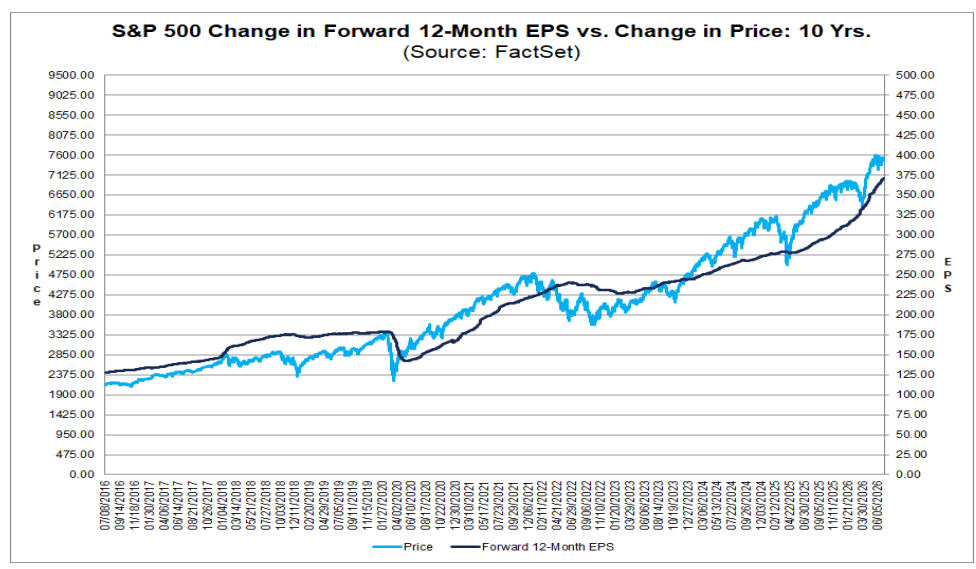

Second-quarter earnings season is getting underway with investor sentiment remaining highly optimistic and expectations for Corporate America among the strongest in years. Analysts currently expect S&P 500 companies to deliver year-over-year earnings growth of 23.6%, up sharply from the 18.8% growth forecast at the end of March.

The first wave of reports is also reinforcing the trend of positive earnings surprises. Although only 4% of S&P 500 companies have reported results so far, 89% have beaten EPS estimates and 72% have exceeded revenue expectations. Despite the index trading at a relatively elevated forward P/E of 20.5—above both its five- and ten-year averages—investors believe a strong earnings season could justify current Wall Street valuations.

Earnings Season Could Deliver Another Positive Surprise

Although the second-quarter reporting season has only just begun, history suggests that analysts often underestimate the earnings power of S&P 500 companies. The market currently expects earnings growth of around 23.6% year over year, which would already mark the second consecutive quarter with earnings growth above 20%. If the historical pattern of positive earnings surprises continues, actual earnings growth could exceed 29%, reaching its highest level since the fourth quarter of 2021.

- The current consensus calls for S&P 500 earnings growth of approximately 23.6% year over year in Q2.

- Historically, the overall earnings growth rate tends to increase throughout the reporting season as most companies report results above analyst expectations.

- In 37 of the past 40 quarters, the final earnings growth rate exceeded the estimate that existed at the end of the quarter. The only exceptions were Q1 2020, Q3 2022, and Q4 2022.

- Over the past ten years, S&P 500 companies have beaten EPS estimates by an average of 7.4%, while roughly 76% of companies have reported earnings above consensus expectations.

- On average, these positive surprises have increased the index's overall earnings growth rate by 6.2 percentage points during the reporting season.

- Applying this historical average would lift Q2 earnings growth from approximately 23.2% to around 29.4%.

- Data from the past five quarters and the past four quarters point to even greater upside potential, implying earnings growth of roughly 29.6% and as much as 31.7%, respectively.

- Even the most conservative scenario based on historical averages suggests earnings growth above 29% year over year.

Early Reports Reinforce Investor Optimism

The first batch of earnings releases suggests the reporting season may once again outperform expectations. Among the first 18 S&P 500 companies to report second-quarter results, 89% exceeded EPS estimates. Collectively, those reports have already lifted the expected earnings growth rate for the entire index from 23.2% to 23.6%, even before the bulk of companies have announced their results.

- 89% of the first reporting S&P 500 companies beat consensus EPS estimates.

- Early reports increased the expected earnings growth rate for the S&P 500 from 23.2% to 23.6%.

- If a similar pace of positive surprises continues over the coming weeks, final earnings growth could approach or even exceed 30%.

- Investors will focus not only on reported results but also on management guidance for the second half of the year, particularly regarding AI-related capital spending, cost pressures, and the impact of higher energy prices.

- Such a strong earnings season could provide a fundamental justification for current Wall Street valuations, especially across technology, semiconductor, and AI infrastructure companies.

Source: FactSet

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.