Tensions in the Middle East remain elevated, with Brent crude once again trading above $100 per barrel. At the same time, Wall Street appears to be largely ignoring the risk of what could become one of the most significant energy crises in history, continuing to push toward fresh all-time highs. Meanwhile, earnings season is entering a critical phase, with results from major tech giants such as Meta, Microsoft, and Alphabet.

However, markets will not focus solely on geopolitics and Big Tech earnings. Next week will also bring key interest rate decisions from major central banks (Fed, BoJ, BoE, ECB, and BoC). Most institutions are expected to keep policy unchanged, although surprises cannot be ruled out. In this context, investors should closely monitor USDJPY, gold, and the US500 index.

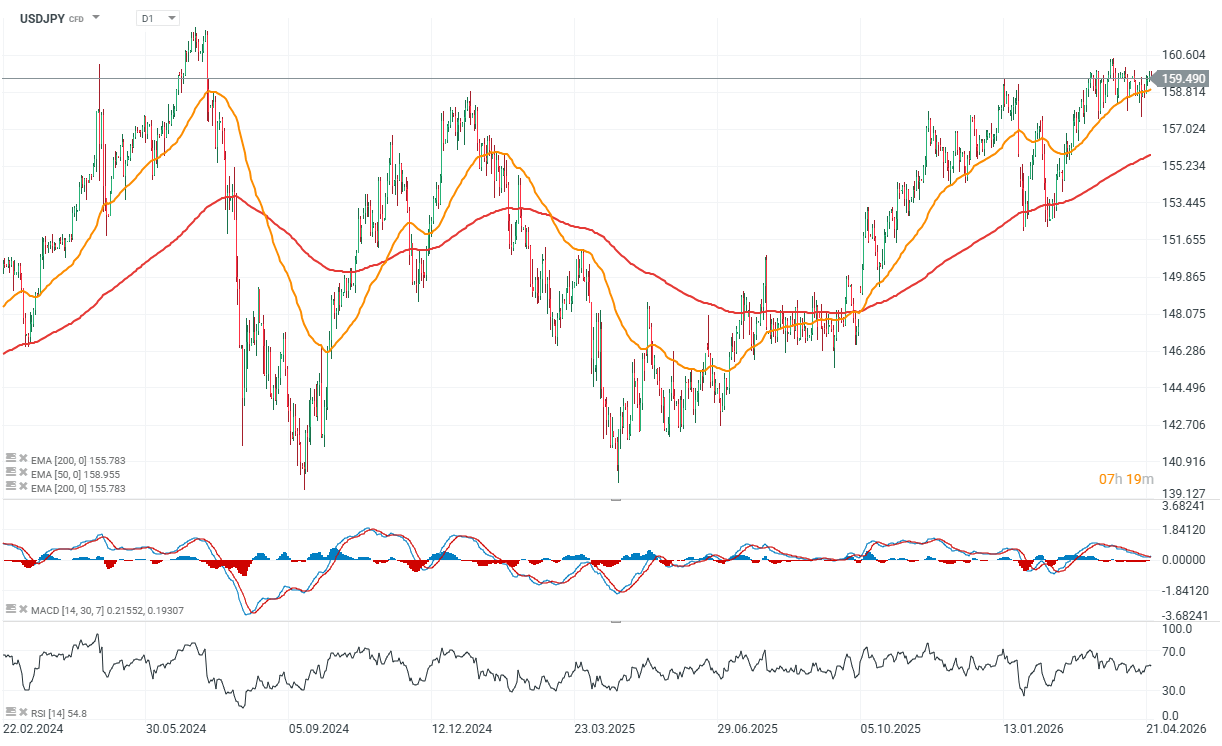

USDJPY

As early as next Tuesday, we will get interest rate decisions from both the Bank of Japan and the Federal Reserve. While not long ago markets were pricing in a possible rate hike in Japan, the country is currently facing significant pressure from rising energy prices, which are weighing on economic conditions.

As a result, markets now expect rates to remain unchanged, similarly to the Fed decision scheduled for Wednesday, April 29. It is also worth noting that this will most likely be Jerome Powell’s final meeting as Chair of the Federal Reserve, although there is still a possibility that his potential successor, Kevin Warsh, may not be confirmed by Congress before May 15. USDJPY remains elevated, with the 160 level continuing to act as a strong resistance zone.

Source: xStation5

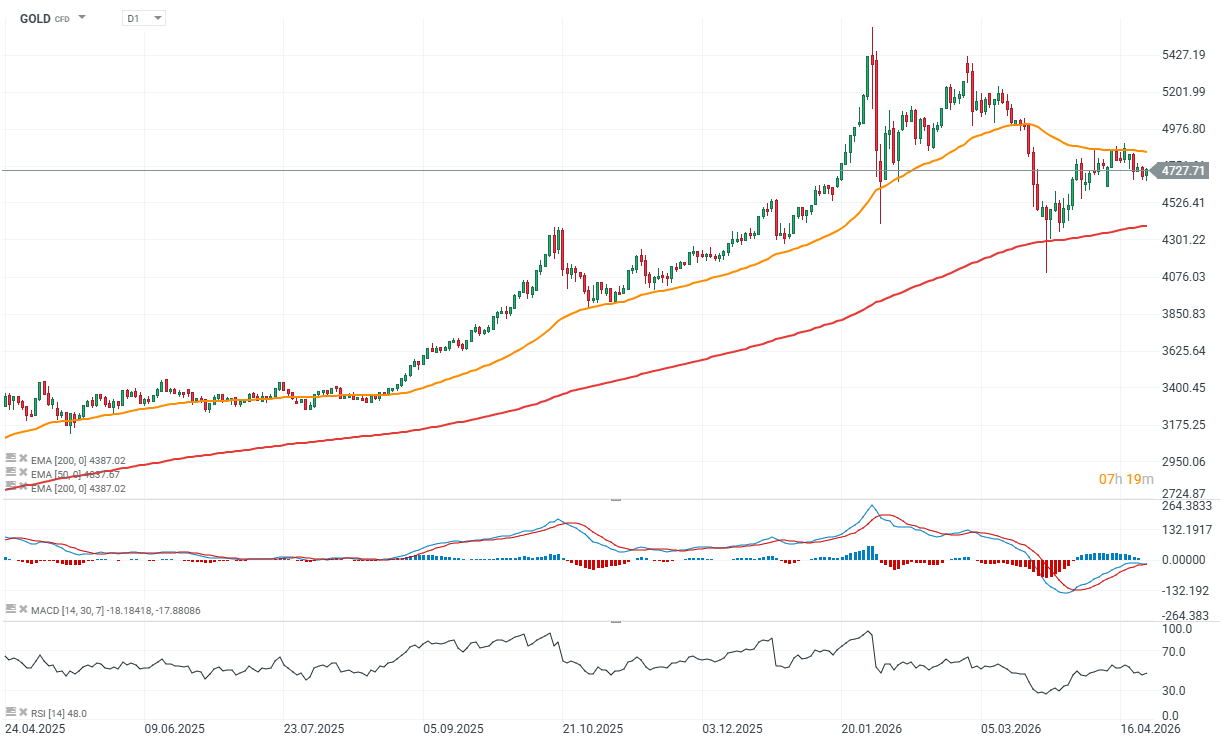

GOLD

The gold market is largely overlooking the broader energy backdrop. This is partly because oil prices, while elevated, are still hovering around $100 per barrel, and a comprehensive agreement between the U.S. and Iran remains distant.

At this stage, gold is reacting primarily to expectations around inflation and interest rates. Moderately rising inflation tends to support gold, but a sharp and sustained spike—similar to that seen in the late 1970s and early 1980s—could force a significant repricing of U.S. rate expectations.

Powell’s remarks following the Fed decision will be key, particularly in terms of how the central bank assesses inflation risks. If geopolitical tensions ease and inflation proves transitory, investors may refocus on structural drivers such as high global debt levels and the ongoing diversification of reserves away from the U.S. dollar toward gold.

Source: xStation5

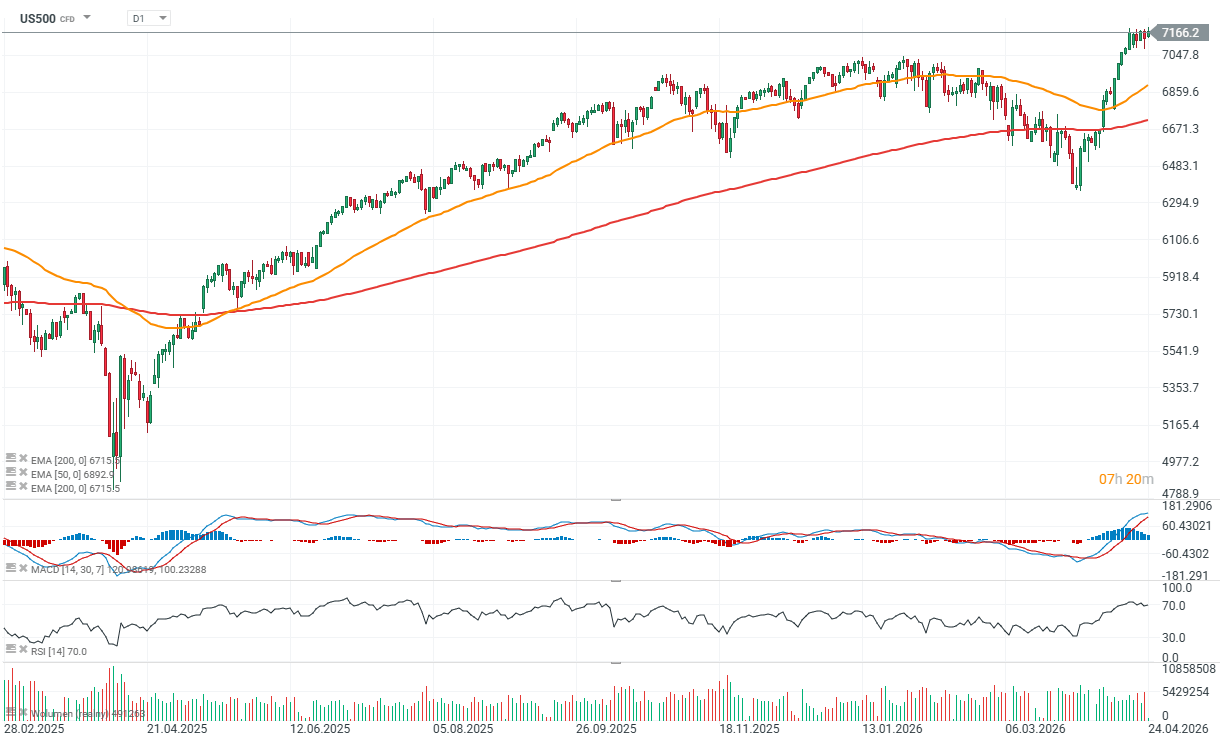

US500

The S&P 500 index and its futures have reached new all-time highs, suggesting that investors are largely dismissing geopolitical risks and focusing instead on expectations of improving economic conditions.

So far, earnings results have been strong. Tesla reported both revenue and profit growth, while also pointing to robust long-term prospects in AI and robotics.

This week’s results from Meta, Microsoft, and Alphabet will be crucial. These companies are likely to determine whether the AI-driven narrative can continue to push major U.S. indices to even higher levels. All three are scheduled to report after the close of Wednesday’s trading session.

Source: xStation5

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.