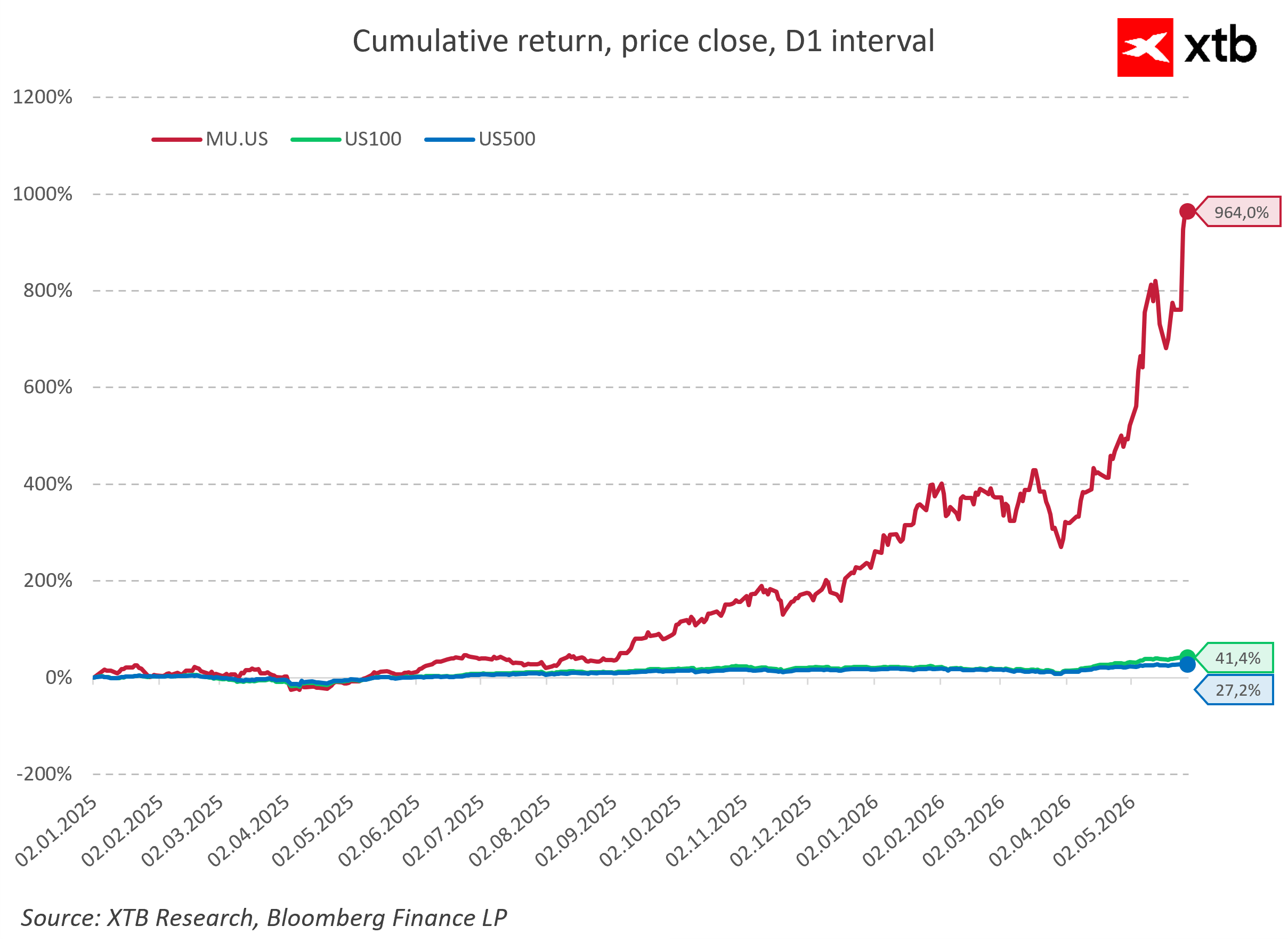

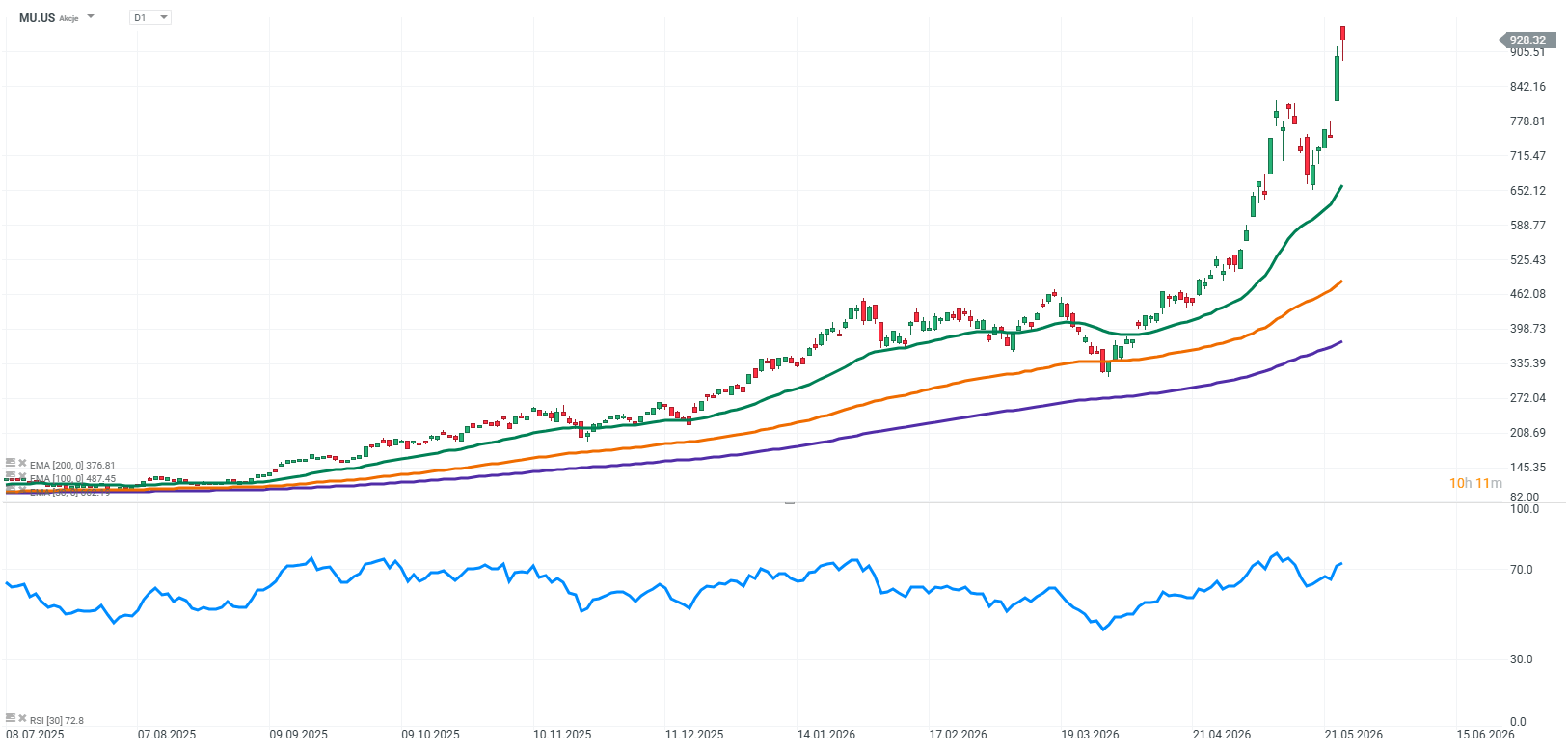

When the stock price of a technology company skyrockets by nearly 900 percent in just twelve months, a red warning light automatically flashes in the minds of investors. On the Micron Technology chart, this unprecedented rally looks like a textbook journey to the peak of a speculative bubble, from where the return to earth is usually painful. However, instead of announcements of a market crash, more and even more optimistic reports from investment banks keep pouring in from Wall Street. The largest institutional players are not only refraining from telling investors to take profits, but they are massively redefining their target prices, indicating that despite the cosmic growth, Micron still has another 50 or even 100 percent of upside potential ahead. This striking discrepancy between classic market intuition and the cold calculations of analysts raises a fundamental question whether the market has gone mad or Micron has become the beneficiary of a phenomenon that traditional valuation models simply cannot capture yet.

The anatomy of dominance or why HBM is the new crude oil

To understand why Wall Street sees the potential for Micron to further double its valuation, one must abandon thinking about this company through the prism of traditional RAM sticks installed in home computers. The key to unraveling the phenomenon of the nine hundred percent growth is the acronym HBM, which stands for High Bandwidth Memory, the high-throughput memory of the new generation. In the architecture of artificial intelligence systems, a paradoxical situation occurred where the most modern Nvidia graphics processors began to drastically waste their potential. Although they were capable of processing operations at cosmic speeds, they became stuck in the so-called memory wall, waiting for the necessary data packets to be transmitted by traditional DRAM circuits. HBM solves this problem in a revolutionary way because it is not just faster memory, but an entire three dimensional architecture of silicon layers stacked directly next to the graphics processor and connected to it by thousands of microscopic pathways. In a world where AI model training time is counted in millions of dollars per day, HBM has become a commodity as scarce and desirable as crude oil during the twentieth century automotive boom.

In this elite technological race, limited in practice to just three global players, Micron made an extremely bold and risky strategic decision. Instead of wasting resources on catching up with Asian competitors in the HBM3 standard, the Americans decided to completely skip this stage and throw all their strength into the development of the next generation designated as HBM3E. This engineering gamble paid off handsomely because Micron offered the market a product that consumes about thirty percent less energy than the solutions of its competitors. In the realities of modern data centers, where power consumption and generated heat represent an insurmountable barrier to the further development of large language models, such energy savings proved to be decisive. Thanks to this, Micron secured key contracts with the absolute leaders of the industry, becoming a strategic supplier for the latest GPU platforms from Nvidia and AMD, which immediately threw the company from the position of a chaser to the role of the leader of the technological peloton.

The consequence of this technological triumph is a phenomenon that has almost never happened in the history of the mass memory industry. Traditionally, manufacturers lived from quarter to quarter, reacting to current market orders, whereas Micron is currently reporting the complete sell out of its production capacity in the HBM segment for entire years ahead. Long term contracts with technology and cloud giants mean that the entire supply planned for the remainder of the current year and the following year has already been rigidly reserved based on prepayments and guaranteed prices. This unprecedented gap between the massive appetite of data centers and the physical production capabilities of the industry gave Micron a unique, almost monopolistic pricing power that completely demolishes the company's previous image as a supplier of cheap, easily replaceable components.

Financial analysis or the return from cyclical hell

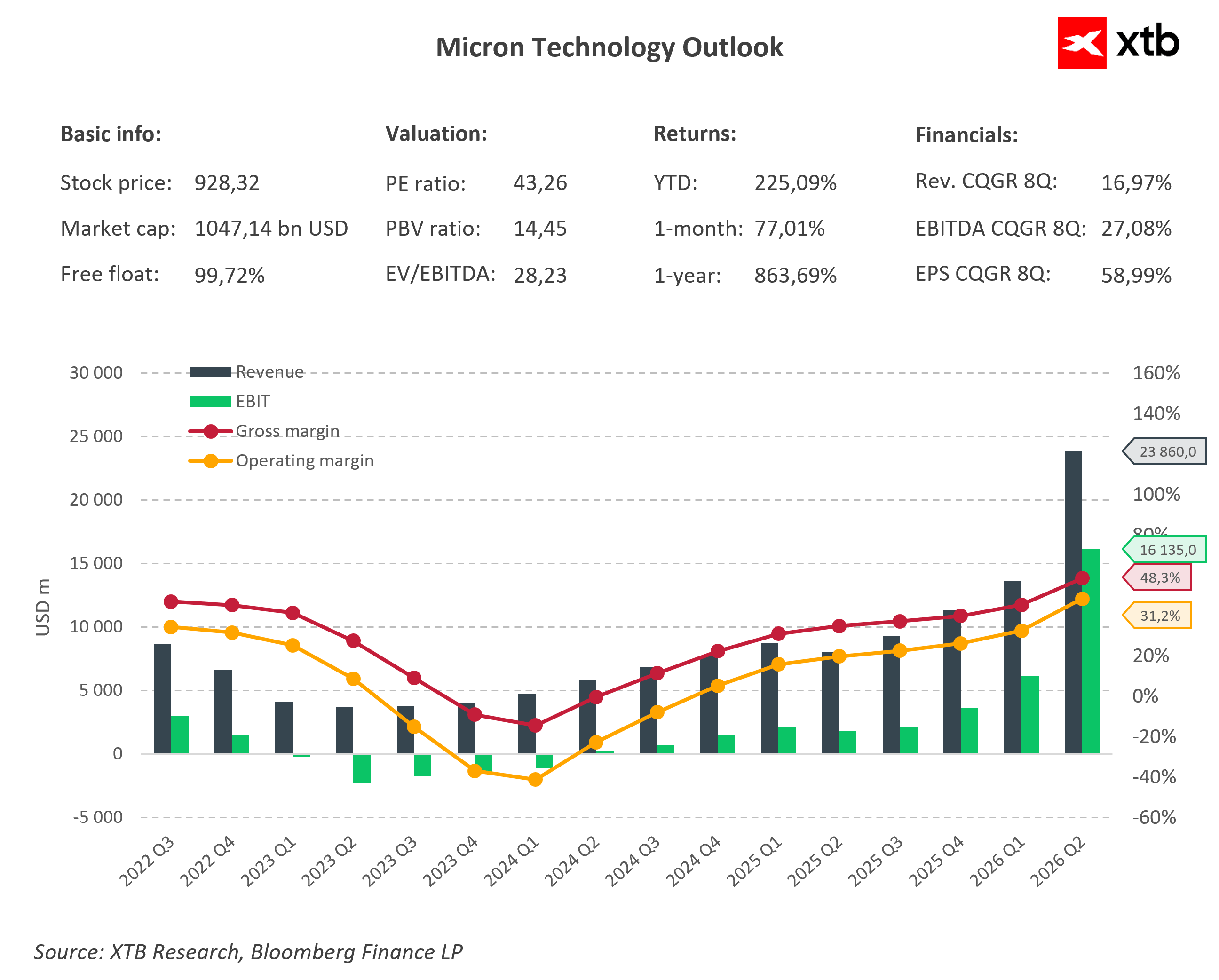

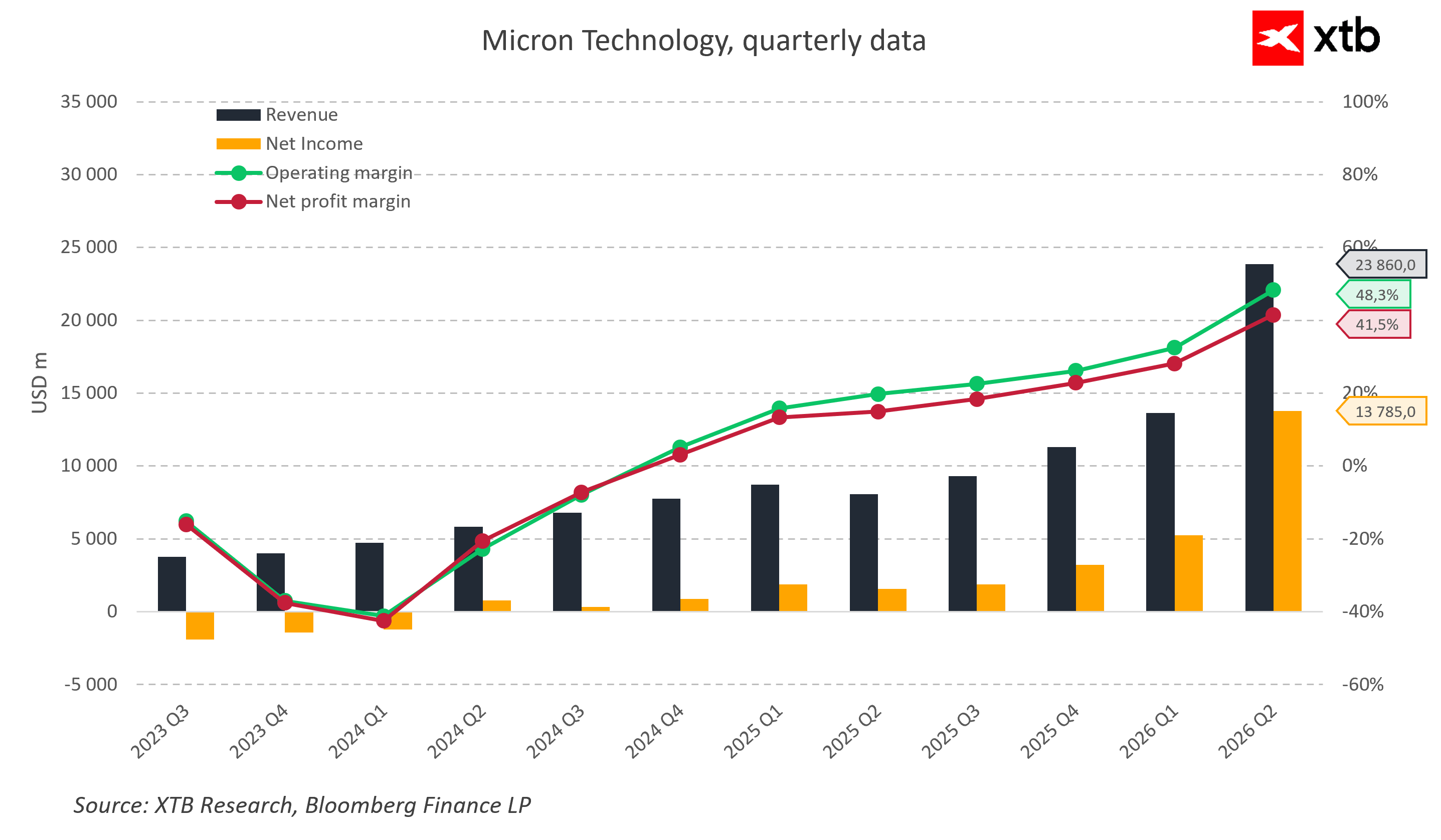

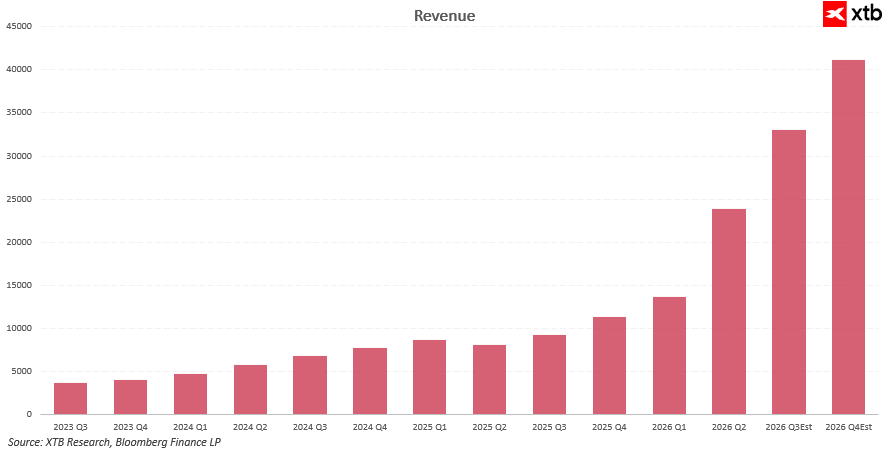

Understanding the fundamental change that has taken place at Micron requires clashing the current scale of the business with the dark period at the turn of 2023 and 2024. At that time, the company was deep on the defensive, recording negative operating results and real net losses that pushed net profitability into negative values in the worst quarters. The breakthrough, however, came with the 2025 fiscal year, in which annual sales reached approximately thirty seven billion dollars, generating over eight billion dollars in pure net profit.

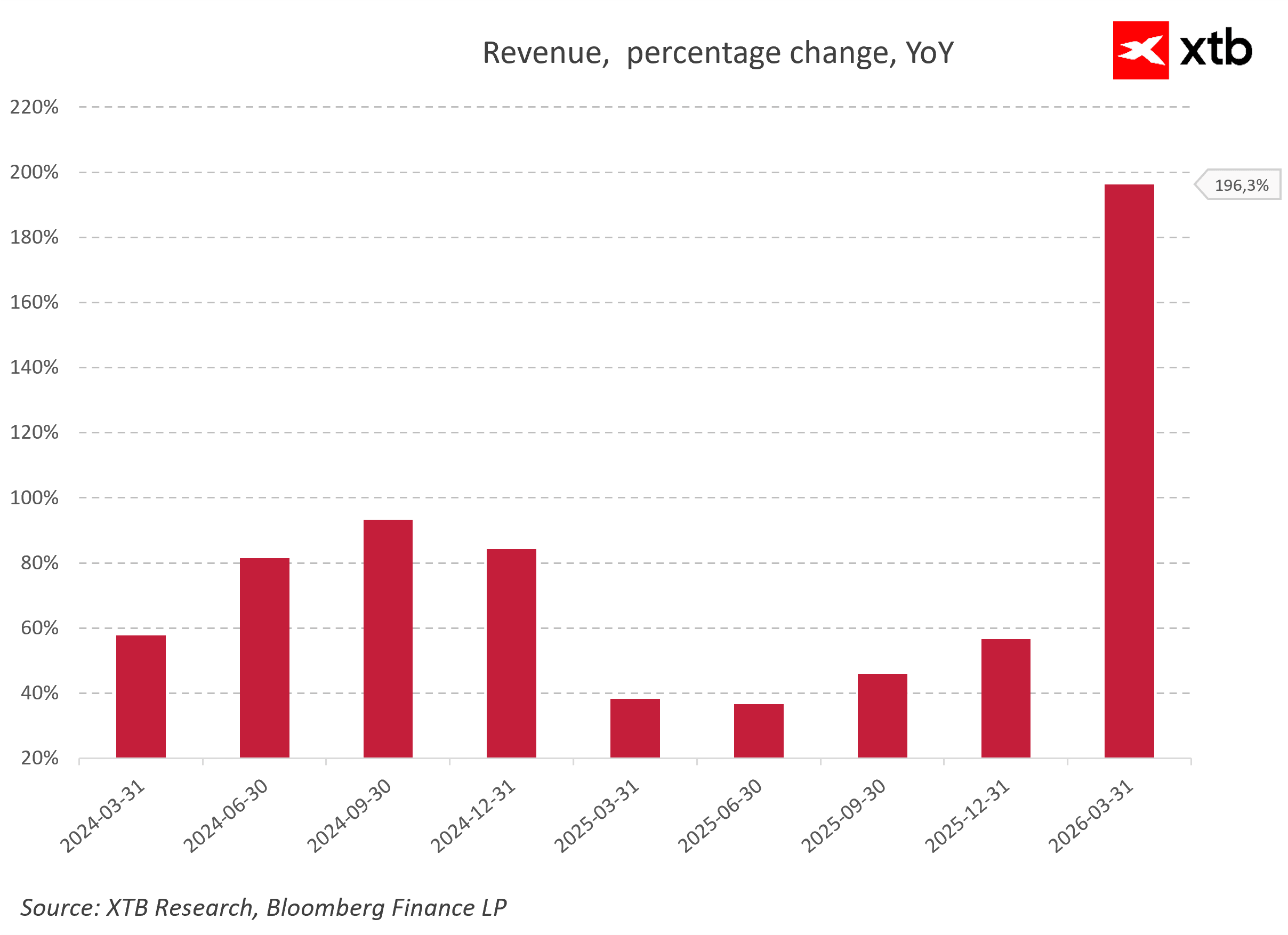

The real explosion of results occurred at the beginning of 2026, when the year over year revenue growth dynamics approached nearly 200 percent. In the second fiscal quarter of 2026, quarterly revenues skyrocketed to 23,860 million dollars, and net profit reached a spectacular value of 13,785 million dollars. The sharp increase in prices and sales volume meant that the operating margin reached 48 percent, while the net margin settled at 41 percent.

This spectacular set of numbers perfectly illustrates a classic market turnaround story that turned from a cyclical rebound into a permanent, structural memory supercycle driven by artificial intelligence. The comparison of revenues, net profit, and operating margins perfectly demonstrates how powerfully the operating leverage worked in Micron's business model. Along with the rebound in memory prices and volumes, margins first returned to positive levels and then climbed to areas that seemed unrealistic in this business just a few quarters ago.

This is not solely the result of an improvement in the general economic climate, but primarily the outcome of a conscious shift in the sales mix towards premium products, such as HBM, advanced DRAM, and SSDs for artificial intelligence, which are characterized by the highest profitability and a huge barrier to entry for competitors. At the level of sales dynamics, it is clear that the current cycle is not a short lived spike, but the consequence of several overlapping waves of demand. After rebounding from the 2023 bottom and a temporary cooling down along with inventory normalization, a re-acceleration occurred when AI projects entered the phase of mass deployment. The culmination of this trend is currently a massive, three digit revenue growth, which analysts link primarily to the skyrocketing demand for memory for data centers and full capacity utilization in the HBM segment.

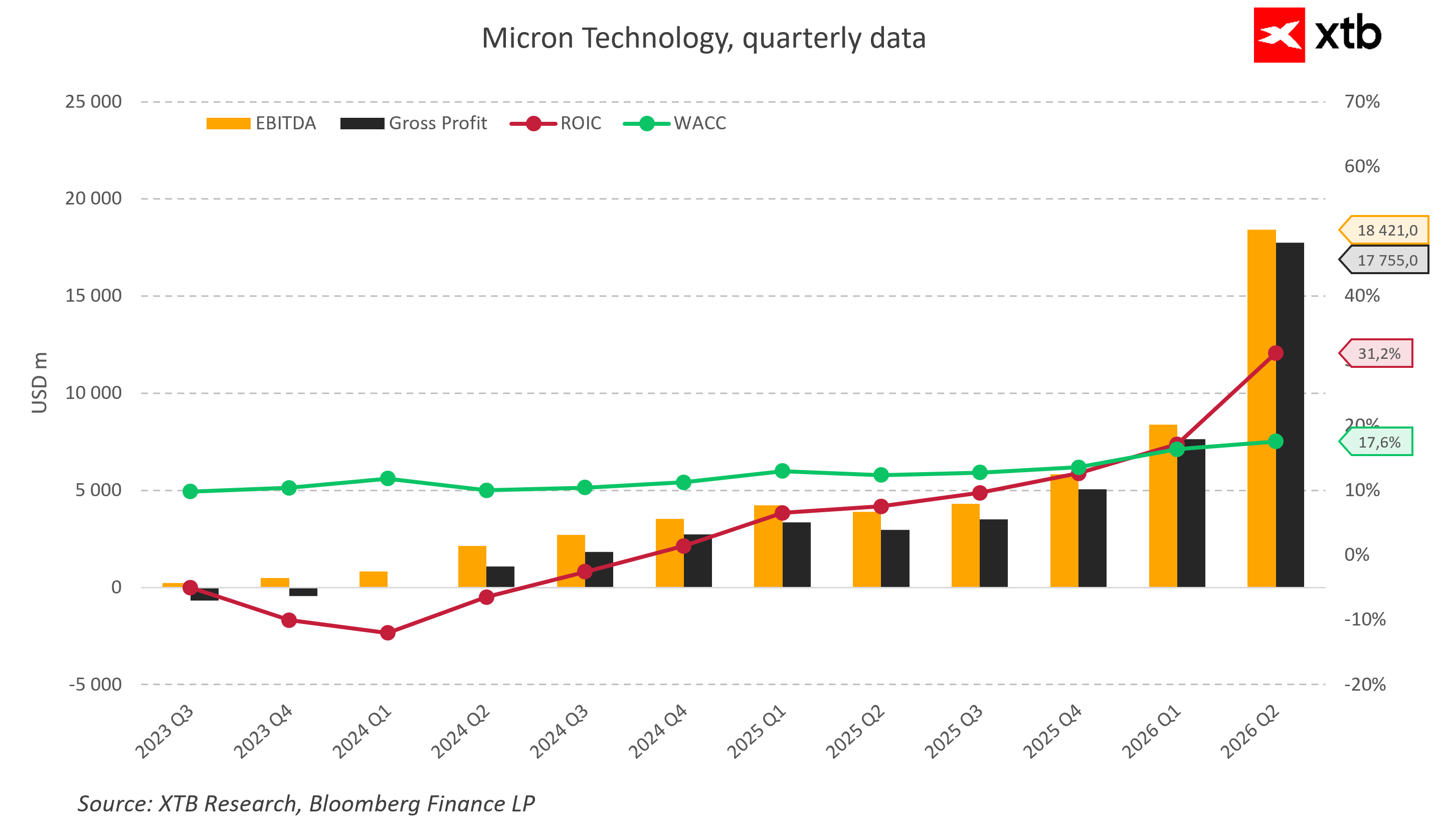

This unprecedented improvement in operating profitability brought about a fundamental change in the efficiency of capital management. Throughout long quarters of crisis, the return on invested capital remained deeply in the red, falling at the worst moment below minus ten percent and remaining far below the weighted average cost of capital, which stably fluctuated between 10 and 11 percent. This meant that Micron was realistically destroying value for its shareholders. The situation turned one hundred and eighty degrees with the arrival of the artificial intelligence era, when the return on invested capital began to climb sharply up, reaching an impressive 31 percent in the second quarter of fiscal year 2026. With the cost of capital rising to 17 percent, Micron began to generate a powerful economic premium. The business began to permanently create value above the cost of capital acquisition, which is typical for a phase of very strong demand advantage and limited supply in the semiconductor industry.

This fundamental improvement was almost immediately reflected in the stock quotes, and Micron's price since the beginning of the AI boom has many times outperformed the returns of the Nasdaq 100 and S&P 500 indices, achieving a return of nearly 1000 percent since the beginning of 2025. Such a sharp outperformance against the broader market suggests that investors treat Micron not as another component manufacturer, but as one of the main winners of the structural change in global infrastructure.

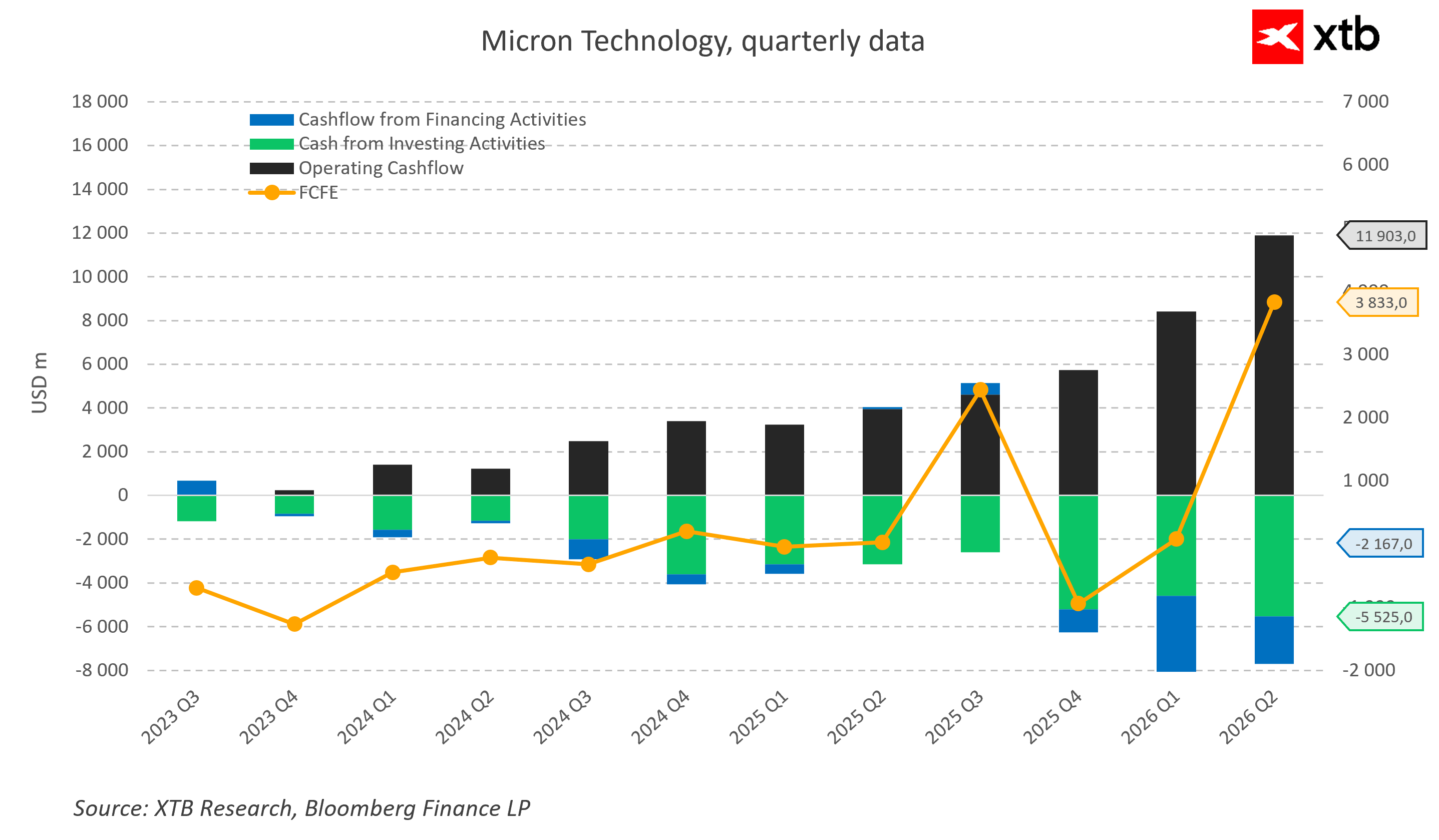

The most important confirmation of the quality of this growth, however, is the condition of the company's cash flows. During the collapse of the memory market, operating cash flow barely covered current needs, and free cash flows for shareholders were deep in the negative, forcing the financing of activities with debt. Micron has, however, transitioned to a situation where the growing cash flow from operating activities, amounting to nearly twelve billion dollars in the second quarter of 2026, begins to finance highly aggressive capital expenditures with a healthy margin.

Even with record investment outlays of five and a half billion dollars per quarter, free cash flows for shareholders shot upwards. This is a key element of this story because the company is building new production capacities mainly from internally generated cash rather than from debt or equity issuance, which drastically raises the quality of the entire business.

At the same time, revenue forecasts for subsequent periods suggest that the market does not expect a quick slide down from the peak, and the consensus assuming further growth in 2026, alongside third quarter forecasts at 33.5 billion dollars with a historic gross margin, confirms that the multiplication of the business scale expected by analysts is permanently entering the market landscape until the end of the current decade.

A look at the valuation

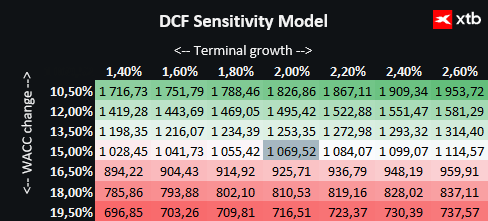

We present the valuation of Micron Technology using the discounted cash flow method. It should be emphasized that it is for informational purposes only and should not be treated as an investment recommendation or a precise valuation.

Micron is a key beneficiary of the global revolution in the field of artificial intelligence, providing advanced memory solutions for data centers and leading manufacturers of graphics accelerators. The company benefits from unprecedented demand related to the expansion of cloud infrastructure, the development of language models, and the digitalization of subsequent sectors of the economy, which creates exceptionally solid foundations for further growth.

The valuation is based on a base case scenario of revenue and financial results forecasts. The adopted cost of capital allows for a realistic picture of the market situation, and conservative assumptions regarding terminal value growth reflect a cautious approach to the future financial prospects of the company.

Taking into account the current share price at 928 and the valuation using the discounted cash flow method indicating an intrinsic value of 1070, the estimated upside potential is approximately 15 percent. This represents an attractive investment opportunity, especially for investors who believe in the further expansion of the company and the maintenance of its technological advantage in the semiconductor industry.

This positive fundamental perspective does not mean, however, that Micron has become an asset completely free of risk because the semiconductor industry by its very nature remains one of the most sensitive segments of the global economy. The greatest long term threat to ongoing growth is the risk of repeating the historical mistake of overexpanding production capacity at the very peak of market prosperity. Currently, all three global players are drastically and simultaneously increasing capital expenditures, and Micron's official announcement to allocate as much as 25 billion dollars for capital expenditures in the current year, alongside strategic plans to invest 200 billion dollars in the coming years, carries serious risk. If in a few years the rate of artificial intelligence adoption in global business unexpectedly slows down or if cloud customers begin to optimize their existing resources, a destructive oversupply of HBM memory will appear on the market, which could lead to a collapse in wholesale prices.

Added to this are highly complex geopolitical factors, as the drive for domestic production and the construction of huge manufacturing complexes in the United States under American government subsidy programs requires many years of work and generates massive fixed costs. Additionally, trade tensions between Washington and Beijing, export restrictions on advanced technologies, and potential disruptions in the supply of rare raw materials and specialized gases constitute a constant operational risk that can in a fraction of a second challenge even the most precise and daring forecasts of Wall Street analysts.

A cycle that became a structure

Micron Technology entered the era of artificial intelligence as an entity that redefined the market status of mass memory, transforming it from a dull infrastructure component into one of the most valuable resources of the modern digital world. Record revenues, an unprecedented expansion of operating margins, and a portfolio of orders for high bandwidth memory sold out under multi year contracts clearly prove that the current growth phase extends beyond the framework of a classic, short lived investment boom. What is extremely important, Micron's business stability is not a hostage to just one market segment. The company is deeply rooted in a number of other, parallel technological megatrends, which include the new generation of smartphones with built in artificial intelligence, modern personal computers, advanced autonomous driving systems in the automotive sector, and edge AI, which significantly broadens the demand base and creates a safe buffer mitigating potential future economic fluctuations.

The open question that most electrifies Wall Street remains whether the current supercycle will maintain its momentum until the end of the ongoing decade or whether in a few years the market will return to historical problems related to overproduction and price pressure from Asian competitors. However, cold mathematical calculations based on financial models show that even under conservative assumptions, Micron still possesses real intrinsic value exceeding the current market valuation. In a world where each subsequent generation of language models means an even greater hunger for data and the need for its instantaneous processing, the American giant has ceased to be merely an optional participant in the technological race. It has become one of its inviolable and absolutely crucial foundations, without which the further evolution of the digital world would be physically impossible.

Source:xStation5

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.