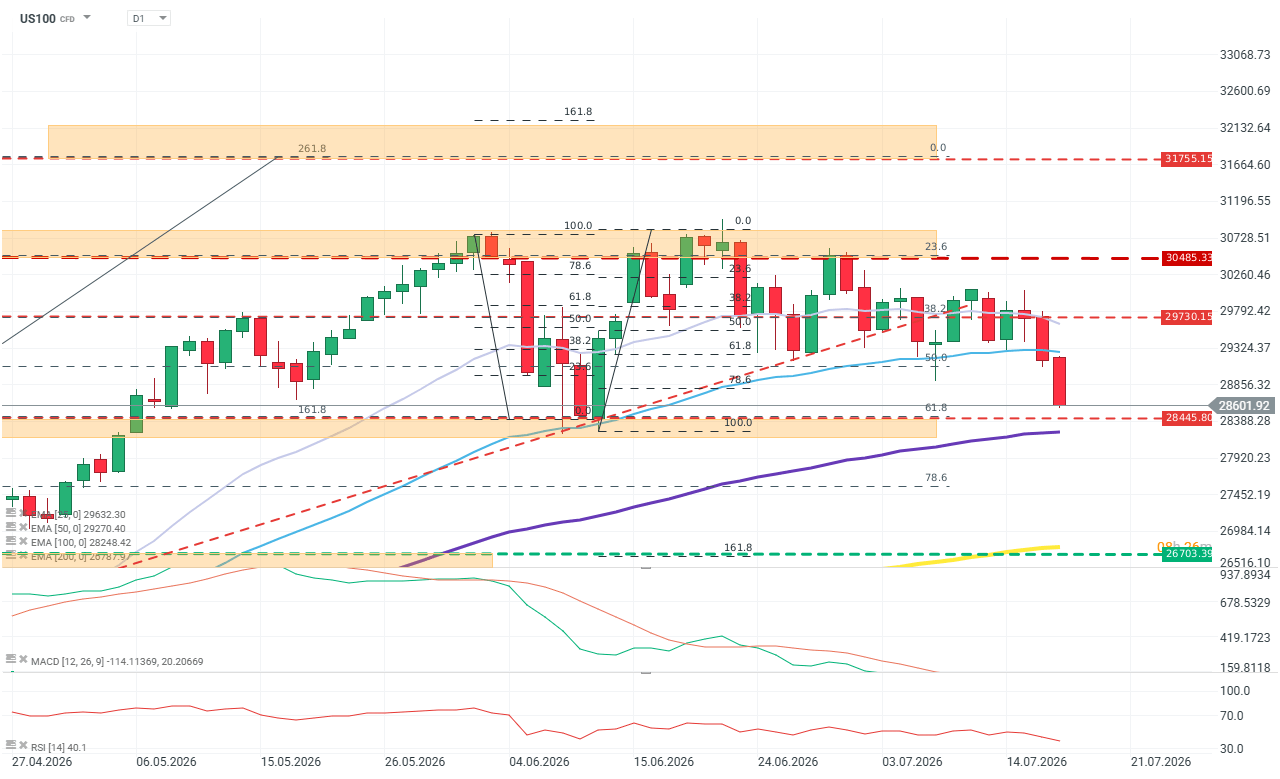

The US stock market opens the final session of the week with further declines. The largest drops are seen in US100 futures, reflecting weakening sentiment toward the technology sector. Losses are around 1.5%. The NASDAQ 100 is now roughly 7% off its peak.

Concerns about the health of tech companies, the AI rally, and semiconductors are increasingly being joined by the escalating conflict in the Strait of Hormuz. Iran responded to the renewed bombardments in Iran with attacks on US military facilities in the Persian Gulf region.

Inflation fears are also not easing due to news from Russia. Concerns about harvests and exports of wheat and oil are becoming more serious. Increasingly effective Ukrainian strikes are disrupting the oil industry and shipping in the Sea of Azov.

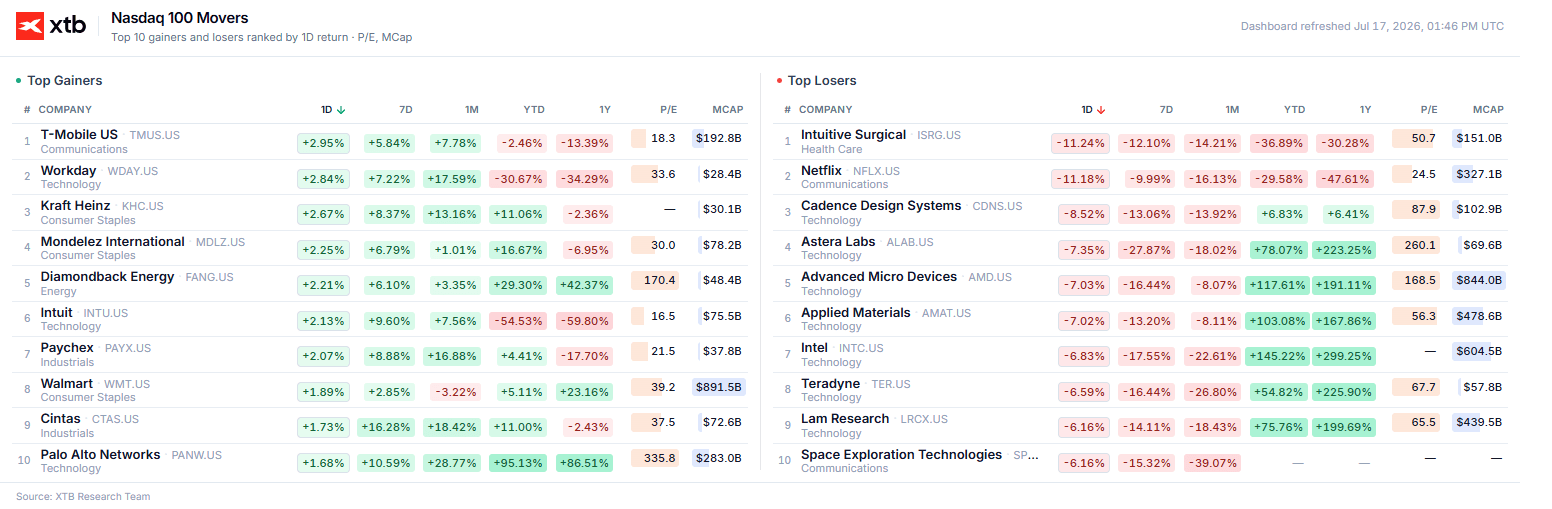

Negative sentiment is also being reinforced by Netflix’s latest results. The streaming leader disappointed both on results and guidance, and concerns about the company’s condition are spilling over to the rest of the sector.

Company news

- Netflix (NFLX.US): Q2 2026 results showed EPS just within the market’s expected range, coming in at $0.80. Revenue rose to $12.56 billion, below Wall Street expectations of $12.58 to $13.0 billion. However, guidance weighed most heavily on the stock. Management guided Q3 EPS at $0.82, also below forecasts. The stock is down more than 10%.

- Intuitive Surgical (ISRG.US): The maker of da Vinci surgical robots fell about 10% after Q2 results. Despite earnings beating expectations, the company did not raise its full fiscal year guidance.

- SpaceX (SPXC.US): The planned “Starship” test flight was called off just before launch on Thursday due to a failure in one of the rocket’s engines. The stock fell 4% and is now trading below its IPO price.

- Semiconductor and memory stocks remain in a downtrend. Intel, Marvell, and AMD are down around 4% at the open. Nvidia, Micron, and Broadcom are down more than 2%.

- Nebius (NBIS.US): The “Neo Cloud” company issued $775 million in secured bonds. According to management reports, demand for the debt instruments significantly exceeded supply. The stock is down 14%.

Technical analysis of US100 (D1)

Sellers have recently taken control on the chart, pushing prices below resistance at the 38.2% and 50% Fibonacci retracement levels. The next target for sellers is a break below 28,445, from where they could extend the correction toward 27,000 points. Supporting buyers is a double resistance zone based on the EMA100 and the 61.8% Fibonacci retracement. RSI is lower (40) but not yet in oversold territory. However, the MACD average still works against buyers. Source: xStation5

Macroeconomic data

- Building permits showed a larger than expected decline. In June, 1.36 million permits were issued versus expectations of 1.4 million.

- US export prices fell 0.6% (more than expected), while import prices rose 0.3% (well above expectations).

- Industrial production rose 0.1% in June versus expectations of 0.2%.

- Overall, the macro releases paint a negative picture of the US economy, which still seems to be masked by nominally strong GDP growth and falling inflation.

- Half an hour after the session opens, University of Michigan data will be released. The market expects a slight improvement in consumer sentiment and a decline in inflation expectations.

Bitcoin Near $64000 as ETF Inflows Return

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.