Micron has emerged as one of the biggest beneficiaries of the artificial intelligence boom, and its shares are among the strongest performers in the entire S&P 500 this year. Despite an explosion in financial results and record demand for memory used in AI, the company also remains one of the cheapest firms in the semiconductor sector. For some investors, this looks like an investment opportunity, but a growing number of analysts believe such a low valuation may be more of a warning signal than a green light for further buying.

Micron is rising like Nvidia, but is valued like a cyclical company

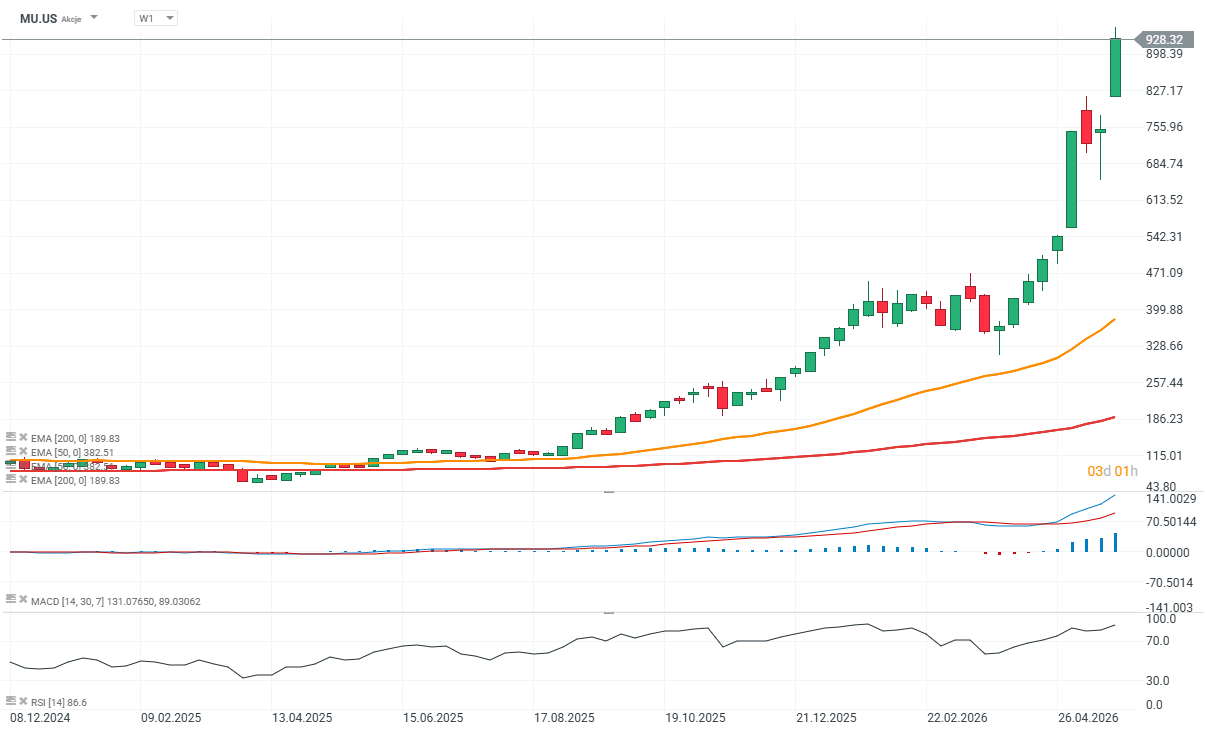

Micron currently trades at around 10 times forecast earnings, making it the cheapest company in the Philadelphia Semiconductor Index. At the same time, it is also among the cheapest companies in the entire S&P 500. This is an extremely unusual situation given the scale of the share price rally. Micron shares have risen by more than 1,000% since the end of 2024, while the company has already joined the elite group of firms with a market capitalization above $1 trillion. In May alone, the stock gained around 80%, marking its best monthly performance in more than 40 years.

The fundamentals also look impressive. In the latest quarter, Micron’s revenue almost tripled year-on-year, recording the fastest growth rate in data going back to 1990. Demand for HBM memory used in AI servers and data centers remains enormous, while investments by technology giants in artificial intelligence infrastructure continue to accelerate. The paradox, however, is that the market still values Micron more like a producer of commodity memory components than a strategic leader of the AI revolution.

Low valuation... A warning for investors?

In the memory market, very low valuation multiples have historically appeared close to the peak of the earnings growth cycle. The market then assumes that current record margins and results are difficult to sustain, and that the next stage will bring slower demand and declining profitability. This is why some investors interpret Micron’s current valuation as a warning signal. According to AGF Investments, the market may fear that the improvement in results has already reached an extreme level and that further growth from here will be difficult.

The current boom may resemble classic cycle peaks in the memory sector, although this time the scale of growth is completely unprecedented. The key question today is whether the AI boom has truly changed the entire semiconductor industry in a lasting way. If Microsoft, Amazon, Alphabet or Meta continue to spend heavily on AI data centers for many years, the traditional cyclicality of the memory sector may be partly broken. This is why Wall Street is beginning to consider entirely new valuation models for companies such as Micron.

AI could completely change how Micron is valued

More and more analysts believe Micron should be valued more like Nvidia than like traditional DRAM or NAND memory producers. UBS analyst Timothy Arcuri points out that AI may represent a lasting structural change for the entire semiconductor sector, rather than just another short-term technology cycle. Nvidia currently trades at around 21 times forecast earnings, more than twice Micron’s multiple. UBS has therefore raised its target valuation multiple for Micron and set one of the highest price targets on Wall Street, suggesting potential upside of around 75% over the next 12 months.

The bull case is based primarily on the fact that AI investments show no signs of slowing down. The largest technology players continue to allocate hundreds of billions of dollars to building data centers and developing artificial intelligence infrastructure, while high-bandwidth memory remains one of the key components of this market. If this trend continues for many years, Micron may stop behaving like a typical cyclical company.

Technical signals, however, are starting to warn of market overheating

Despite the very strong fundamental narrative, more and more warning signals are emerging from the technical analysis side. The scale of the recent gains has been extremely aggressive, and Micron recorded its best month in decades, with some individual trading sessions bringing gains of nearly 20%. The stock’s RSI is already at levels considered strongly overbought.

As a result, the market may be approaching a so-called “climax move”, the final phase of a very dynamic bull run, often followed by sharp corrections. The current average Wall Street analyst target is now below the current share price and implies a decline of around 25% over the next 12 months. This shows how divided the market remains in its assessment of Micron’s future.

On the one hand, investors see a potentially historic transformation of the entire memory market thanks to AI. On the other, there is still the risk that the current euphoria will prove to be just another extreme peak of the classic semiconductor cycle, and that memory chips will eventually become oversupplied. The company itself expects memory market shortages to persist into 2027.

Source: xStation5

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.