The technological race in the era of the digital economy is most often viewed through the lens of American tech giants. NVIDIA provides computing power, Microsoft and Google develop artificial intelligence models, while Amazon builds global cloud infrastructure. In this picture, Europe often appears more like an observer than an active participant. But that picture is incomplete.

Alongside the entire race for AI, there is a company that builds neither language models nor hyperscale data centers, yet remains one of the most important pillars of the global digital economy. A company without which thousands of the world’s largest organizations simply could not function normally.

That company is SAP.

SAP is not a typical software company focused on single purpose applications. It provides systems that sit at the very center of how enterprises operate. Its software records everything that matters inside a business: finance, manufacturing, logistics, procurement, HR, and supply chains. It is not a tool sitting “next to the business,” but rather its digital backbone.

That is why SAP is more than just another technology company. In practice, it controls the layer where the digital representation of the real economy is created. And in the age of artificial intelligence, that layer is becoming increasingly valuable.

Because AI, regardless of how advanced it becomes, still depends on data. Not just any data, but structured, reliable, real time operational data generated by actual business processes. This is precisely where SAP occupies a uniquely privileged position.

From a European perspective, this carries another dimension. In a world where most critical digital technologies originated in the United States, SAP remains one of the very few truly global technology players built in Europe and still headquartered there today. As a result, SAP is increasingly discussed not only as an IT company, but also as a strategic asset for the continent itself.

In effect, SAP is no longer viewed as simply another software vendor, but as a piece of economic infrastructure connecting the traditional economy with the emerging AI era.

And that is why any serious discussion about AI should occasionally step away from models and chips, and focus instead on something far less visible, yet equally important: the systems that have quietly kept global business operations running for decades.

What SAP Actually Is and Why It Is Not a Typical SaaS Company

SAP is often grouped together with SaaS companies, but in reality it belongs to a completely different category of software.

This is not a standalone application. It is a system that integrates the entire enterprise. Finance, production, logistics, procurement, sales, and HR all operate within one environment, effectively forming the operational backbone of large organizations.

Most importantly, SAP does not merely support these processes. It records them. Its systems create the digital representation of what actually happens inside a company, from invoices and deliveries to financial decisions and workforce management. In practice, SAP becomes the system of record for the enterprise.

That fundamentally differentiates it from traditional SaaS products. Many software tools can be replaced relatively quickly. Replacing SAP, however, would often require rebuilding an organization’s operational infrastructure over many years and at enormous business risk. That makes SAP far closer to infrastructure than to conventional application software.

Around this core, SAP has built a broad ecosystem of products and services. As a result, SAP is not a single product, but rather an environment that organizes how large enterprises function.

This structure is precisely what makes SAP significantly harder to replace than typical SaaS solutions. It behaves less like an application and more like the digital operating backbone of modern corporations.

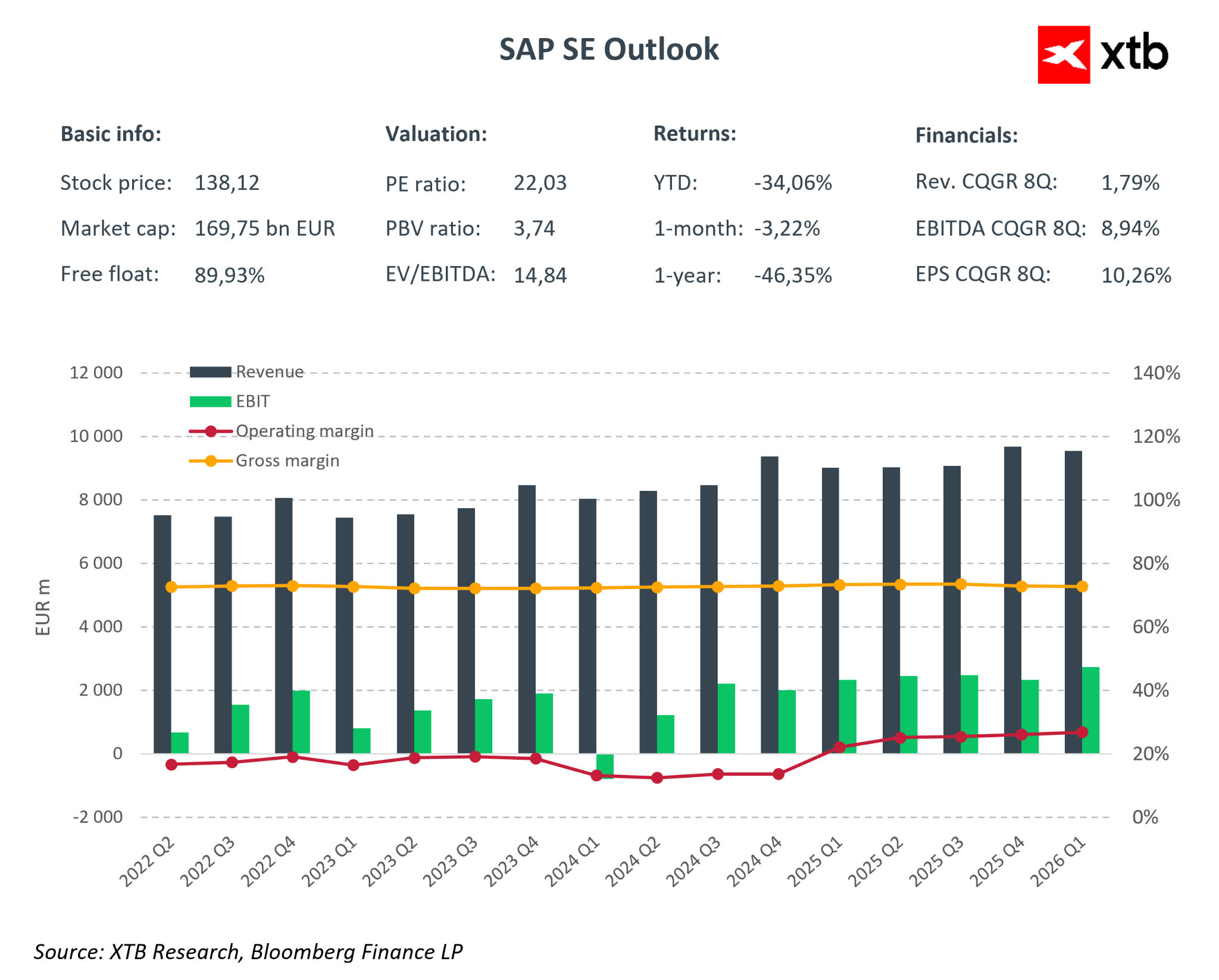

Financial Analysis: SAP’s Transition Into a New Growth Phase

Recent quarters show a company that has evolved beyond being a traditional software vendor and increasingly resembles mature digital infrastructure for the global economy. The results for the first quarter of 2026 only reinforce this picture.

Key Financial Highlights (Latest Quarterly Results)

- Total revenue: approximately €9.4–9.6 billion, up year over year

- Cloud revenue growth: approximately 20% year over year

- Cloud backlog: continued growth to over €50 billion

- Operating margin: improved to approximately 27–28%

- Net income: annual growth supported by stronger margins

- Free cash flow: significant improvement and return to strongly positive levels

- Net debt: maintained at a safe and controlled level

- Cloud revenue mix: continued expansion of recurring cloud revenue share

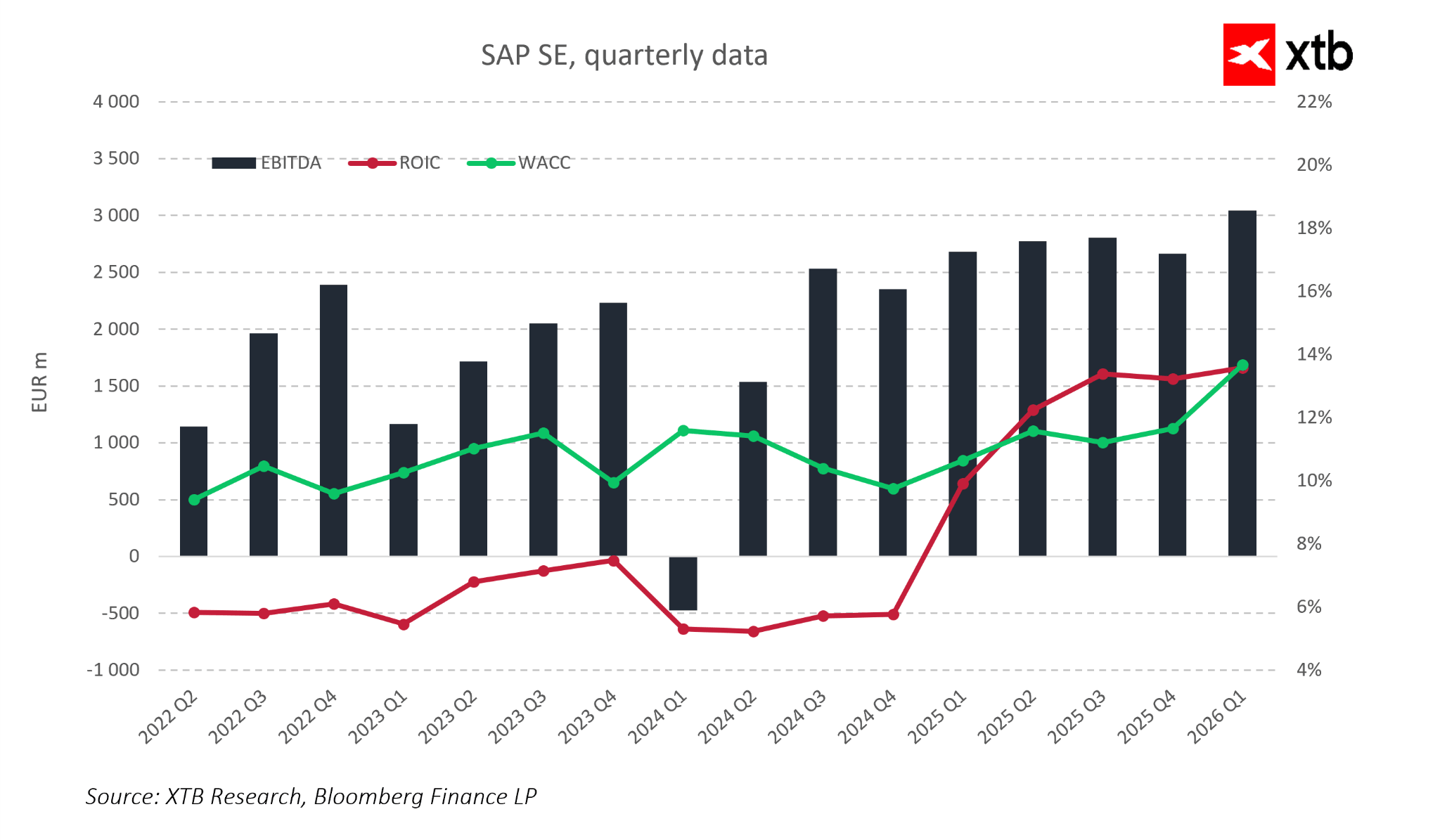

Revenue in the first quarter of 2026 reached approximately €9.6 billion, representing 6% year over year growth. At first glance, this may not seem extraordinary in the technology sector, but for SAP the key factor is not headline growth, but the structure of that growth. The cloud segment expanded by 19%, or 27% at constant currencies, showing that the company’s primary growth engine continues to accelerate despite a difficult macroeconomic environment.

An even stronger signal comes from current cloud backlog, which reached €21.9 billion and increased 25% year over year. This metric arguably provides the clearest picture of SAP’s near and medium term future. In practice, it reflects already contracted but not yet recognized revenue, effectively orders already sitting in the system that will gradually convert into future sales.

In this context, SAP is not a company that must constantly fight for every new contract. An increasing share of future performance is already secured through signed agreements, giving the business the profile of a long duration cash flow compounder.

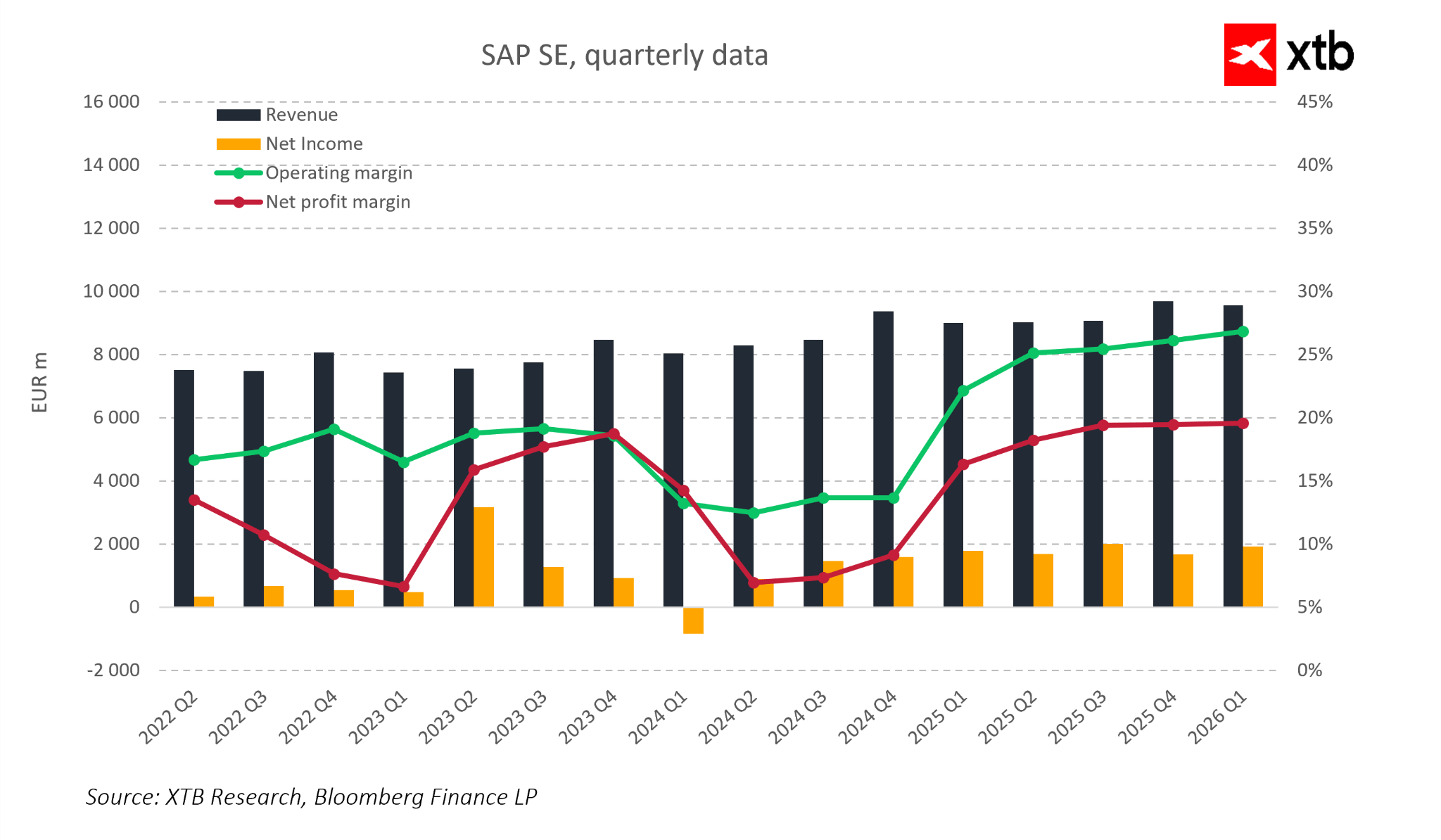

Profitability also remains extremely strong. Operating margin in Q1 2026 approached 30%, marking a clear improvement compared with previous years and confirming the scale advantages SAP is achieving through its cloud model. Revenue growth is increasingly paired with cost discipline, which remains one of the defining characteristics of high quality long term software businesses.

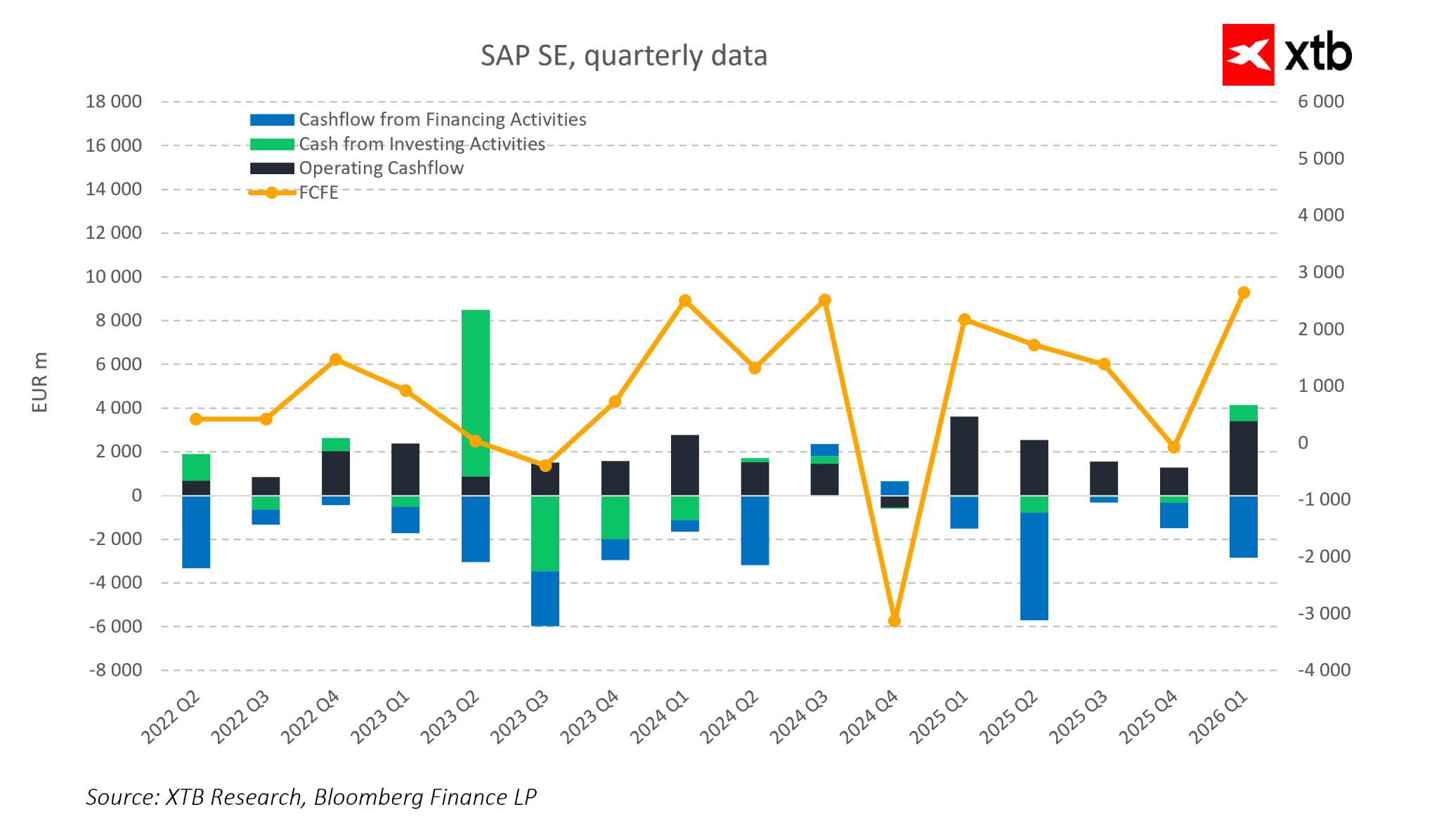

Cash flow is another critical element. SAP generated more than €3 billion in free cash flow in a single quarter, confirming that its transition toward a subscription driven model is now translating into tangible financial outcomes. While quarterly cash flows may fluctuate, the long term direction is increasingly clear: SAP is becoming a significantly more cash generative company.

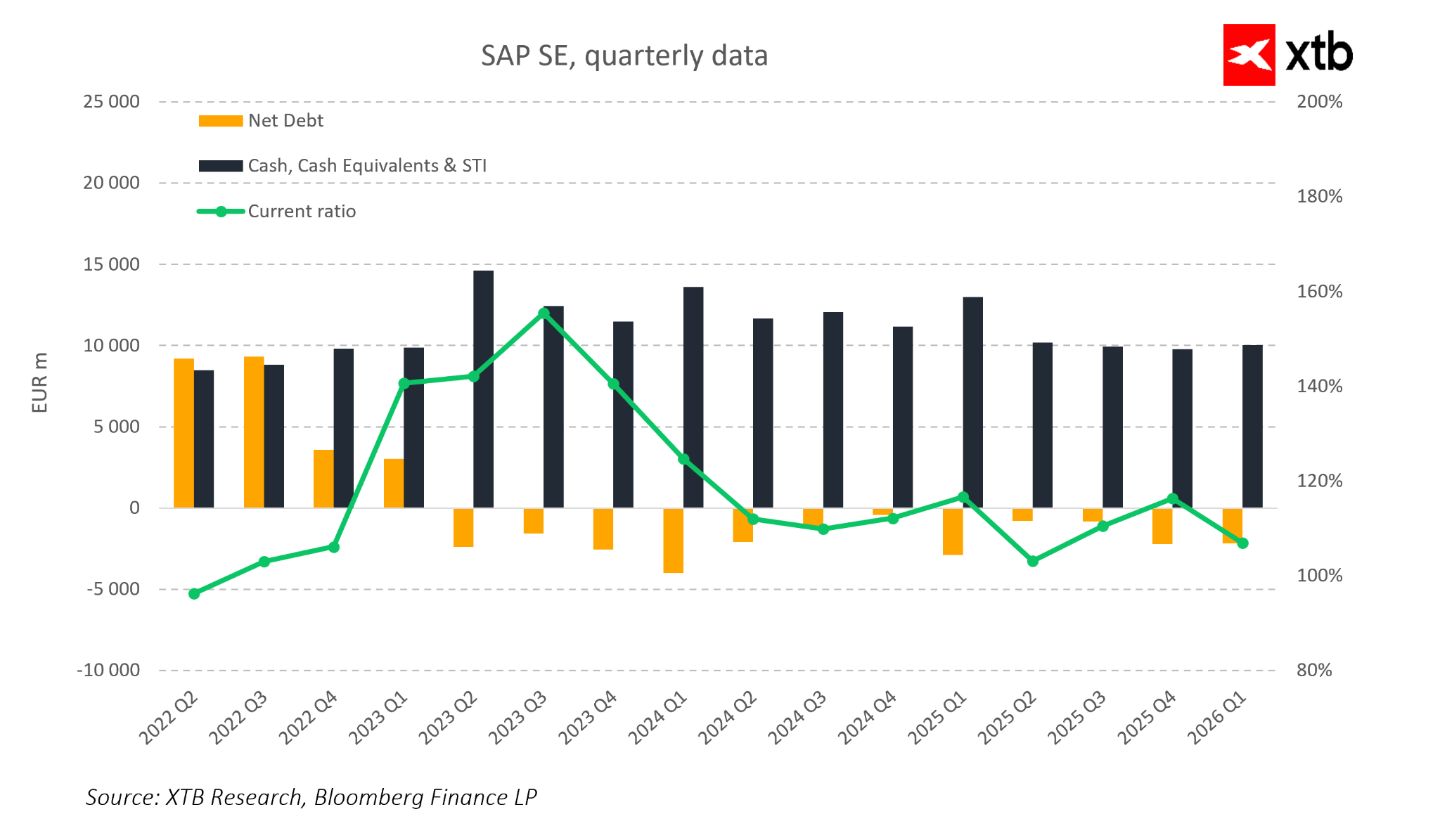

At the same time, SAP maintains one of the more conservative balance sheets among large technology companies. Low net leverage and strong liquidity provide financial flexibility to invest in AI development, maintain share buyback programs, and continue expanding its cloud ecosystem.

Taken together, these figures paint a coherent picture. SAP is no longer a company in transition. It is increasingly a company that has already completed much of that transition and is now beginning to monetize its effects. The shift from licensing toward cloud subscriptions has not only increased recurring revenue, but also improved visibility into future performance.

In this context, the key question is no longer whether SAP can grow quickly, but whether it can grow in a stable and predictable way. Based on recent results, the answer appears increasingly clear: yes.

SAP in the Era of AI and Geopolitics: The Quiet Operating System of the Global Economy

In discussions surrounding artificial intelligence, attention naturally gravitates toward models and AI agents, the most visible layer of the stack. But the truly critical layer exists lower down, where the operational data of the global economy is actually created and maintained.

AI does not operate in a vacuum. It depends on structured, trustworthy financial, logistical, manufacturing, and workforce data. Those datasets are not created inside models themselves, but within ERP systems that record and structure real economic activity. Without that foundational layer, AI remains little more than an analytical interface disconnected from operational reality.

Within this structure, SAP occupies a uniquely important position. Across many global enterprises, SAP functions as the central operating system of the business itself. It is where the operational “source of truth” exists, where finance, supply chains, production, procurement, and HR processes are recorded and executed. In practice, this makes SAP far more than a software provider. It becomes infrastructure underpinning a meaningful portion of the global economy.

From the perspective of AI, this is critically important. Models may optimize and automate processes, but they still require reliable operational data from systems like SAP. That shifts SAP’s role from being a traditional ERP vendor toward becoming the infrastructure layer supplying the foundational data environment for enterprise AI.

The second dimension of this transformation is geopolitical. Global digital infrastructure remains heavily dominated by American cloud providers and AI ecosystems, while Europe often acts primarily as a consumer rather than a creator of these platforms. Against that backdrop, SAP represents one of the few truly European pillars of global business infrastructure.

The growing importance of digital sovereignty means systems like SAP are no longer judged solely by operational efficiency. Increasingly, organizations care about where data is processed, who controls it, and under which regulatory frameworks it operates. Through sovereign cloud initiatives and enterprise focused infrastructure, SAP aligns directly with these priorities, strengthening its role as infrastructure compatible with European regulatory and data governance standards.

A further layer of change emerges with the rise of AI agents. Instead of humans manually interacting with dozens of systems, AI increasingly performs tasks autonomously on behalf of users. In that environment, SAP does not become less important. It arguably becomes more important, because it serves as the execution layer for AI driven operations.

Models may recommend, optimize, and plan processes, but execution must ultimately occur inside systems that represent operational truth. In practice, this shifts SAP from being a traditional ERP platform toward becoming the infrastructure layer on which intelligent business agents actually operate.

As a result, SAP’s role in the AI ecosystem is not about competing with frontier models themselves. Its role is to provide the environment in which those models can interact with the real economy.

And that ultimately changes how SAP should be viewed. It is no longer merely a software company. It increasingly resembles a quiet but essential layer of digital infrastructure connecting the traditional economy with the next generation of AI driven systems.

Valuation Perspective

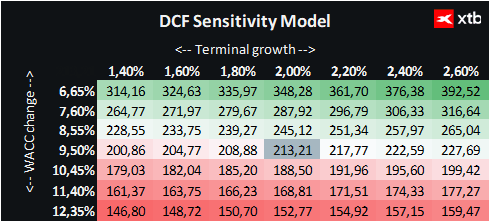

Below is a discounted cash flow valuation of SAP SE. It should be emphasized that this valuation is purely informational in nature and should not be treated as investment advice or as a precise estimate of fair value.

SAP is a global leader in enterprise software whose systems form a critical foundation for a large portion of the world economy. The company benefits from accelerating cloud adoption, the increasing importance of recurring subscription revenue, and the growing role of data and artificial intelligence in enterprise operations, all of which create strong foundations for long term growth.

The valuation is based on a base case scenario for future revenue and financial performance. The selected cost of capital reflects a balanced and realistic framework, while conservative terminal growth assumptions aim to maintain a prudent long term perspective.

Taking into account SAP’s current share price of approximately €138 and a DCF valuation of approximately €213 per share, the implied upside potential stands at roughly 54%.

This suggests a significant gap between current market pricing and the company’s estimated intrinsic value, particularly given the increasing predictability of SAP’s cash flows and the continued transition toward a cloud based recurring revenue model.

Technical Perspective

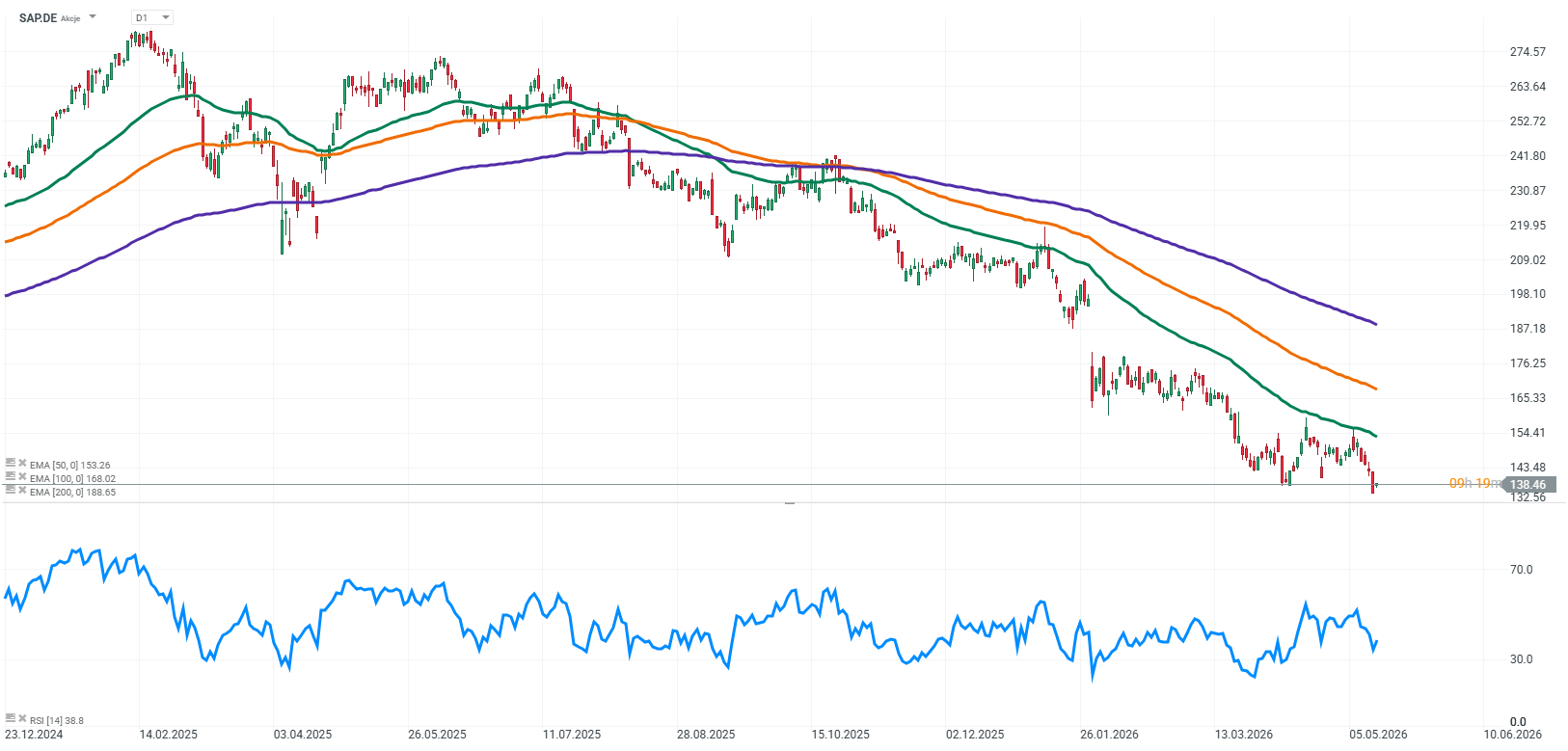

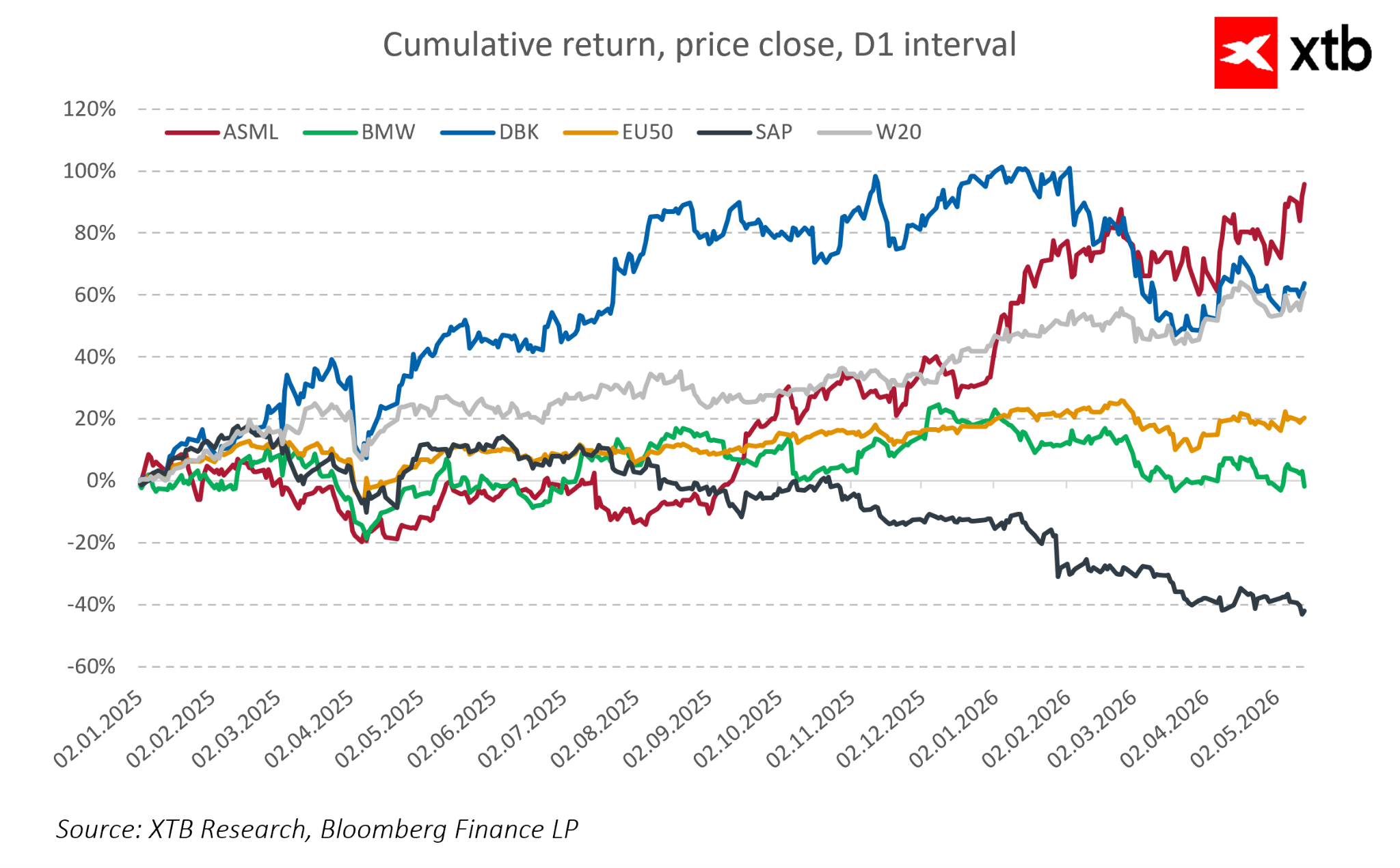

Looking at SAP’s share price over a broader timeframe, the stock currently appears to be trading through a meaningful correction relative to previous highs, despite business fundamentals remaining relatively strong. Periods of market pressure have not materially altered the long term picture of a company that continues expanding cloud revenue, strengthening recurring cash flows, and building a more predictable business model.

The recent correction is not fully reflected in operational performance. SAP continues reporting cloud growth, expanding backlog, and strong operating margins, reinforcing the view that much of its business transformation has already been completed and is beginning to generate measurable financial benefits.

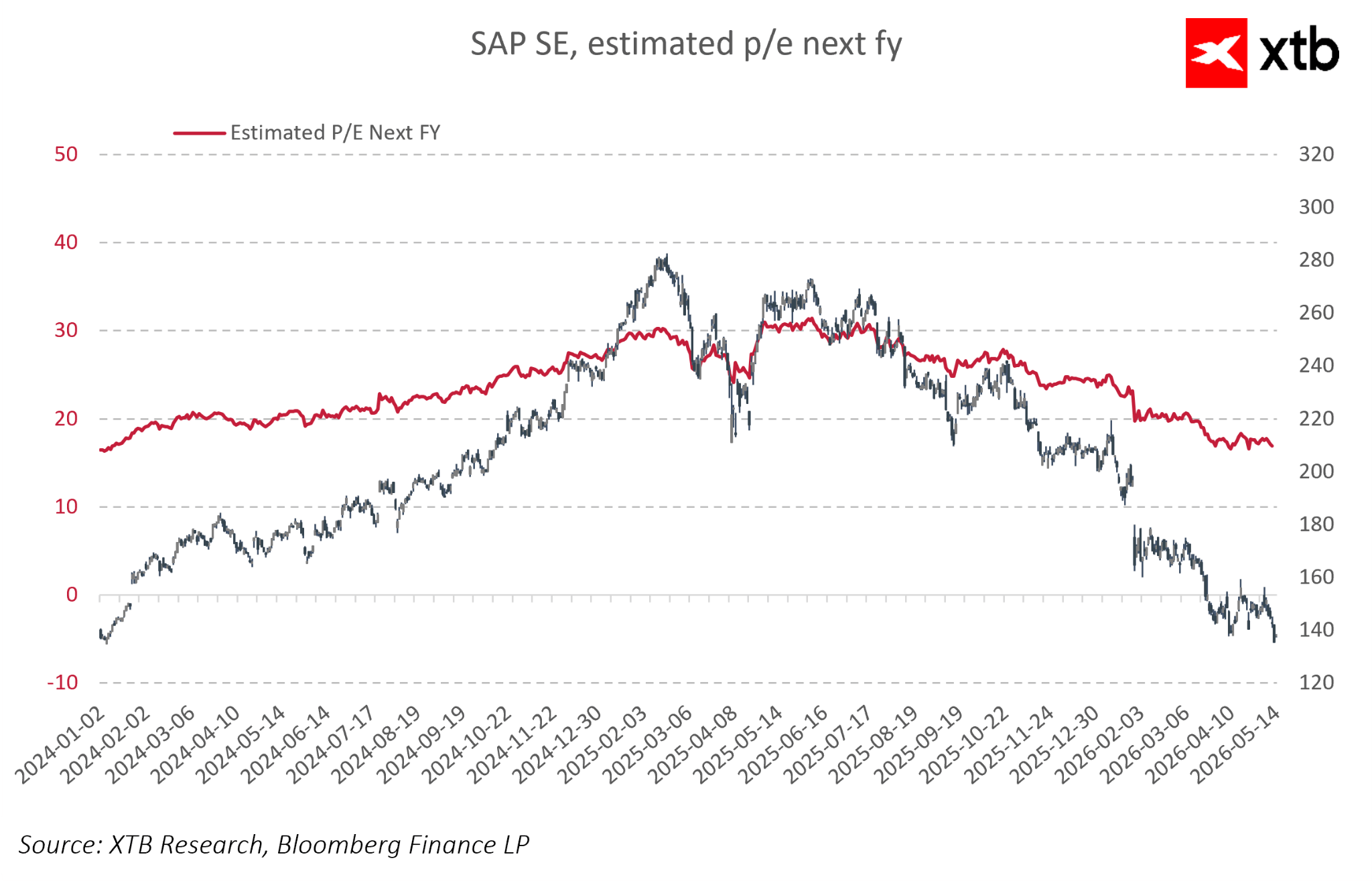

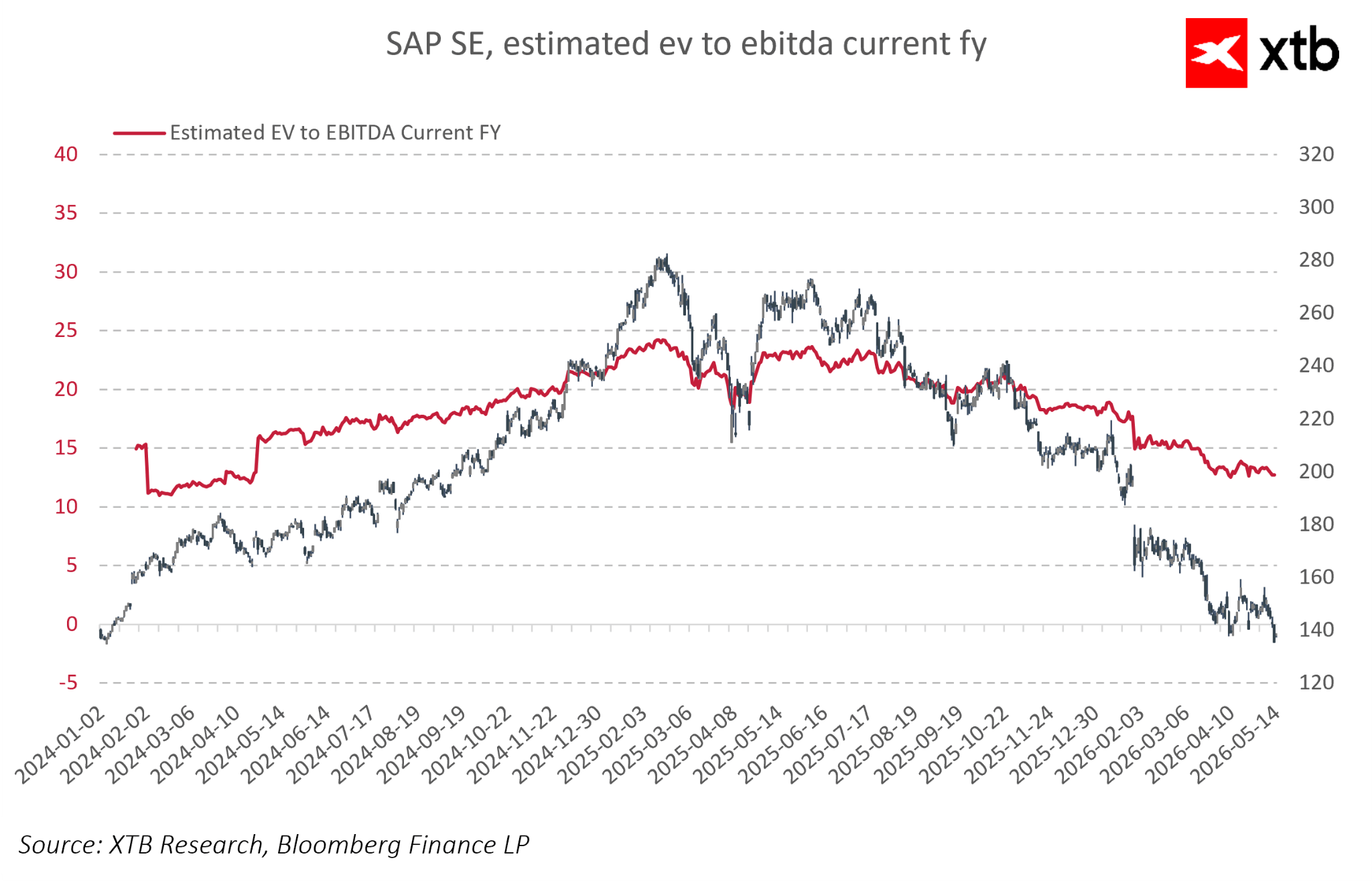

At the same time, recent months brought a visible compression in valuation multiples. Forward P/E ratios declined from around 30x toward roughly 17–18x, while EV/EBITDA multiples compressed from above 23x toward the low teens. This suggests the market has become materially more cautious regarding future growth expectations and less willing to maintain elevated valuation premiums.

In this context, the current valuation may not fully reflect either the scale of SAP’s transformation or its increasingly strategic role within digital infrastructure and enterprise AI. The company’s fundamentals remain strong, while its business model increasingly resembles that of a mature platform capable of generating stable and recurring cash flows, characteristics that historically supported premium valuations among high quality technology businesses.

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.