Target Hospitality is a niche company that provides accommodation for workers in remote parts of the United States. So far, the company’s business has been based mainly on building and operating temporary housing facilities for, among others, the extractive and construction industries.

The company has just held an interesting earnings call.

- Revenue fell again, to USD 72.8 million, representing a roughly 20% quarter-over-quarter decline.

- EPS looks even worse: the company has reported losses for five consecutive quarters. The loss in Q1 2026 came in worse than expected, reaching -USD 0.13 versus the expected level of around -USD 0.10.

- Adjusted EBITDA looked better, coming in at USD 9.94 million versus expectations of USD 8.5 million. However, given the rest of the data, it is fair to ask to what extent the strong adjusted EBITDA reflects operational efficiency rather than, for example, accounting effects.

After the results, the stock is up as much as 14% - it likely would not have risen that much while showing a widening loss. Investor optimism stems from a massive contract the company reportedly won, expected to bring in USD 750 million over the “next few years.”

This contract allowed the company to raise profitability forecasts by more than a dozen percent as early as year-end 2026.

Management increased its year-end revenue target to USD 375 million (vs. USD 325 million) and its EBITDA target to approximately USD 80 million (versus prior estimates of around USD 73 million).

This is not the first such contract recently. In April, the company announced another contract worth USD 550 million. The first question that arises in light of this information is: who is paying hundreds of millions of dollars for modular housing containers and mobile toilets?

Of course, both contracts relate to supporting the construction and operation of AI data centers, and the company emphasizes the strategic nature of this shift and its reorientation toward that segment. From the company’s perspective, it’s a home run: it keeps its existing business model unchanged—only the customer changes, to one whose enormous CAPEX budgets can support higher margins. From an investor’s perspective, however, it may be worth asking how durable such growth and margin improvement really are.

This leads to a second question. It is important to add context: Target Hospitality reached its peak in revenue and profitability in 2023 and has been on a downward trajectory since then. From this perspective, the company’s rebound looks like a temporary attempt to latch onto a broader market trend that has stopped asking hard questions about the durability of solutions, the rationality of growth, or the cost of investment.

Some investment firms also appear optimistic, raising their price targets on the stock.

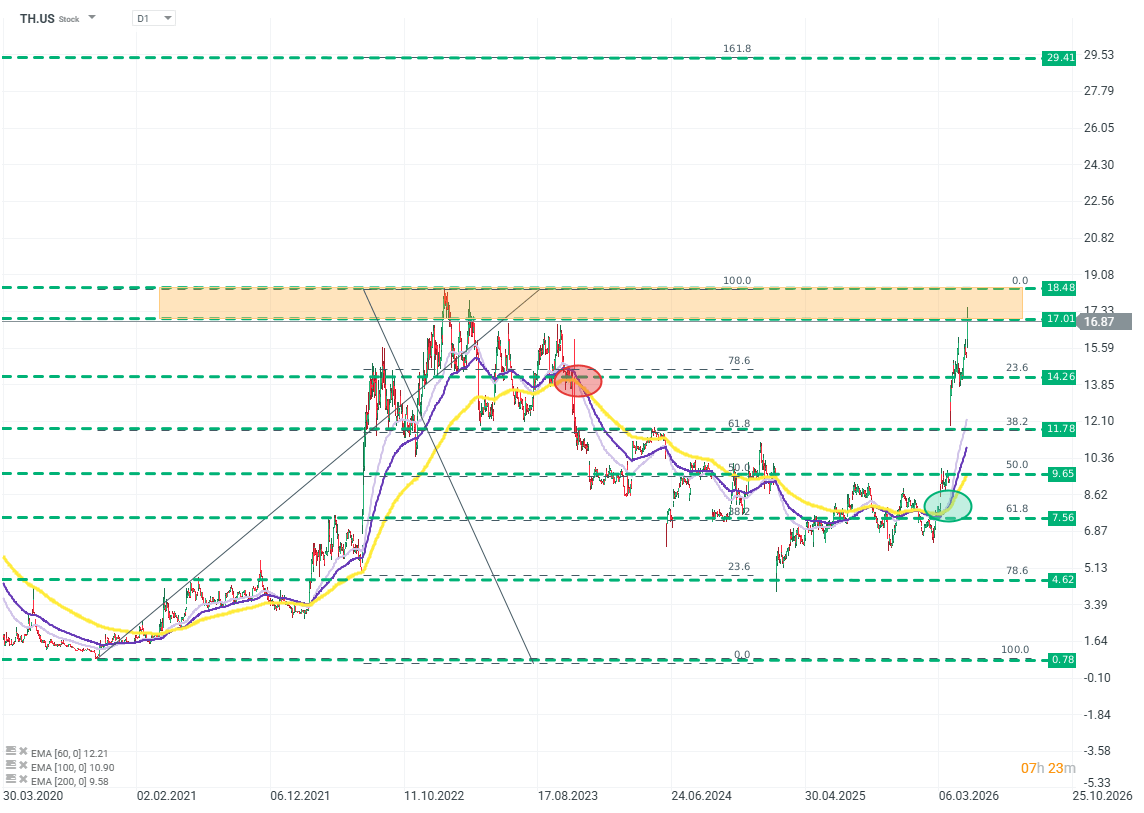

TH.US (D1)

The price increase reacts much more quickly, discounting future benefits from new contracts. The company has risen ~130% in the last three months, reversing over two years of losses. This reflects the broader market sentiment toward entities associated with the "AI boom." Source: xStation5

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

SK Hynix earnings: Did market over-sold?

France Challenges Palantir, Market Reacts.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.