US indices are opening higher today, with Nasdaq 100, S&P 500, the Dow Jones Industrial Average and the Russell 2000 futures posting solid gains. Strong results from Taiwan’s AI chip heavyweight TSMC (TSM.US) have propelled tech stocks and set the “market optimism machine” in motion. Nasdaq (US100) futures are up more than 1% early in the US session.

Moves across the semiconductor segment are particularly strong - ranging from Europe’s ASML to US names such as Nvidia, AMD, Lam Research and KLA Corp (KLAC.US). KLA is seeing an outright impressive ~8% jump following an upgrade at Wells Fargo, driven by the 2nm roadmap and the high-performance computing (HPC) cycle.

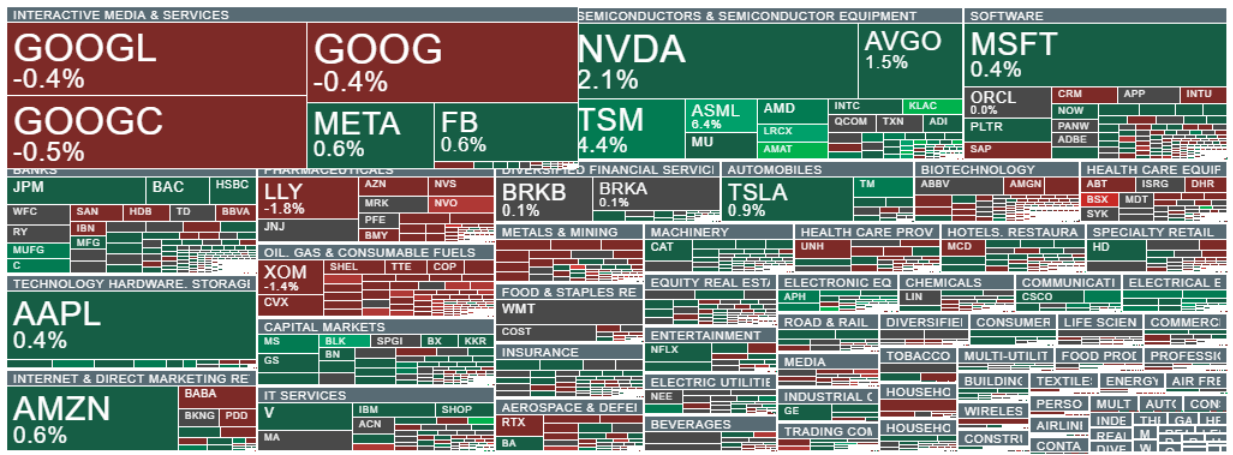

Source: xStation5

Semiconductor stocks and the financial sector are supporting today’s gains in equities. Source: xStation5

Company news

-

Nvidia sets the pace among the “Magnificent Seven” after TSMC’s strong earnings and outlook, driven by AI demand, Nvidia (NVDA) is up +2%, Amazon (AMZN) +1%, Tesla (TSLA) +0.5%, but Alphabet (GOOGL) lags, losing -0.5%. Microsoft and Apple shares are slightly higher.

- Amplitude (AMPL) rises 5.7% after Morgan Stanley upgraded the software company from equal-weight to overweight.

- Applied Materials (AMAT) gains 2.1% after Barclays also upgraded the stock from equal-weight to overweight. The name is also benefiting from a stronger demand backdrop after TSMC set a more ambitious 2026 capex target—read by the market as a sign of robust AI-related chip demand.

- Chip equipment names are clearly higher in US pre-market trading: Lam Research (LRCX) +8.2% and Teradyne (TER) +4.1%. The backdrop is similar—TSMC’s 2026 spending target came in above expectations, which investors interpret as confidence in the durability of the AI boom.

- Clearway Energy (CWEN) rallies 7.5% after announcing a package of power purchase agreements (PPAs) with Google for 1.17 GW in Missouri, Texas and West Virginia.

- Coinbase (COIN) slips 1.1% after the US Senate Banking Committee postponed a debate on crypto market structure, while Coinbase withdrew support for a bill proposal concerning caps on stablecoin rewards.

- Disc Medicine (IRON) drops 7.1% after reports that the FDA delayed its review of an experimental treatment for a rare blood disorder that was part of an accelerated voucher program (per Reuters).

- Goldman Sachs (GS) gains 2.3% after its quarterly report: 4Q FICC and trading revenues beat the average analyst estimate.

- Millicom (TIGO) rises 3% after UBS upgraded the stock from neutral to buy, citing an attractive valuation and potential benefits from consolidation, which could support growth and cash returns.

- Morgan Stanley (MS) falls 1% despite posting 4Q wealth management revenues above consensus—investors appear to have taken a cooler view of other parts of the report.

- Penumbra (PEN) jumps 13% after Boston Scientific agreed to acquire the company in a cash-and-stock deal valuing it at around $14.5bn.

- Samsara (IOT) is up 2.6% in pre-market trading after BNP Paribas upgraded the stock to outperform from neutral, pointing to stronger demand.

- Sandisk (SNDK) gains 4.1% after Benchmark raised its price target to $450 from $260. Analysts note that even after the strong rally, “the story still holds” and rests on several solid pillars.

- Southwest Gas Holdings (SWX) rises 1.4% after Citi upgraded the stock from neutral to buy, citing an acceleration in EPS growth.

- Talen Energy (TLN) jumps 11% after signing agreements to purchase three gas-fired power plants from Energy Capital Partners for $3.45bn. The deal increases its generation capacity portfolio by roughly 2.6 GW.

BlackRock hits new records

Shares of BlackRock, the world’s largest asset manager, are up 2.2% after earnings. Adjusted EPS and net inflows came in well above market expectations. BlackRock reached a new all-time scale record, with assets under management (AUM) rising to $14.04 trillion—highlighting how strongly the firm “rides the market’s current” when asset valuations climb.

The AUM surge was driven largely by the 4Q equity rally, fueled by:

-

AI enthusiasm

-

easing rate pressure

-

relatively stable US economic growth

Results beat Wall Street expectations, and the market reaction was swift: BlackRock shares were up about +2.5% in pre-market trading, suggesting investors welcomed both the revenue scale and the quality of inflows. Revenue increased to $7.0bn from $5.68bn y/y, beating the analyst consensus of $6.69bn. For BlackRock, that matters because most revenues are calculated as a percentage of AUM—so rising assets act like operating leverage. EPS clearly beat forecasts: $13.16 versus expectations around $12.21. For investors, that signals revenue growth is translating into net results more efficiently than the market assumed.

- Adjusted net income rose to $2.18bn from $1.87bn a year earlier, pointing to a strong profitability quarter despite rising cost pressure.

- Costs rose sharply: $5.35bn vs $3.6bn y/y—putting a key issue on the radar going forward. At this scale, investments in growth and expansion can be “expensive,” and the market will watch closely whether higher spending delivers durable payoffs.

- Equity product inflows were essentially flat y/y: $126.05bn vs $126.57bn a year earlier. That may look like “no fireworks,” but at this scale, stability itself is a strong signal.

- Fixed-income inflows were very strong: $83.77bn in the quarter, which Reuters links to a more dovish Fed stance and a cooling labor market. This is important—it shows BlackRock is benefiting from investors rotating back into bonds.

- Total long-term net inflows came in at roughly $267.8bn, with ETFs once again the main locomotive. This is the key point: BlackRock is effectively “wired” to win when capital returns to passive, low-cost strategies.

The company also posted record annual net inflows of $698.26bn, reinforcing the picture of BlackRock as the biggest capital-gathering machine in the world.

ETFs: low fees, massive scale

ETFs remain the core engine of BlackRock’s organic growth, even if the unit economics carry lower margins. The mechanism is simple: lower fees are offset by enormous scale and the iShares network effect.

The passive trend isn’t slowing. Investors continue to look for low-cost diversification, and the “ETF as a default investment product” narrative is only getting stronger over time.

Performance fees: the market is paying for results again

Performance fees jumped 67% to $754m, suggesting the firm benefited not only from rising AUM and base fees but also from strong performance in strategies that include success-fee components.

Notably, this marks another strong quarter in this line item—performance fees were up around 33% in 3Q. It adds an “extra layer” of revenue that isn’t always repeatable, but can be highly profitable.

“Private market play”: BlackRock wants higher-margin revenues

BlackRock is increasingly diversifying toward higher-fee products, which makes sense given the intensifying fee competition in ETFs.

The firm is leaning more heavily into:

-

private markets

-

real estate

-

infrastructure

-

AI-linked assets (data centers, energy infrastructure)

This direction is margin-accretive because private assets typically generate higher fees than ETFs. In other words, BlackRock is trying to build a “higher-end dining room” next to a very large—but lower-margin—“ETF cafeteria.” Private market inflows were $12.71bn in the quarter. The scale is still nowhere near ETFs, but the trend is clear: the company is steadily building a second pillar. The target is ambitious: $400bn of cumulative fundraising by 2030. That suggests BlackRock sees private markets not as an add-on, but as a future major source of margins and more stable revenues. A particularly interesting move is its plan to integrate private assets into retirement programs—potentially opening up a huge pool of long-term capital.

BlackRock shares (D1 interval)

Source: xStation5

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Did SaaS lost too much? Morgan Stanley says yes.

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.