US CPI data for April showed much higher price growth than market expected. Inflation in annual terms reached 4.2% - the highest reading since mid-2008! Stock markets took a hit but concerns abated after Fed members continued to claim that high price growth is transitory. However, another acceleration is expected in May - this time to 4.7% YoY. The question now seems to be by how much must price growth accelerate for the markets to stop believing Fed?

US CPI inflation data for April showed a 0.8% month-over-month jump in the headline US price growth while annual dynamic reached 4.2% - both at the highest level since mid-2008! CPI inflation is set for another acceleration in May with market consensus expecting a reading of 4.7% YoY! Meanwhile, core gauge is seen accelerating from 3 to 3.4% YoY. Data will be release on Thursday at 1:30 pm BST.

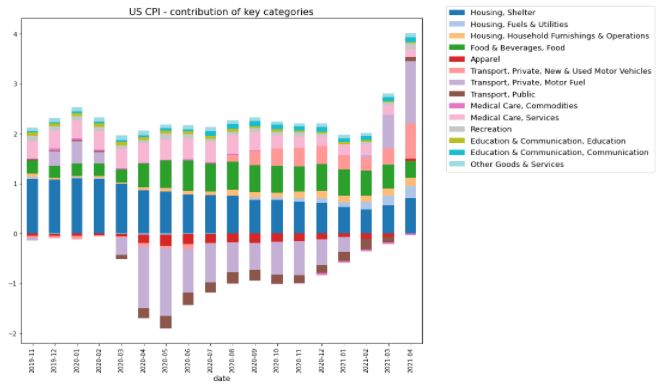

Prices increased in almost all major categories in April 2021 on the year-over-year basis. Fuel prices contributed the most to headline CPI reading. Source: Macrobond, XTB Research

Prices increased in almost all major categories in April 2021 on the year-over-year basis. Fuel prices contributed the most to headline CPI reading. Source: Macrobond, XTB Research

Is it really transitory?

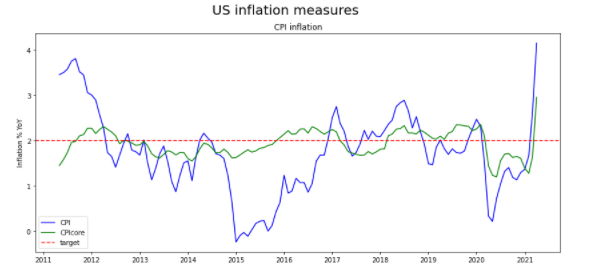

So far, it looks like investors' faith in the Fed was what prevented markets from experiencing any major reaction. Fed members continue to stress that pick-up in price growth is transitory and can be reasoned with low base effects. However, is it really so? Sure, April 2020 was a month when oil prices went negative and it was seen in the outsized contribution of motor fuels to April 2021 CPI reading. Nevertheless, as one can see on the chart above, prices increased in almost all major categories in April. Another large beat could give Fed less arguments to stick to its narrative, especially if it is accompanied by similarly "broad" pick-up in price growth. US CPI inflation jumped above the upper band of Fed target. PCE inflation (Fed's favourite measure) is also on the rise, although pick-ups are smaller due to different composition. Source: Macrobond, XTB Research

US CPI inflation jumped above the upper band of Fed target. PCE inflation (Fed's favourite measure) is also on the rise, although pick-ups are smaller due to different composition. Source: Macrobond, XTB Research

Wage growth accelerates

Another issue that seems to bite into Fed's narrative of transitory inflation is wage growth. NFP report for May showed a much higher-than-expected increase in average wages. Note that wage growth cannot be reasoned with low base effect as average wages in the US spiked after the pandemic began (due to removal of low-income jobs from the equation). Moreover, wage growth is seen as a more persistent source of inflationary pressures. Having said that, another major beat in US CPI is a potential risk event for equity markets as it may show investors that Fed is simply wrong. Data release will also be closely watched as it comes less than one week before the FOMC meeting (it will be a quarterly meeting so it will also include new macro forecasts).

Markets' reaction

US100 dropped below the 13,000 pts mark following release of April's CPI data. However, this also marked the end of a short-term correction with the market starting to regain ground later on. US tech index is trading less than 2% below its all-time highs and has been an underperformer among US indices recently. This should not come as a surprise as upbeat data from the United States shows that risk of earlier-than-expected tightening is real and the tech sector is one of the most exposed. Other markets that are likely to become more volatile in the aftermath of the release are GOLD, EURUSD and TNOTE.

US100 bottomed out after US CPI reading for April. Index has recovered around 900 points since and is trading less than 2% below all-time highs. Source: xStation5

US100 bottomed out after US CPI reading for April. Index has recovered around 900 points since and is trading less than 2% below all-time highs. Source: xStation5

Economic calendar: Strong reading from the UK labour market, German ZEW in focus

Morning wrap: Indices Look for a Rebound Amid the U.S.-Iran Conflict (21.07.2026)

Daily Summary: China Shows Its Teeth on AI; The U.K. Sees a Government Revolution 🏛️

Economic calendar - Europe's Inflation and US Housing Market in Spotlight

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.