Wall Street is trading slightly higher on Tuesday as key earnings reports keep rolling in. While early bullish momentum has moderated, major U.S. indices remain in positive territory. The tech-heavy Nasdaq and small-cap Russell 2000 are leading with gains of 0.25%, followed by the S&P 500 up 0.15%. The Dow Jones Industrial Average is the outlier, hovering just below flat at -0.05%.

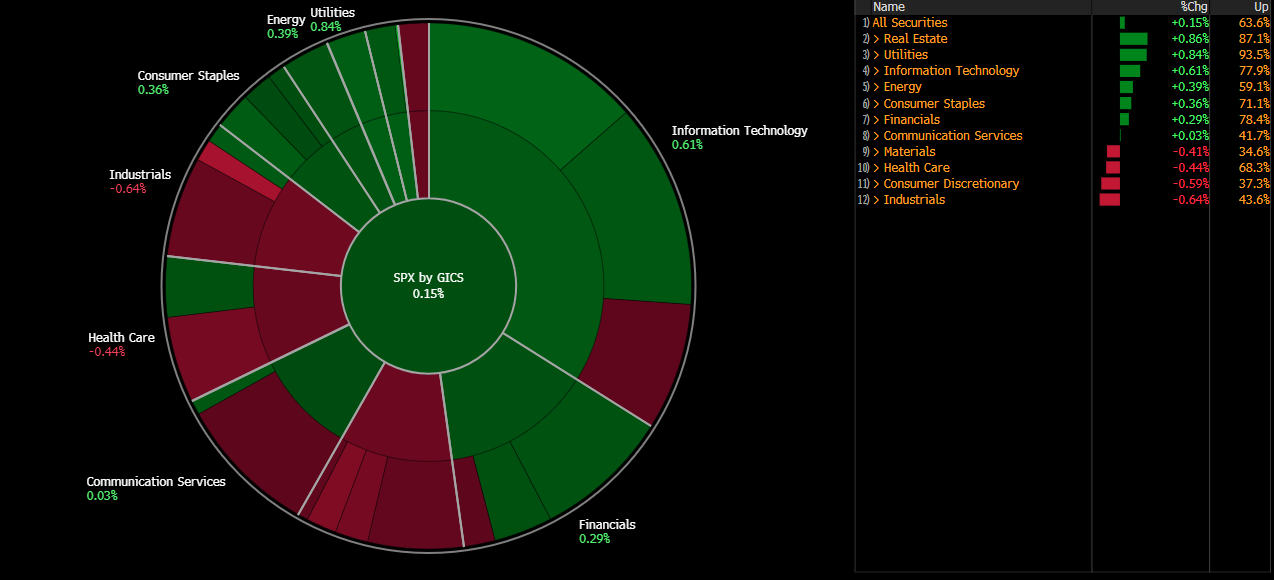

Real estate stocks are leading the market today, even as home prices continued to decline in May (-0.2% MoM vs. -0.1% forecast, after -0.3% previously). Tech remains strong, extending its rally ahead of tomorrow’s Magnificent 7 earnings. On the downside, healthcare is under notable pressure, with Novo Nordisk and UnitedHealth disappointing reports weighing on the sentiment on both sides of the Atlantic. The broader pharmaceuticals space is also feeling the strain, as investors brace for potential sector-specific tariffs expected in the coming weeks.

JOLTS came in little changed, though notable declines in openings were seen in accommodation, healthcare, and finance. Quits remained flat at 3.1 millions, suggesting continued labor market stability amid sector-specific shifts.

Today's volatility in S&P 500 sectors. Source: Bloomberg Finance LP

US500 (H1)

S&P 500 futures are holding steady near the open, having already given back some of their early pre-market gains. Despite this, the index continues to test new record highs, currently up about 0.15% from yesterday’s close. Price action is finding solid support around the 30-hour exponential moving average (EMA30, shown in light purple), which is maintaining its role in sustaining the recent upward momentum. The Relative Strength Index (RSI) remains in neutral territory, indicating there is still ample room for further upside beyond the pre-market peaks—provided the rest of earnings for today won’t upset the markets. That said, investors will likely remain moderately cautious ahead of the highly anticipated earnings from the “Magnificent 7” tech giants, with Meta and Microsoft reporting on Wednesday, followed by Amazon and Apple on Thursday.

Source: xStation5

Company news:

-

Boeing (BA.US) beat Q2 revenue estimates with $22.7B, up 35% YoY, while adjusted loss per share narrowed to $1.24 versus $1.40 expected. CEO Kelly Ortberg’s turnaround plan cut cash burn drastically to $200M from $2.3B last quarter. Production improvements and steady 737 Max deliveries underpin optimism for 2025 as a “turnaround year,” with plans to ramp 737 Max output to 42 jets/month by midyear. The stock is down 0.7%.

-

Merck & Co.'s (MRK.US) slump 7.6% after extending its Gardasil shipment pause to China through year-end amid weak demand, dragging vaccine sales down 55% YoY. Q2 EPS of $2.13 missed, though sales of $15.81B slightly beat. Keytruda and Lynparza exceeded expectations, offsetting vaccine weakness. Merck trimmed its 2025 revenue outlook range slightly and announced a restructuring plan targeting $3B in annual savings by 2027, with reinvestment in R&D and new products.

-

PayPal (PYPL.US) raised its 2025 EPS guidance to $5.15–$5.30, above estimates, as CEO Alex Chriss’s profitability-focused turnaround gains traction. Q2 saw Venmo revenue jump 20% and transaction margin dollars rise 7% to $3.8B, with operating margin expanding to 19.8%. Strong U.S. consumer spending helped offset macro risks, as PayPal leans into branded checkout and high-margin growth areas. While Q3 EPS guidance of $1.18–$1.22 was in line, shares dip 6.8%.

-

Procter & Gamble (PG.US) topped Q4 expectations with $1.48 core EPS and $20.89B in sales, driven by pricing gains. Organic revenue rose 2%, led by modest growth across all categories. Baby, Feminine & Family Care beat estimates, while Beauty, Grooming, and Health Care lagged. FY2026 guidance sees 0–4% organic revenue and EPS growth. Capital return plans include $10B in dividends and $5B in buybacks. FX and tariffs remain key headwinds. The stock is down 0.7%.

-

Spotify (SPOT.US) stock slides 8.8% after a surprise Q2 loss and weak Q3 guidance. EPS came in at a €0.42 loss vs. €1.97 profit expected, with revenue of €4.19B missing forecasts. Currency headwinds shaved €104M off revenue, while social charges and rising costs pressured margins. Despite the miss, user growth remained strong: MAUs rose 11% to 696M, and premium subscribers hit 276M. CEO Daniel Ek reaffirmed 2025 as a "standout year," focusing on long-term value over short-term metrics.

-

UnitedHealth (UNH.US) shares are down 5.5% after reaffirming a 2025 adjusted EPS forecast of at least $16—well below the $20.40 consensus. Revenue guidance also missed estimates. Q2 adjusted EPS of $4.08 fell short, while revenue grew 13% to $111.62B, in line with forecasts. Segment results were mixed: UnitedHealthcare and OptumRx beat, but OptumHealth and OptumInsight lagged. Higher care costs and compressed margins drove the cautious outlook. Peers Humana, Elevance, and Cigna also declined on the news.

-

Whirlpool (WHR.US) shares plunged 10.2% as Q2 results missed estimates and guidance was slashed. EPS came in at $1.17 vs. $1.58 expected, with $3.7B in sales below the $3.8B consensus. The company cut FY EPS guidance to $6–$8 (from $10) and halved its dividend. Competitive stockpiling ahead of tariffs hurt U.S. sales, though Whirlpool remains bullish on housing trends and its domestic manufacturing strength.

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.