” that can simply be copied by AI or replaced with solutions based on LLM models. They are an entire enterprise operating environment: multilayered, multimodule, deeply embedded in specific business processes and regulatory compliance. Systems of this class are among the most complex software constructions in the business world. Even today, AI models still struggle with analyzing them, let alone replicating them.

Even if we take an extremely optimistic assumption that AI can perfectly recreate the functionality of SAP systems (or those of similar companies), this would still solve only part of the problem. The application is the end product here, not the entire competitive advantage. Replicating organizational, procedural, and infrastructure advantages is even harder - if not impossible.

AI may know how to program a system correctly. But does AI know what solution the client actually needs? That is a completely different question. One of the most crucial, most expensive, and persistently underestimated elements of the arduous process of acquiring business software is the merged process of requirements gathering, design, and implementation. These are not exaggerated questions, these are questions whose answers determine the final quality of the product, which in the case of business software can mean the difference between a company’s survival and failure. The narrative about AI’s advantages in this area doesn’t just fall apart - it often completely skips this key stage.

It is also worth thinking for a moment about the cost and profit structure of SaaS firms, including SAP. The main driver of costs is not raw materials or goods, it is the cost of hiring engineers, managers, and consultants. These are the people who, thanks to AI, will be able to work more efficiently, directly supporting the company’s profitability. AI models support work and management and eliminate the most tedious and time-consuming processes, directly reducing the marginal costs of product development.

This means that the company’s difficult-to-replicate, unique advantages remain in place: the brand, knowledge and expertise, customer base, logic and regulatory compliance. These elements will stay where they are, keeping the company ahead of competitors regardless of how cheap or advanced AI models become. This means that SAP can only benefit from the AI revolution - not lose.

It is also worth addressing the elephant in the room: the USA, the American tech sector, and the new administration’s policy toward, among other things, Europe. In business software at this level of sophistication and scale, SAP is the only publicly listed player in Europe. The other leaders - Microsoft, Oracle, and Workday, are US companies. In the current balance of power, these companies create a vulnerability and dependency that Europe can increasingly less afford.

Growth Pace vs. the Pace of Expectations

SAP’s valuation is also under pressure from more down-to-earth concerns, less driven by the impact of technology that may never materialize or may fall far short of the hopes and fears of many investors. That concern is the company’s growth rate.

In 2024 and 2025, the market viewed SAP as a growth company - but in 2025, suddenly it stopped. Why?

This perception problem partly overlaps with expectations about AI.

The market has lost faith that a company that does not increase its CAPEX by dozens of percent per year and does not build power-hungry data centers can grow enough to justify its previous valuation multiples. This largely comes down to the concepts of operating leverage and terminal value.

SaaS companies, even if they are profitable today and growing quickly, have operating leverage discounted by the market—and therefore a terminal (target) value, much smaller than what AI-sector companies are currently promising.

The problematic facts are:

- The divergence between these expectations boils down to the difference between what SaaS companies already have today and what AI companies might have - someday.

- The market does not seem to take into account whether a given company’s model is actually under pressure from AI adoption - it reprices entire segments of the market.

- Palo Alto’s CEO Nikesh Arora put this in a nuanced way: “The market must learn to distinguish between companies that will be hurt by AI, SaaS that must adapt to AI, and SaaS that will benefit from AI.”

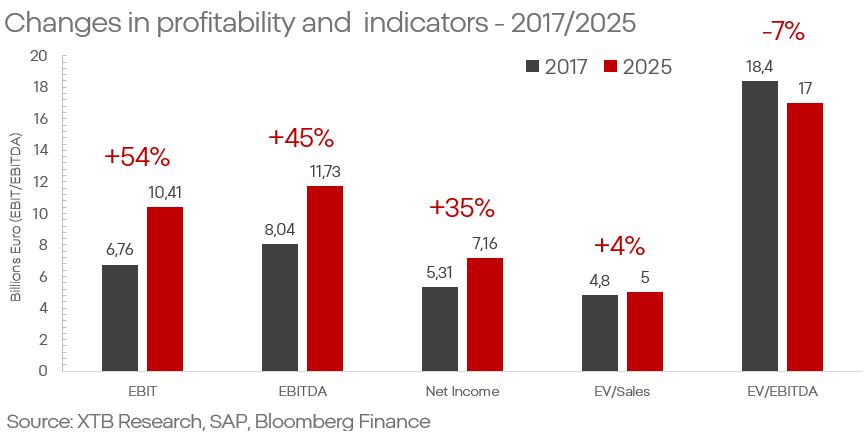

- Concerns about the quality of the company’s business model are in no way reflected in its financial results. The company keeps breaking records, and the growth rate remains impressive for an entity of this scale.

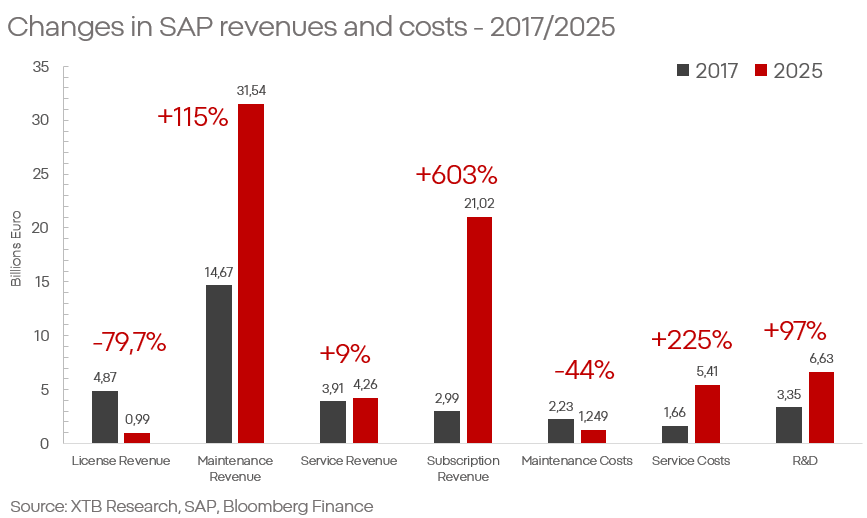

- Revenue growth from maintenance and subscriptions at SAP increases year-on-year on average by, respectively, over 10% and over 20%. At the same time, service-related costs are growing noticeably more slowly than sales, which supports profitability, the operating margin fluctuates around 73%.

- SAP is successfully executing its long-term transformation, based on shifting the company from a licensing model to subscriptions.

All these claims are clearly confirmed by the latest results. SAP has delivered another record quarter: revenue up 6%, net profit up nearly 20%. Particularly noteworthy are the cloud segments, up 20% - including backlog growth to nearly €22 billion, versus €18 billion a year earlier. The company clearly shows it is a beneficiary of structural changes - not their victim.

Aggregating forecasts from major analyst centers, there is no sign that projections for the coming years assume a collapse in growth. For 2026 and 2027, revenues are estimated at €40 and €44 billion, with EPS expanding to over €7 in 2026 and over €8 in 2027. This implies not only maintaining growth but also improving profitability. In the context of SAP and market expectations, it is also worth noting that the company has clearly beaten EBITDA expectations for seven years in a row.

What Does This Mean in Practice?

As of today, the market:

- Sells off high-quality companies based on threats that have not yet materialized.

- Rewards companies whose growth thesis is based on promises and hopes regarding technology whose perception is increasingly detached from business and technical realities.

SAP is a business that has survived for more than half a century, a business that defined and set standards for the industry. Neither SAP nor SaaS is going anywhere. Naturally, we should also assume that “AI” technology and LLM models will remain with us for a long time, and their impact on the market will be significant.

However, skepticism and prudence are needed when valuing the potential and nature of that impact. The capabilities of these solutions mainly support the profitability of SaaS companies and further highlight their market advantages.

A careful investor must ask: are the increasingly bold promises around artificial intelligence worth such large valuation premiums? And are the fears about the existing market leaders justified?

Kamil Szczepański

Financial Market Analyst at XTB

Bitcoin Near $64000 as ETF Inflows Return

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.